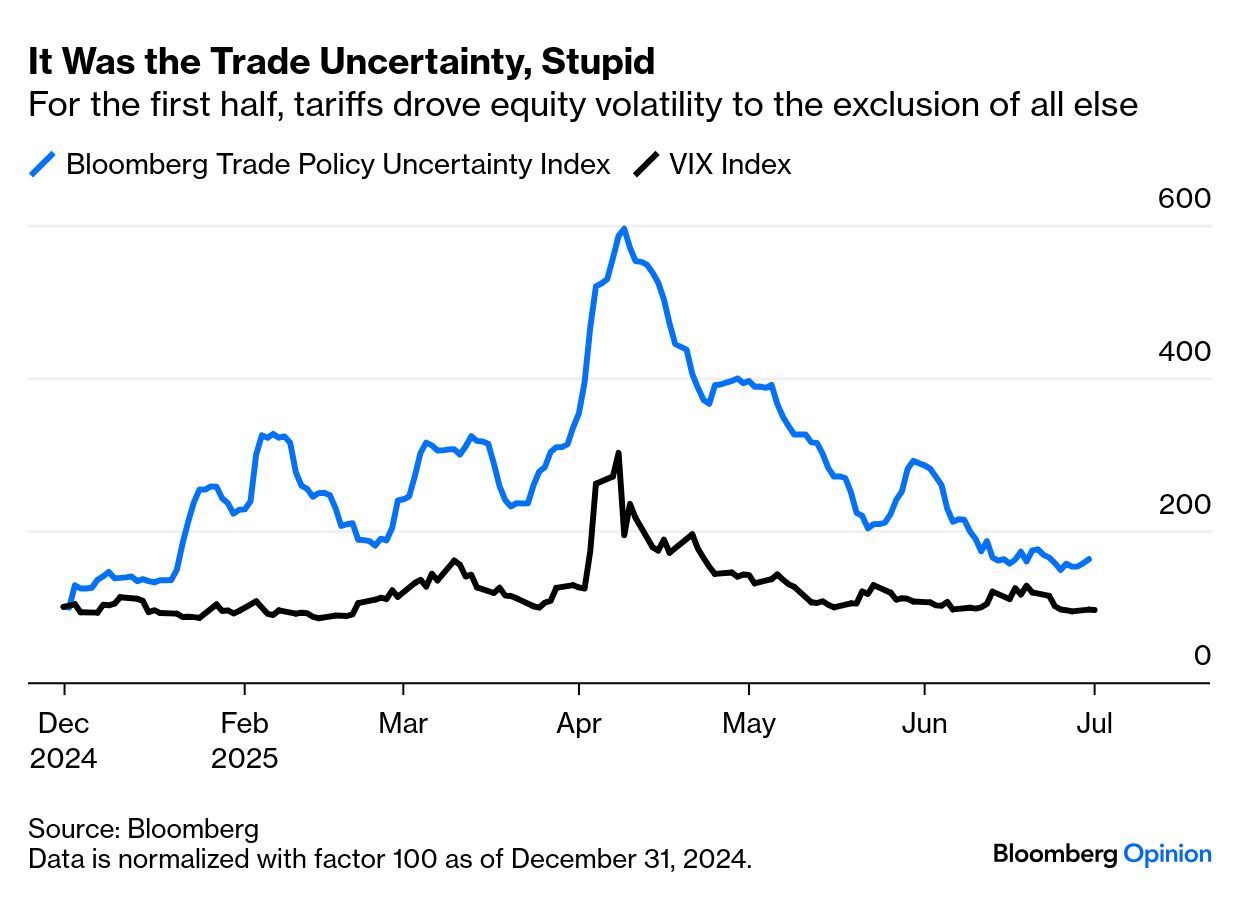

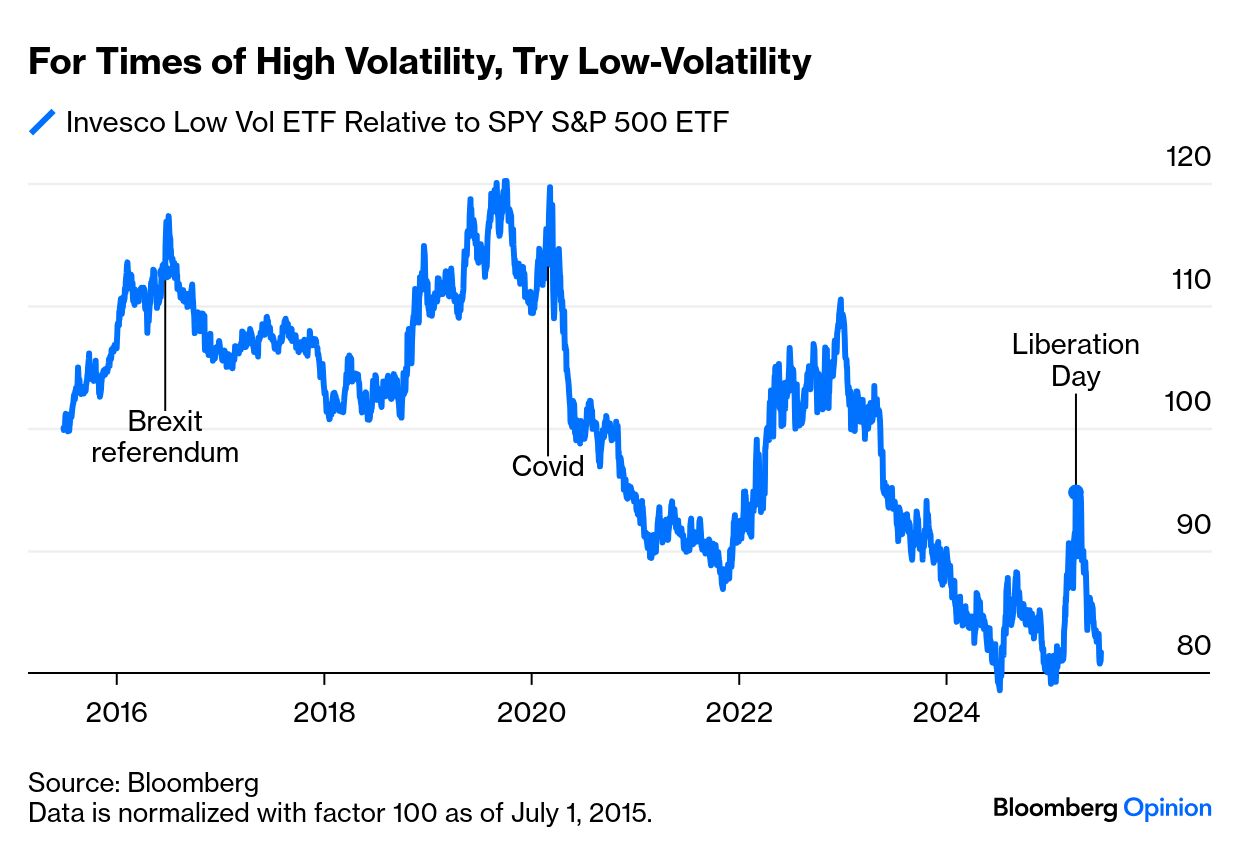

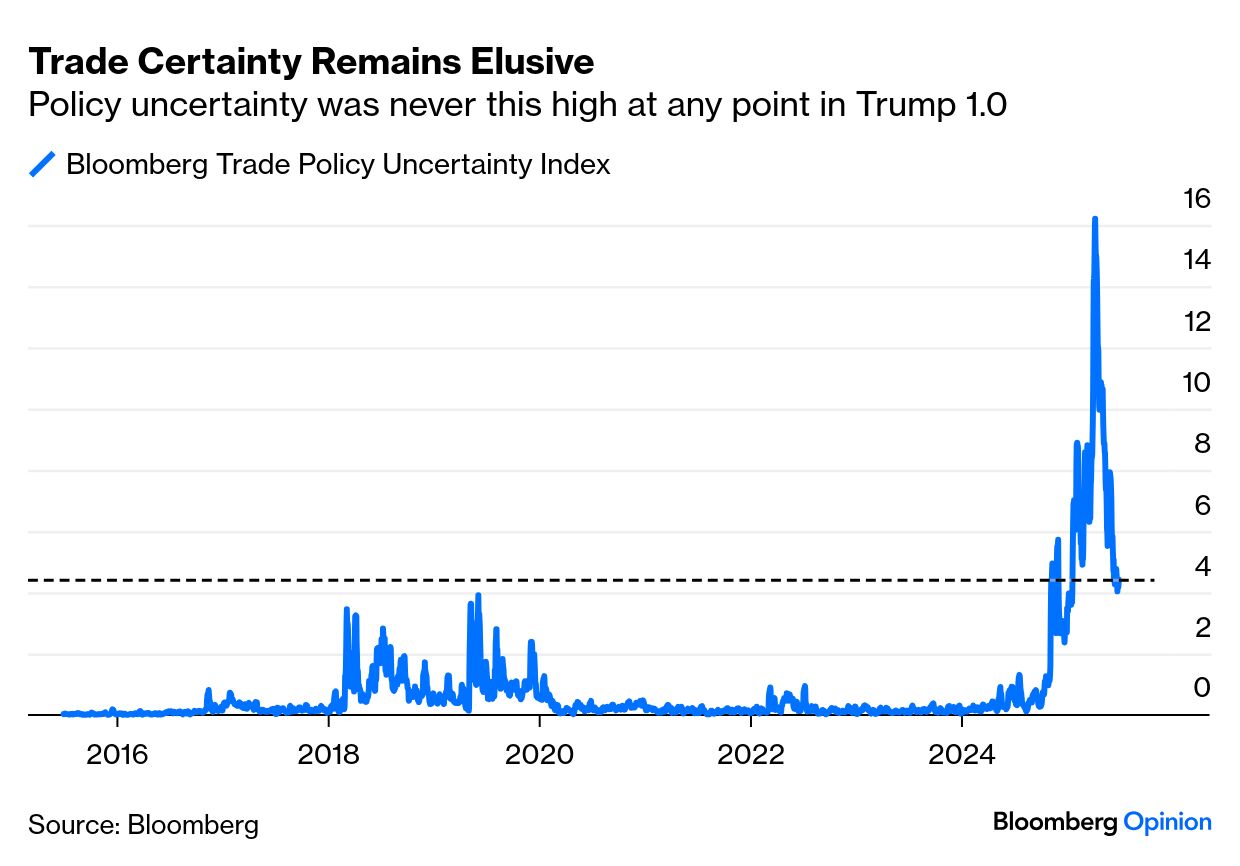

| Confusing data and political uncertainty notwithstanding, the S&P 500’s record has allowed the “end of US exceptionalism” narrative to take a break. But US stocks remain much more expensive, and global investors are still heavily overweight. With political risks souring US attractiveness, that will need to be addressed. Meanwhile, with indexes of equity volatility back down to normal, investors don’t stand to be compensated for enduring the next bout of market ructions: Bloomberg’s index of trade policy uncertainty, derived from the number of press reports, makes clear that tariffs have already driven one hefty dose of volatility: The weakening dollar, which Points of Return highlighted here, compounds the problem posed by the domination of US assets in many portfolios. Goldman Sachs’ Christian Mueller-Glissmann argues that the problem predates even Liberation Day (April 2), with the US peaking relative to the rest of the world at the turn of the year. Mueller-Glissmann argues that dollar weakness intensifies the need to rethink US asset dominance, which has also been driven by geopolitical risks. The answer, he suggests, is to focus on relatively low-volatility stocks, “which is like a defensive strategy”: It can be a very good way to moderate risk while staying invested, and essentially also free up risk budget to maybe own some of these more convex but more volatile parts of the market like tech and the Magnificent Seven. So, to some extent, the opportunity, if you want to sum it up in one word, is again diversification in the second half.

In general, as the name implies, low-volatility stocks provide a smoother ride, and outperform when volatility is spiking. Generally, over the last decade, they have underperformed. Invesco’s exchange-traded fund (ticker: SPLV) that tracks the S&P 500 Low-Volatility index has surged during times of high tension, but mostly dragged: The more fractious and divided world makes life that much harder, particularly as it can be difficult to track the specific exposure of multinational companies. Westwood Group’s Drew Miyawaki points out that this has turned into concrete policy moves such as the bipartisan No China in Index Funds Act. Geopolitical risk isn’t theoretical — but rather an isolated, independent factor requiring treatment like any other in portfolios. It also requires subtle analysis: The example we use to illustrate this is McDonald’s, a blue-chip US company that operated over 800 franchises in Russia. When Putin invaded Ukraine and Russia became uninvestible, McDonald’s had to forfeit those franchises and they took a $1.5 billion balance sheet hit. That’s an indirect risk that many investors didn’t quite understand they had. They just thought they owned McDonald’s, an American company.

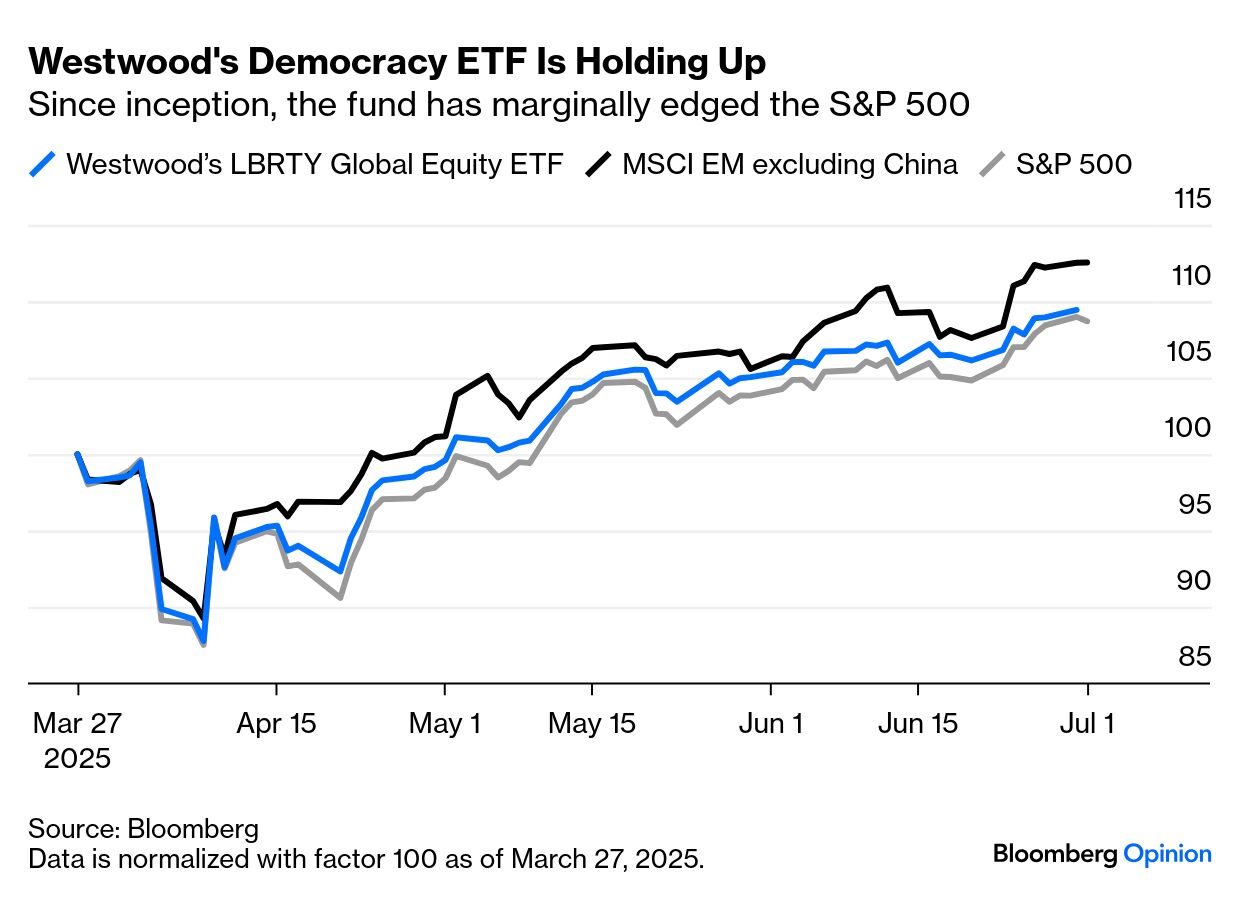

Eliminating all such risks would miss out on global exposure and create sectoral imbalances. There’s growing interest in screening international indexes to avoid such situations. In March, Westwood launched an ETF using a rules-based methodology to reduce direct and indirect exposure to authoritarian regimes, including China:

An older fund with a similar concept, the Freedom 100 Emerging Markets ETF, excludes countries with bad human rights records. It’s dominated by Chile, Taiwan, South Korea and Poland, and excludes China. So far this decade, it’s beaten the MSCI Emerging Markets index, occasionally lagging when China is doing well: Ultimately, market dynamics require investors to stay on constant high alert. Glenmede’s Jason Pride, in his outlook for the second half, adds that investors shouldn’t be lulled into complacency, nor should they be stunned into inaction. As a reminder, trade policy uncertainty remains very high: For now, there’s no need to take big risks in any direction. Rebalancing and diversification, as they always do, make more sense. —Richard Abbey |