|

|

|

|

Note to readers: Business Brief will pause for a holiday Monday and return next Tuesday. |

|

|

|

|

Good morning. Investor advocates are urging caution over the Ontario government’s push to open up more public access to private equity and debt. That’s in focus today – but first, let’s catch up on the dramatic shakeup at Canada’s third-largest telecommunications company. |

|

|

|

|

|

|

|

|

|

|

The news: Telus Corp. announced that retired Canadian Imperial Bank of Commerce chief executive Victor Dodig would replace long-time CEO Darren Entwistle, catching many off guard. |

|

|

|

|

|

|

|

|

|

|

The succession question: Of the many things boards of directors are responsible for, Kiladze writes, nothing matters more than succession planning. So, what did the board do for 14 years? |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Proponents of private market products for ordinary people say they would democratize access to investments that can far outstrip returns in the stock market. Paige Taylor White/The Canadian Press

|

|

|

|

|

|

|

|

|

|

|

Private markets for everyone |

|

|

|

|

Hi, I’m Erica Alini, personal economics reporter at The Globe. |

|

|

|

|

Ontario’s securities regulator has faced pressure from the government of Premier Doug Ford to green-light the creation of a new breed of mutual funds that would invest in privately owned companies and assets, my colleagues Clare O’Hara and Jameson Berkow recently reported. |

|

|

|

|

|

|

|

|

These mutual funds would invest in or lend money to companies that don’t trade on stock exchanges or borrow on public bond markets. They could also take ownership stakes in privately held assets, such as real estate, ports and bridges. |

|

|

|

|

Welcome to the world of private equity and private credit, until recently the rarefied domain of large investors, such as pension funds, and people with seven-digit savings accounts. |

|

|

|

|

Over the past five years, the Ontario Securities Commission has allowed financial firms to make private market products available to ordinary investors in only a few exceptional cases. But more recently, according to three people familiar with the process, the Ford government has pushed for the regulator to authorize private market mutual funds that could significantly broaden access to these types of investments. (The Globe has agreed not to identify the sources as they are not authorized to discuss the matter publicly.) |

|

|

|

|

The provincial government views the new mutual funds as a way to raise money for big infrastructure projects, according to the sources. But the idea has proven controversial. |

|

|

|

|

The sales pitch from the investment industry |

|

|

|

|

Proponents of private market products for ordinary people say they would democratize access to investments that can far outstrip returns in the stock market. They also argue the change would make new capital available for smaller Canadian companies that don’t have access to public markets. |

|

|

|

|

The warnings of investor advocates |

|

|

|

|

Investor advocates say that private asset mutual funds are riskier than traditional mutual funds and come with higher and more complex fees that are not clearly disclosed in advance. |

|

|

|

|

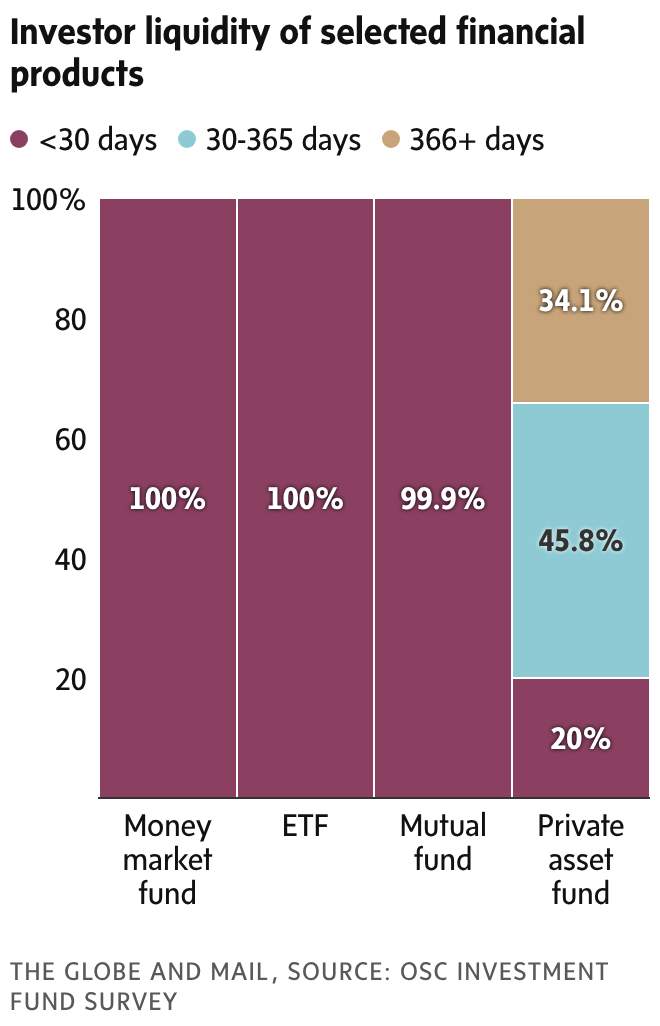

Another stark warning: Private funds are typically “illiquid,” meaning it can be hard for investors to cash in on their investments. That’s because it can take time for the fund itself to find buyers for the companies and assets it holds and generate the cash needed for large-scale payouts to investors. |

|

|

|

|

Private funds typically only allow investors to redeem a small percentage of their money at certain predetermined intervals. If too many investors want out at the same time, the funds can halt redemptions – sometimes for as long as several years. |

|

|

|

|

|

|

This isn’t an abstract scenario. Canada’s real estate market slowdown, for example, has caused a number of private funds holding real estate assets to pause investor redemptions. |

|

|

|

|

But so far, those halts have only affected institutional investors and wealthy individuals. |

|

|

|

|

There are also questions about whether private market returns are really as good as the industry says they are. The sources who spoke to The Globe, for example, said the OSC’s proposal to turn private asset funds mainstream was written hastily and contained little research corroborating the claim of higher returns. |

|

|

|

|

Many private equity firms snapped up companies and assets years ago, when interest rates were lower and the economic outlook rosier. Some of those firms are now struggling to sell what they bought at prices that would support the lofty returns they promised investors. |

|

|

|

|

Who offers private market products for ordinary investors right now? |

|

|

|

|

- Mackenzie Northleaf Private Credit Interval Fund. Started nearly two years ago, it’s a mutual fund that allows small investors to redeem up to 5 per cent of the money at three-month intervals. Mackenzie Investments is the only investment company in Canada that has obtained a regulatory exemption from the OSC for selling a private market fund to small investors.

- Wealthsimple Private Equity Fund and Wealthsimple Private Credit Fund.

Wealthsimple Investments uses a different exemption under current rules to offer private market investments to clients who have fully managed accounts. The funds are only available to investors for whom Wealthsimple believes the investment is suitable. On its website the company says qualification criteria include having at least $30,000 in investable assets and an investment horizon of at least three years.

|

|

|

|

|

The OSC said it has been contacted by more than 20 parties expressing interest in the new mutual funds, including investment fund managers, portfolio managers and industry associations. |

|

|

|

|

|

|

|

|

|

|

Instead of creating a whole new set of rules for private asset mutual funds, the OSC has opted for an ad-hoc approach, saying it will review applications for new funds on a case-by-case basis. |

|

|

|

|

|

|