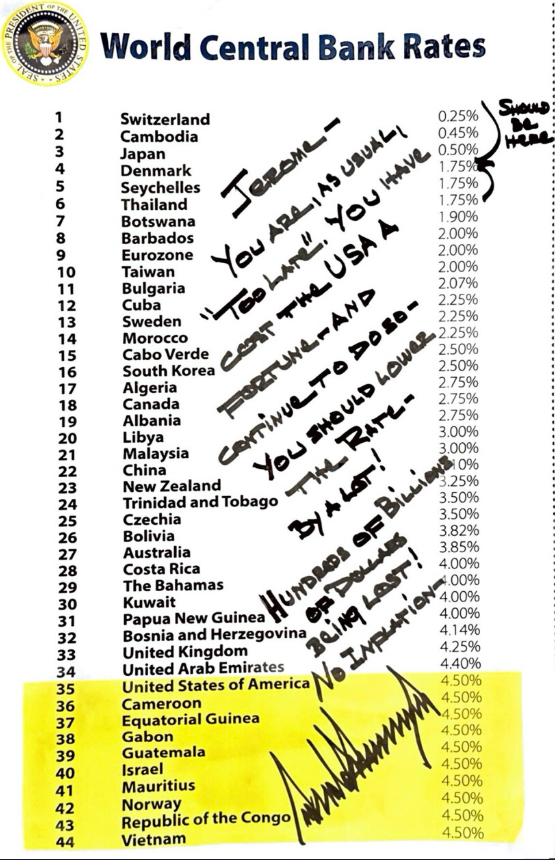

| President Donald Trump wants us to know that his opinions on monetary policy differ from those currently in charge of the Federal Reserve. On Truth Social, he has posted this: Jerome “Too Late” Powell, and his entire Board, should be ashamed of themselves for allowing this to happen to the United States. They have one of the easiest, yet most prestigious, jobs in America, and they have FAILED — And continue to do so. If they were doing their job properly, our Country would be saving Trillions of Dollars in Interest Cost. The Board just sits there and watches, so they are equally to blame. We should be paying 1% Interest, or better!

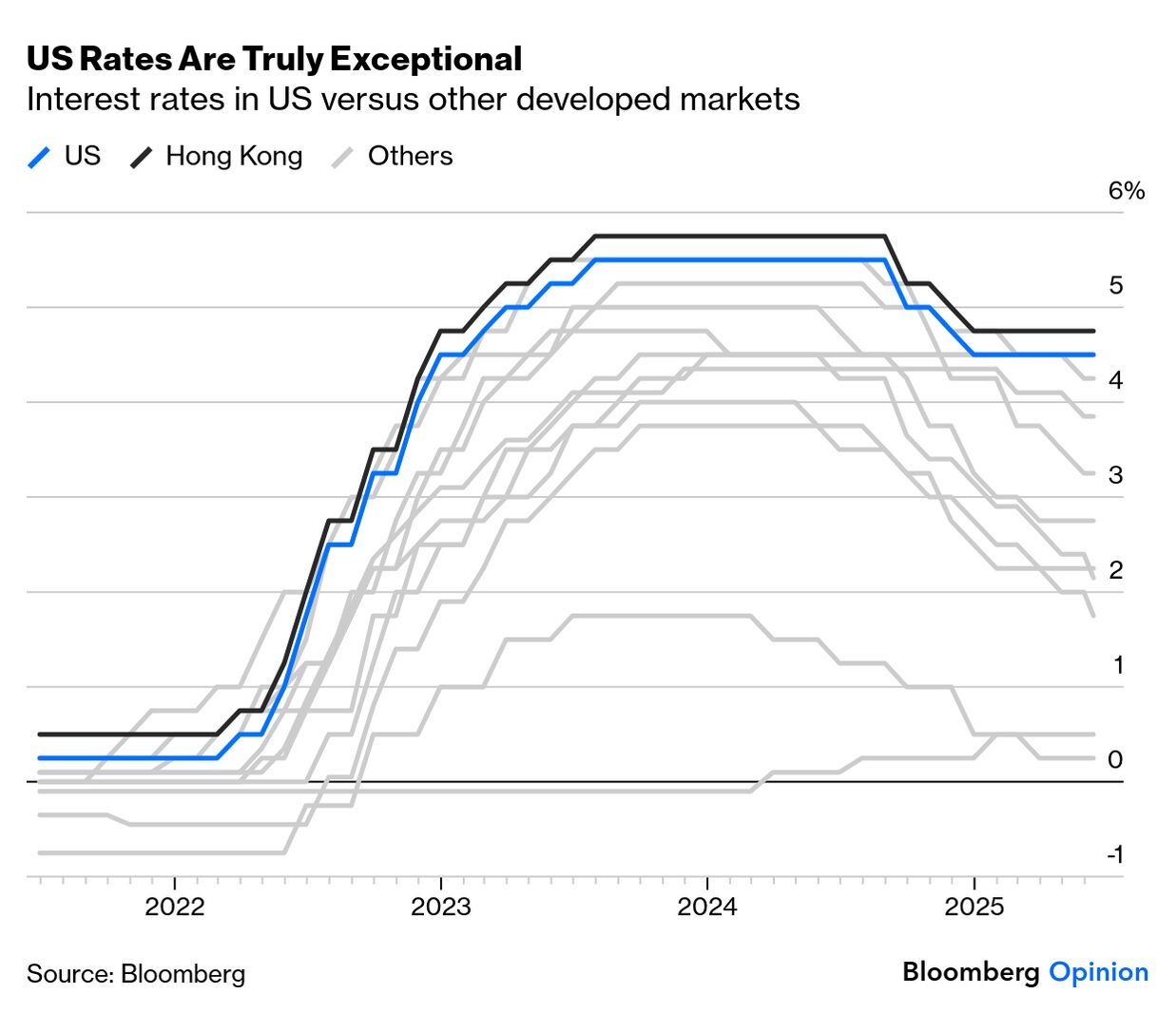

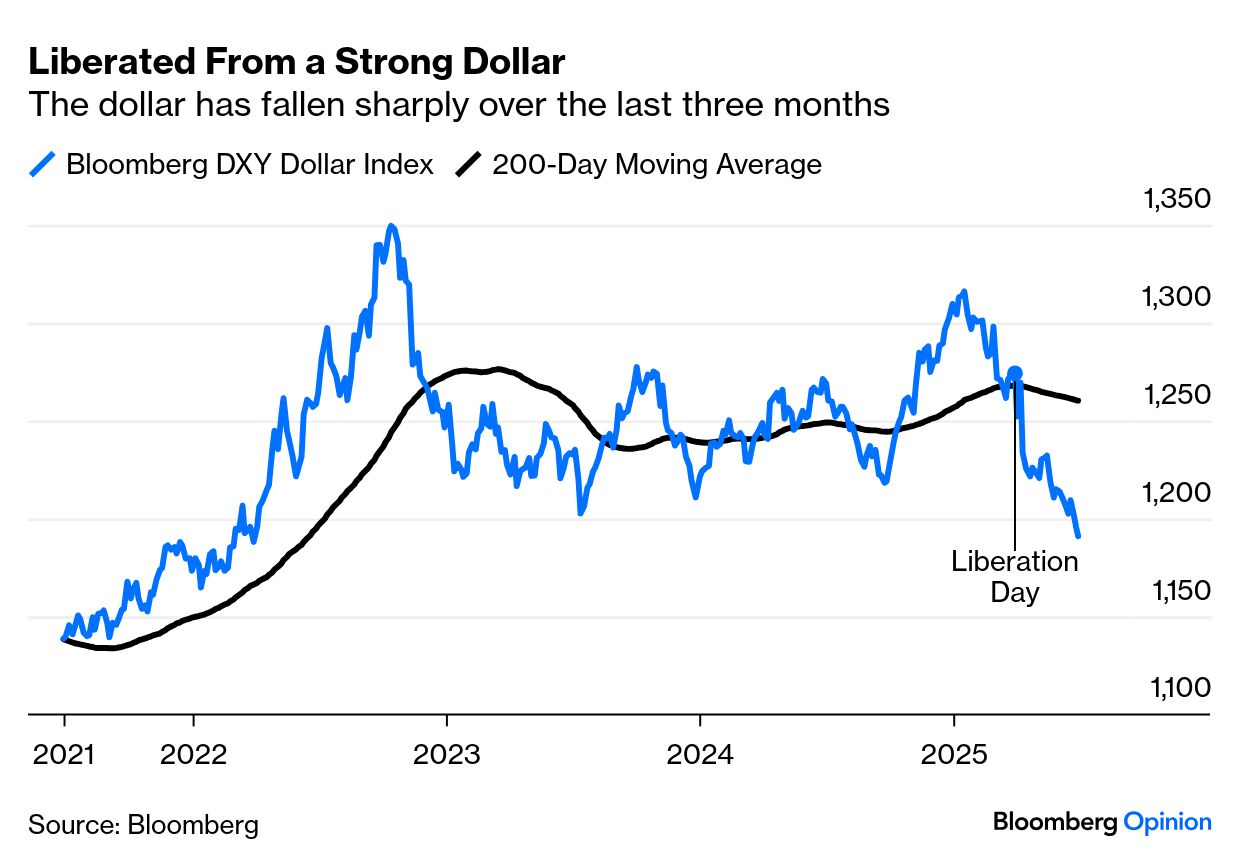

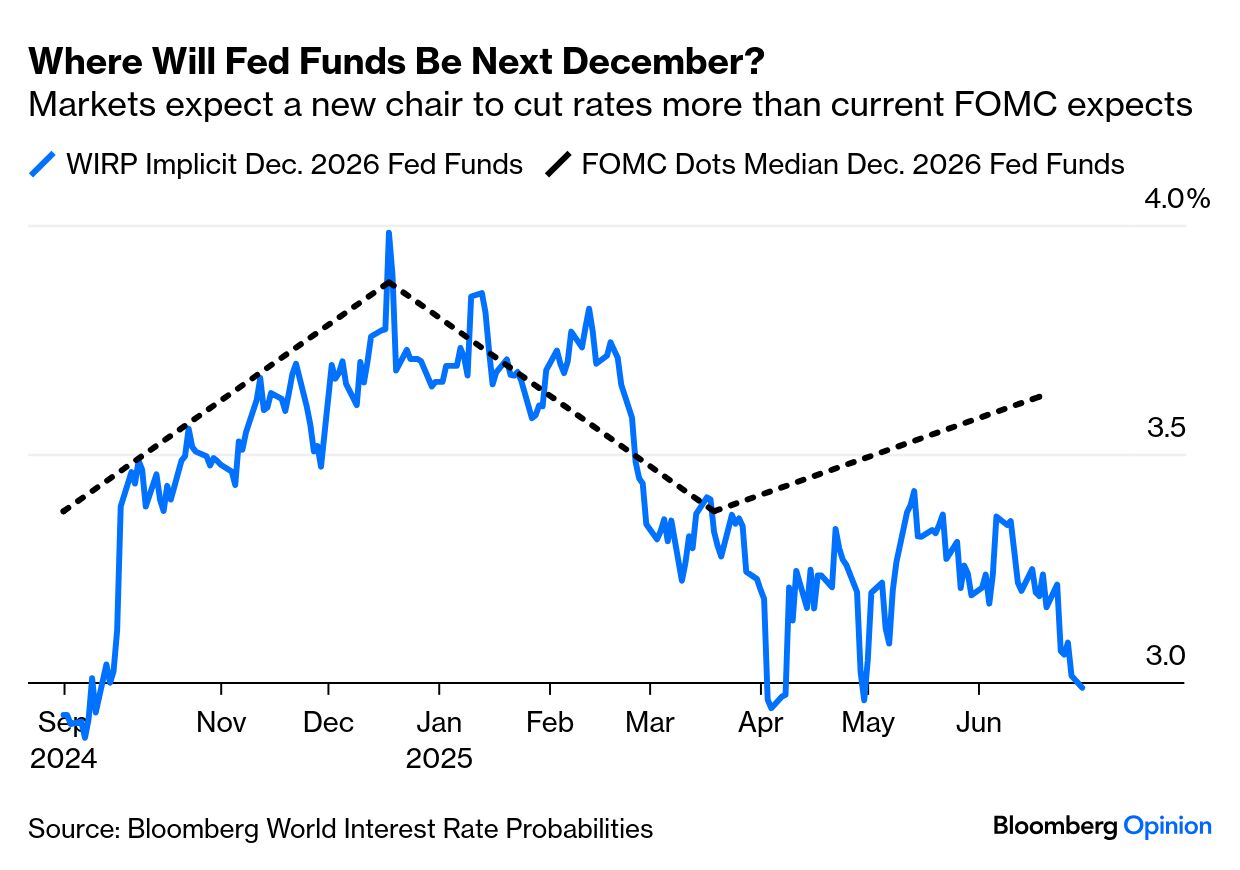

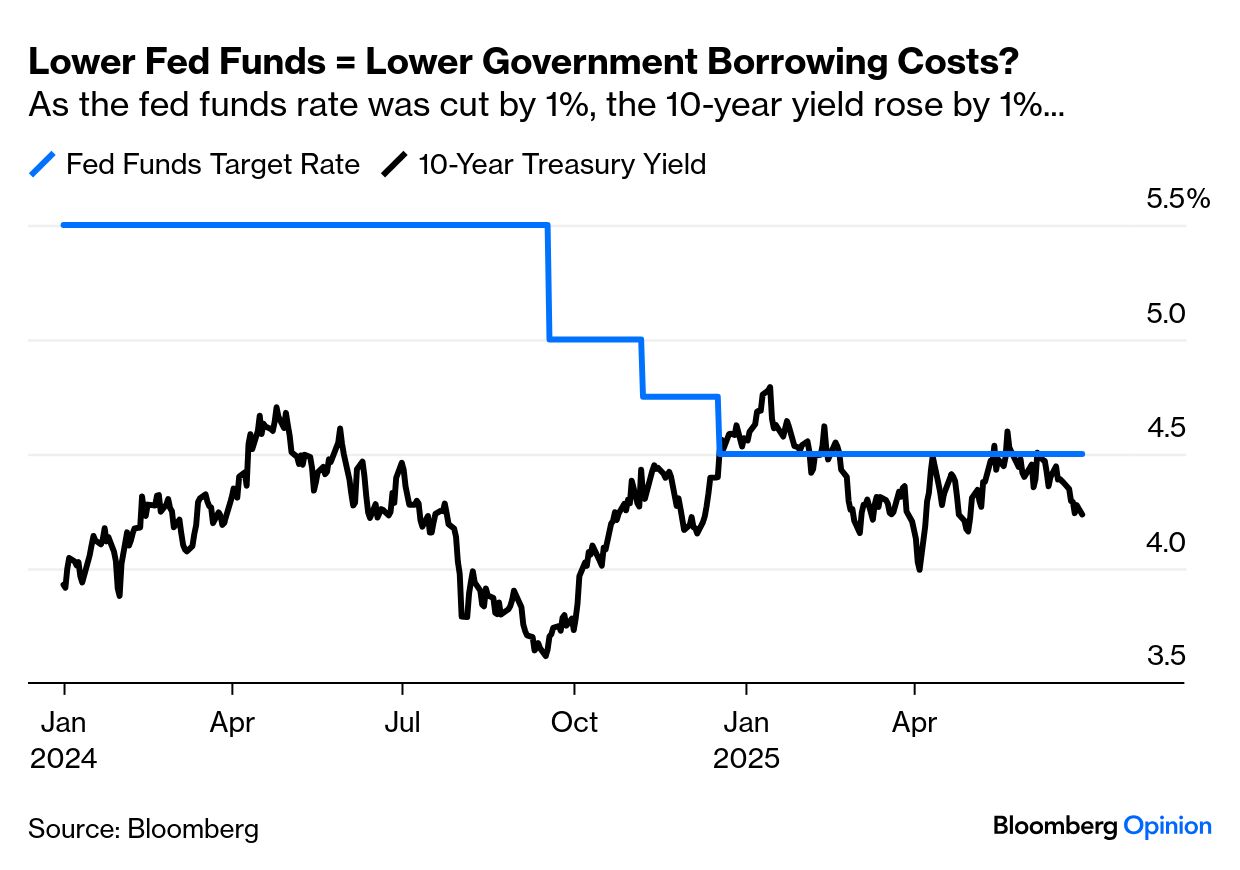

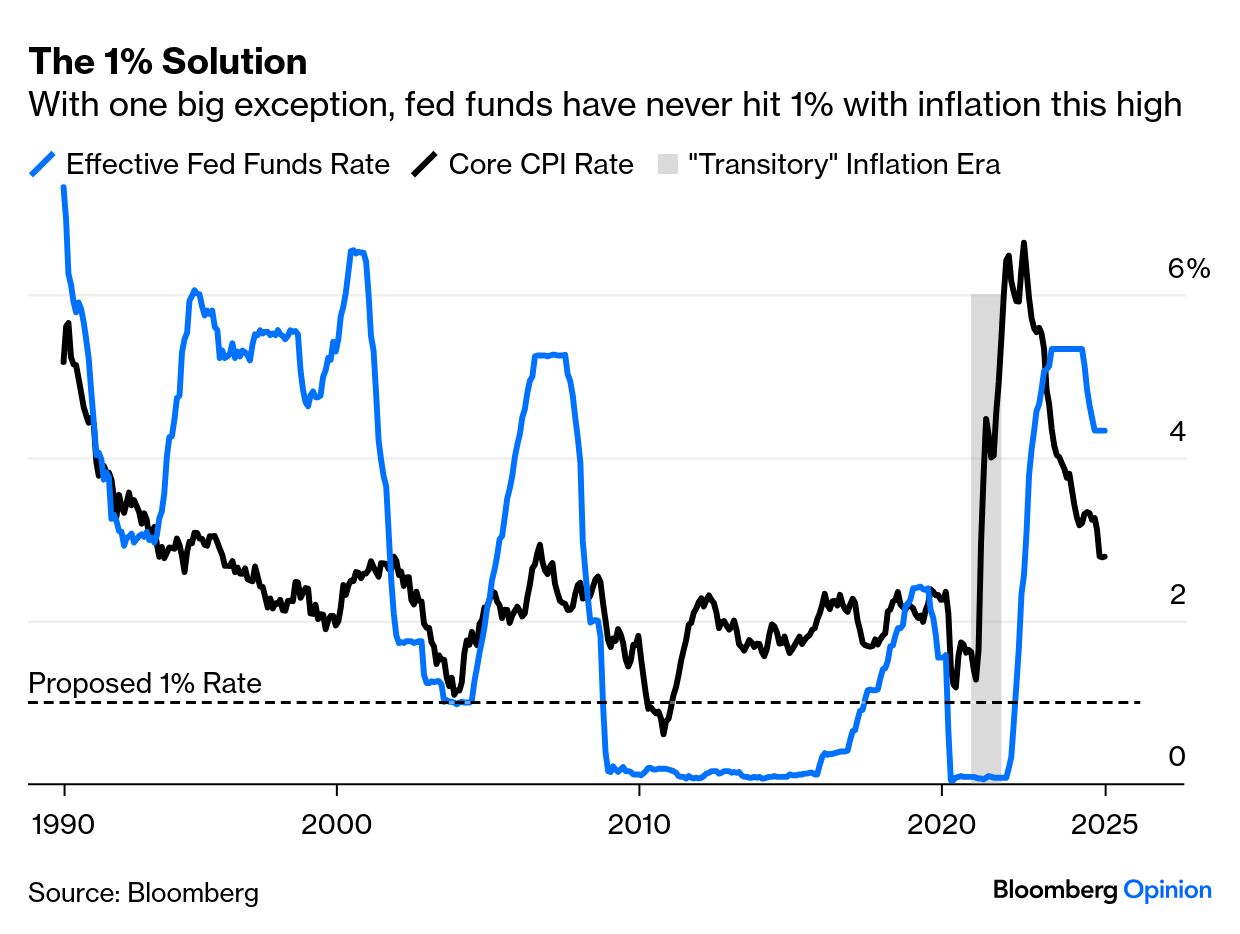

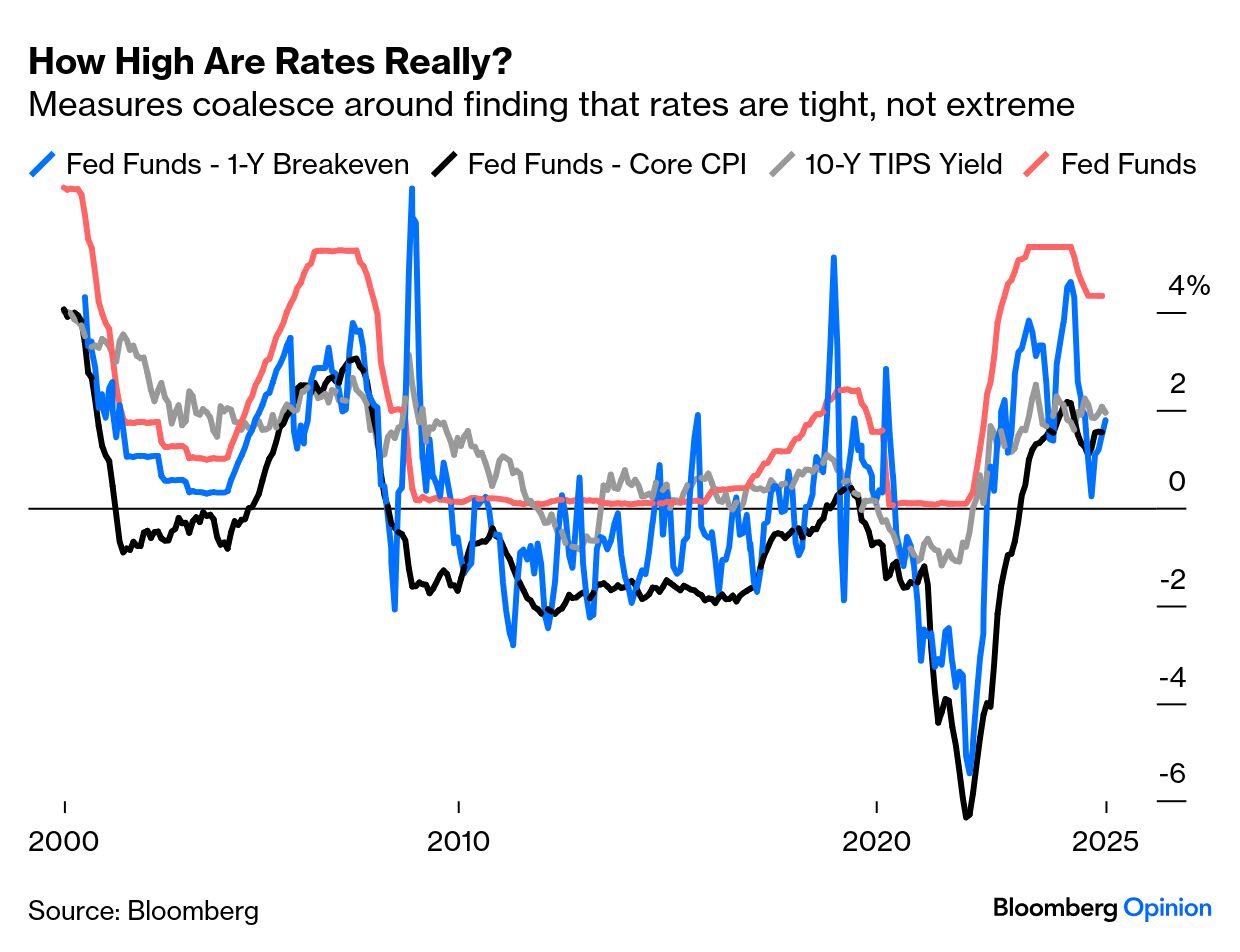

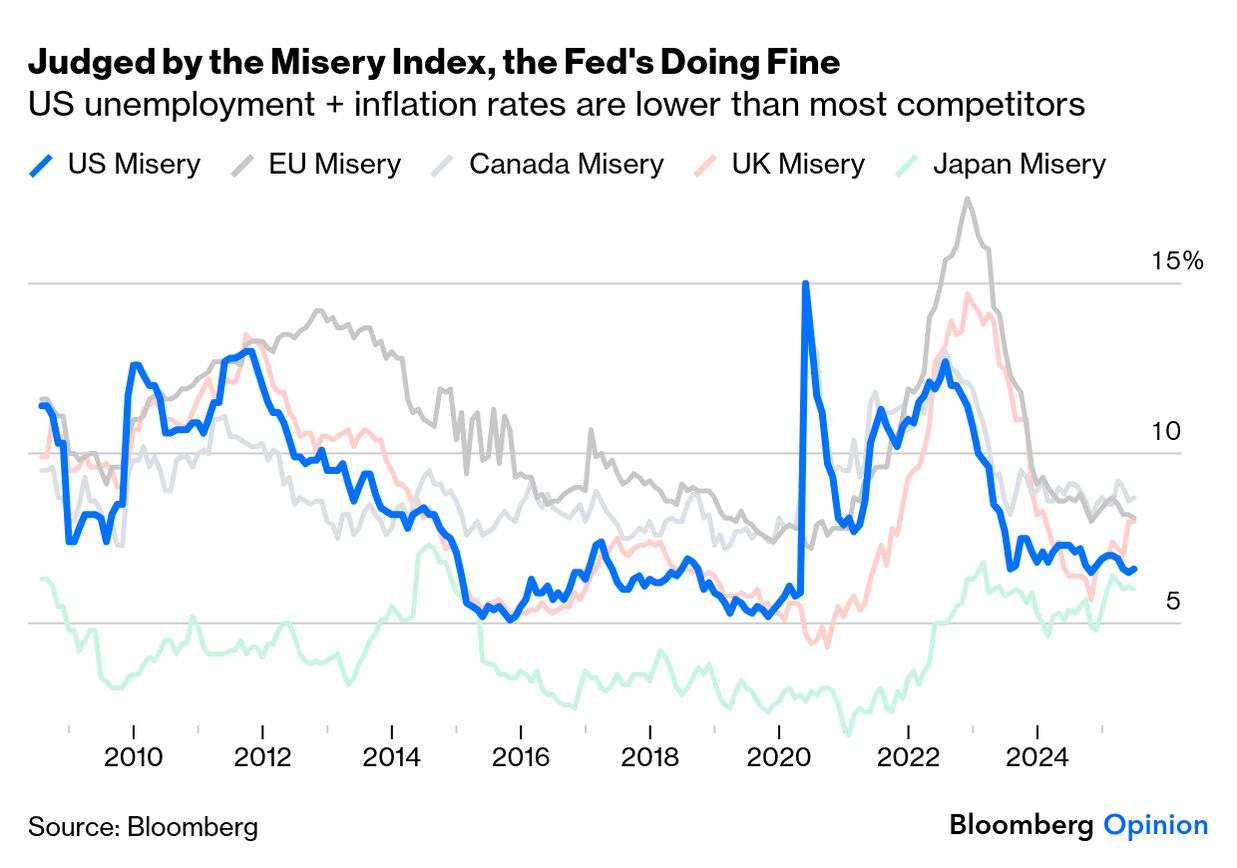

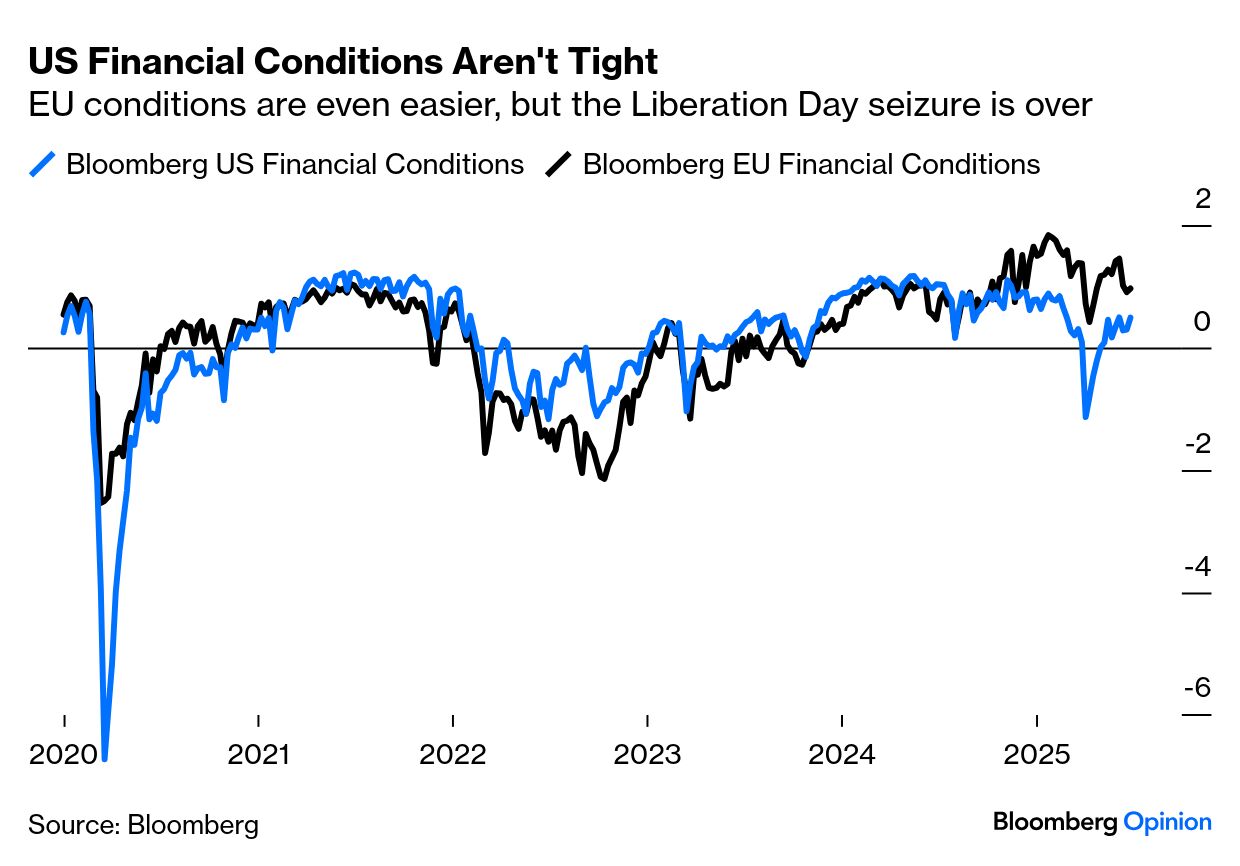

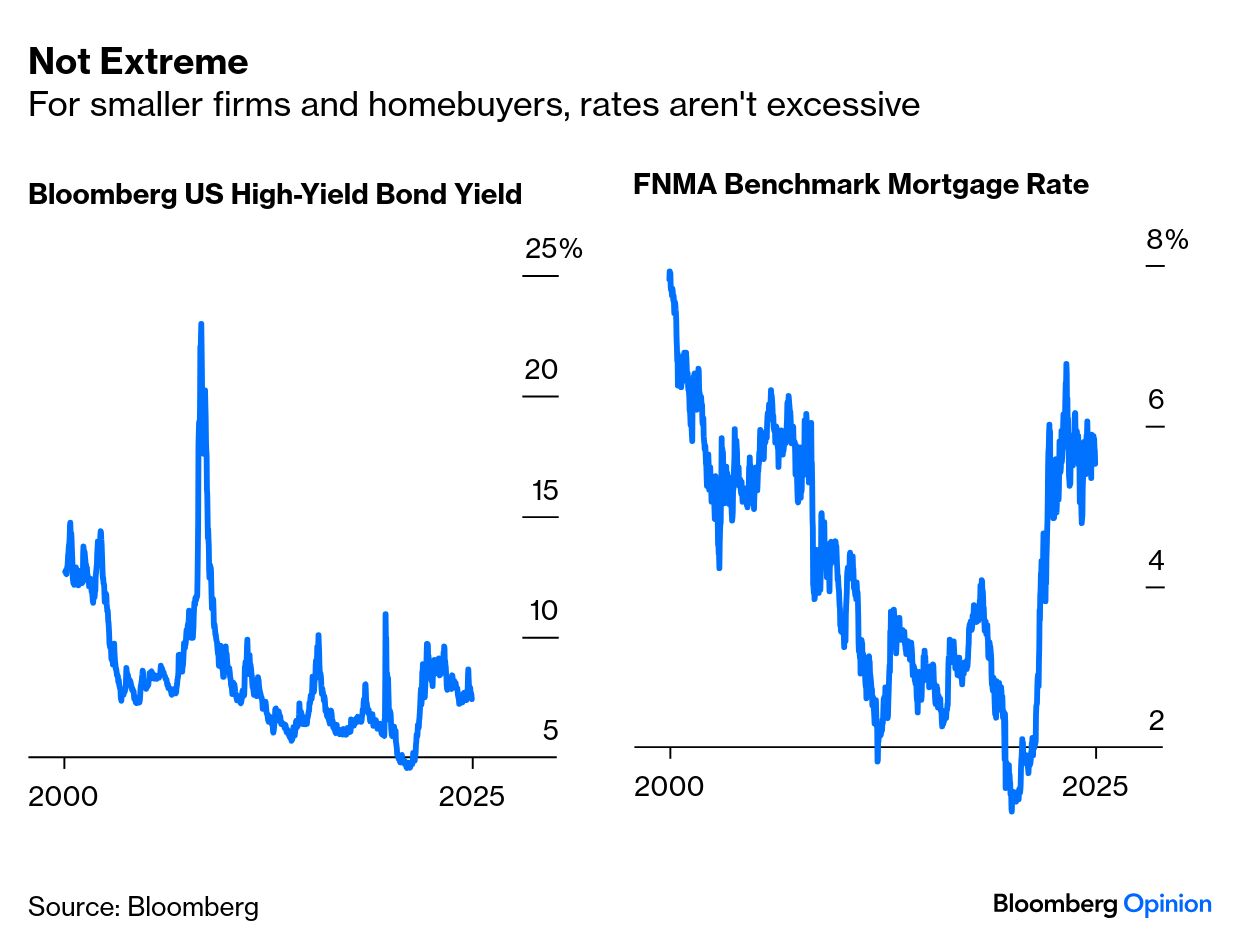

To make his point clearer, he added this illustration: Bully-boy tactics from this White House are not new. And Trump has a point. Points of Return showed two weeks ago that the Fed was increasingly an outlier among developed world central banks. Here, without the presidential Sharpie, is our own chart of the phenomenon: The post followed Sonali Basak’s interview with Scott Bessent for Bloomberg TV, in which he more diplomatically suggested that the Fed was burned by its terrible mistake in leaving rates low in 2021, igniting the worst round of inflation in two generations, and was “a little frozen at the wheel.” Politicians will always try to influence the Fed, but this administration’s tactics are growing subtler and cleverer. Firing Powell, who Trump appointed in his first term, would run into serious legal difficulty and fatally compromise any notion of the central bank’s independence. Trump threatened to do this two months ago (analyzed here) and swiftly backed down. But there are other ways to undermine Powell, and a number of plausible successors that Trump could nominate. The new idea is to name the next Fed chair this summer, to be confirmed months before Powell’s term ends next May. Powell would be a lame duck, and it would be his successor who set longer-term expectations. Powell may or may not quit in those circumstances, but it wouldn’t matter much — the Fed would be run by someone whose chief virtue was a willingness to cut rates. Though maybe not all the way to 1%. It’s clear that this has reduced the market’s estimate of where rates will go next year. A less independent Fed means less confidence in the dollar, which tanked on Liberation Day and is at a fresh three-year low: Bloomberg’s World Interest Rate Probabilities function shows futures predicting fed funds of below 3% by the end of next year, its lowest forecast since last September’s “jumbo cut.” This is a big divergence from the “dot plot” published two weeks ago by the Fed, which had the median FOMC member expecting three cuts fewer: The presidential assertion that a lenient Fed could bring government borrowing costs down to 1% doesn’t hold up to scrutiny. As has been clear for 20 years, central banks can control overnight rates but not 10-year bond yields. In the mid-2000s, Alan Greenspan moaned about the conundrum that the 10-year yield stayed stable as he hiked fed funds again and again — and last year, the 10-year greeted a one percentage point fall in fed funds with a one percentage point rise of its own: While 1% fed funds probably wouldn’t help the government finance its deficit, history suggests it would stoke inflation. Since 1990, there is only one instance of the rate dropping that low when core inflation is as high as it is now — in 2021, the year of the Powell Fed’s notorious “transitory” mistake. There are good arguments that the rate should be lower than it is now. There is no sensible case that it should be as low as 1%: Are current rates damaging? There are various ways to measure this, but again it’s hard to justify the Trumpian ire. To determine how tight a rate is, compare it to inflation. That could be done using the latest actual inflation number, or the breakeven bond market prediction for the next year. Or you could look at the 10-year TIPS yield, reflecting the rate borrowers will get above inflation. Those measures are laid out here. They agree that policy was way too loose in 2021. They also concur that the current real rate is a bit below 2%, which is on the high side but lower than rates on the eve of the Global Financial Crisis — when hindsight suggests they were too low: Is this hurting? Since Jimmy Carter, the “misery index” — the unemployment rate plus the inflation rate — has been a standard measure, which handily captures both sides of the Fed’s mandate. The US index is low, and below all major peers except Japan — and even there, the gap is closing. Rates aren’t hurting yet: Viewing financial conditions more broadly, including credit spreads and equity valuations to capture how hard it is to raise finance, again suggests that the Fed isn’t tightening the screws. Conditions are slightly easier in the euro zone, which has a weaker economy. Any number above zero suggests conditions are loose: And while rates seem high by recent experience, they are arguably only normalizing after years of artificial stimulus to tide the economy through after the GFC. That is true of mortgage rates, while the yields on junk bonds are unremarkably low even in absolute terms: Central bank independence is an eternally difficult subject. It’s hard to disagree that institutions so powerful should have some degree of democratic accountability. The administration’s attacks on Powell will age badly, and drastic cuts will only make sense if the economy lapses into recession. But in the short term, Trump 2.0 wants a weak dollar, and it’s achieving that beautifully. |