Six weeks in, it's worth noting that the S&P 500 is still in the red for the year to date, the Nasdaq is down over 2%, and funds tracking the 'Magnificent Seven' mega-cap tech stocks are down almost 8% for 2026 so far. U.S. stock index futures were firmer ahead of Wednesday's bell, however.

In Europe, all the chatter centred on fresh reports that European Central Bank President Christine Lagarde plans to step down before her term ends in October 2027. The ECB said no decision had yet been made, but the original FT report said Lagarde was mulling the move to allow Emmanuel Macron and Friedrich Merz to influence the selection of her successor.

European markets were calm on the news as these reports have been doing the rounds for some time. In any case, steady ECB policy looks baked-in for the foreseeable.

But there will inevitably be focus on the political decision over Lagarde's successor - whether Germany may break with convention and claim its right to have a Bundesbanker head the ECB for the first time, or whether a compromise candidate like BIS boss and former Bank of Spain chief Pablo Hernández de Cos is more likely.

If a German ECB president emerged, markets may, at the margin, bet on a more hawkish trajectory over the horizon.

Elsewhere, UK inflation fell to 3%, as expected, keeping speculation about another Bank of England rate cut next month on the boil. Sterling was unmoved.

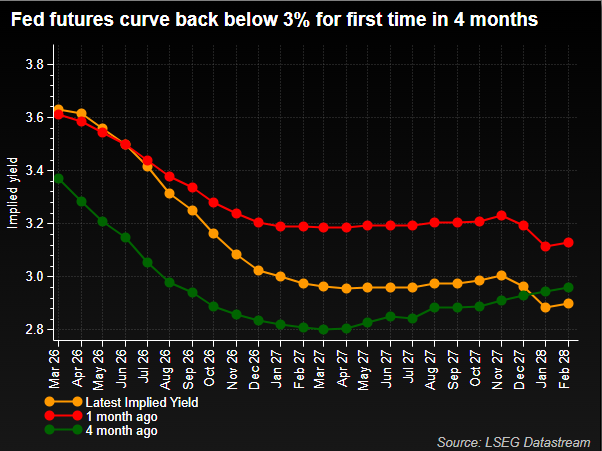

The main focus of the macro world later will be the FOMC's release of minutes for its January meeting - usually a relatively anodyne readout, but one that could take on more significance amid debates around AI's impacts on productivity and inflation going forward.

In geopolitics, Iranian Foreign Minister Abbas Araqchi said on Tuesday the U.S. and Iran had reached an understanding on "guiding principles" in nuclear talks. The prospects of a final deal remain uncertain, however. Oil prices trimmed some losses after falling around 2% on Tuesday.