Equities were unfazed on Monday by the recent commodities selloff as the already upbeat earnings season continued, with all major Wall Street indexes in the green. The S&P 500 closed higher, led by tech and AI companies, with Alphabet up 1.9% and Amazon up 1.5%. Both companies are set to report later this week, on Wednesday and Thursday, respectively.

European equities followed suit, with the pan-European STOXX 600 closing 1% higher, notching a new record high, thanks to strong gains in financial and healthcare stocks.

In tech news, Elon Musk announced Monday that SpaceX has acquired his AI startup xAI. The ambitious tie-up consolidates Musk’s space and AI ambitions and could boost SpaceX’s planned expansion into the data center business as it seeks to compete with AI heavyweights.

Investors will get a further taste of how the AI economy is faring when AMD and Supermicro Computer report today, alongside updates from consumer and pharma names including PepsiCo and Pfizer.

But they will have to wait longer for the JOLTS data originally slated for today, thanks to the partial government shutdown that began last Friday. January’s employment report, originally due Friday, will also be delayed until government funding resumes. Happily, the shutdown is likely to be brief, with lawmakers expected to vote today on legislation to end it.

In commodities, volatile precious metals seemed to find their level on Tuesday after the withering shakeout of recent days, with gold surging more than 5%, putting it on track for its biggest one-day gain since 2008. Despite the recent selloff, analysts say the precious metals bull run still has plenty of space to continue.

Oil continued to edge down on Tuesday as the geopolitical risk premium dissipated, due to the possibility of de-escalation in U.S.-Iran tensions. The two sides are gearing up for nuclear talks in Turkey on Friday. Oil fell more than 4% on Monday.

Meantime, President Trump on Monday announced a trade deal with India that would see New Delhi cease Russian oil purchases in return for a reduction in tariffs on Indian goods to 18% from 50%. Trump said India will instead buy oil from the U.S. and possibly Venezuela - alongside American arms and aircraft.

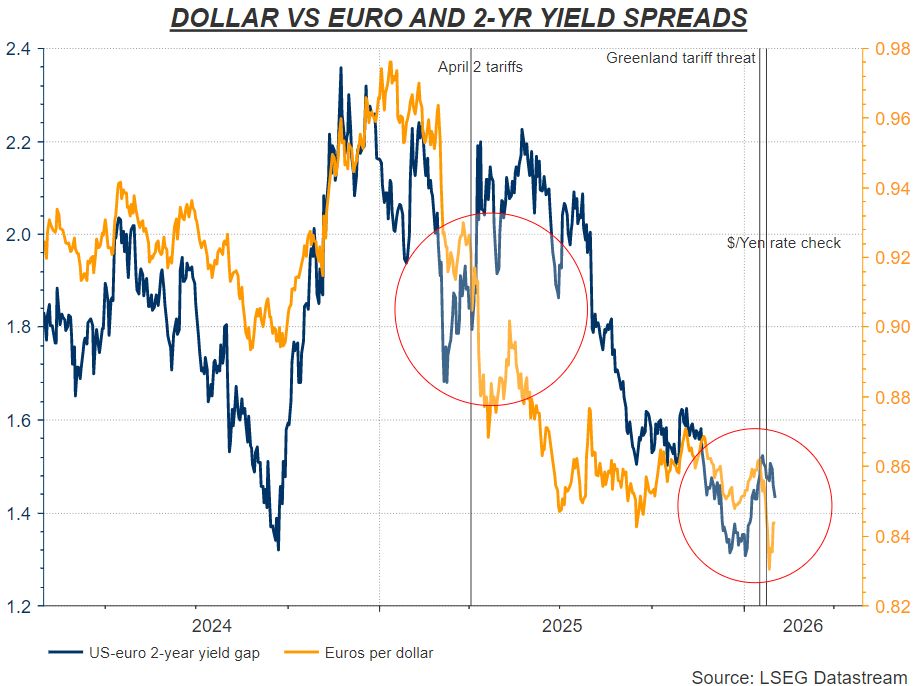

The dollar weakened a touch, but China's yuan reached its highest level in almost three years ahead of the Lunar New Year holidays.

Australia's dollar and bond yields all climbed after its central bank hiked rates for the first time in two years, with the Reserve Bank warning that inflation was likely to stay above target for some time.