An unexpected beneficiary of the Iran war? Maritime shipping intelligence platforms. The owners of MarineTraffic, an app that provides real-time ship movement and location data in harbors and ports, has gained millions of new users since the conflict began, and many of them are paying a premium, meaning the app’s top line has been floating straight up.

Stocks fell from record highs on Tuesday, with the S&P 500, Nasdaq 100, and Russell 2000 all trading lower as the AI trade was dragged down by a Wall Street Journal report on OpenAI (more on that below). |

|

|

|

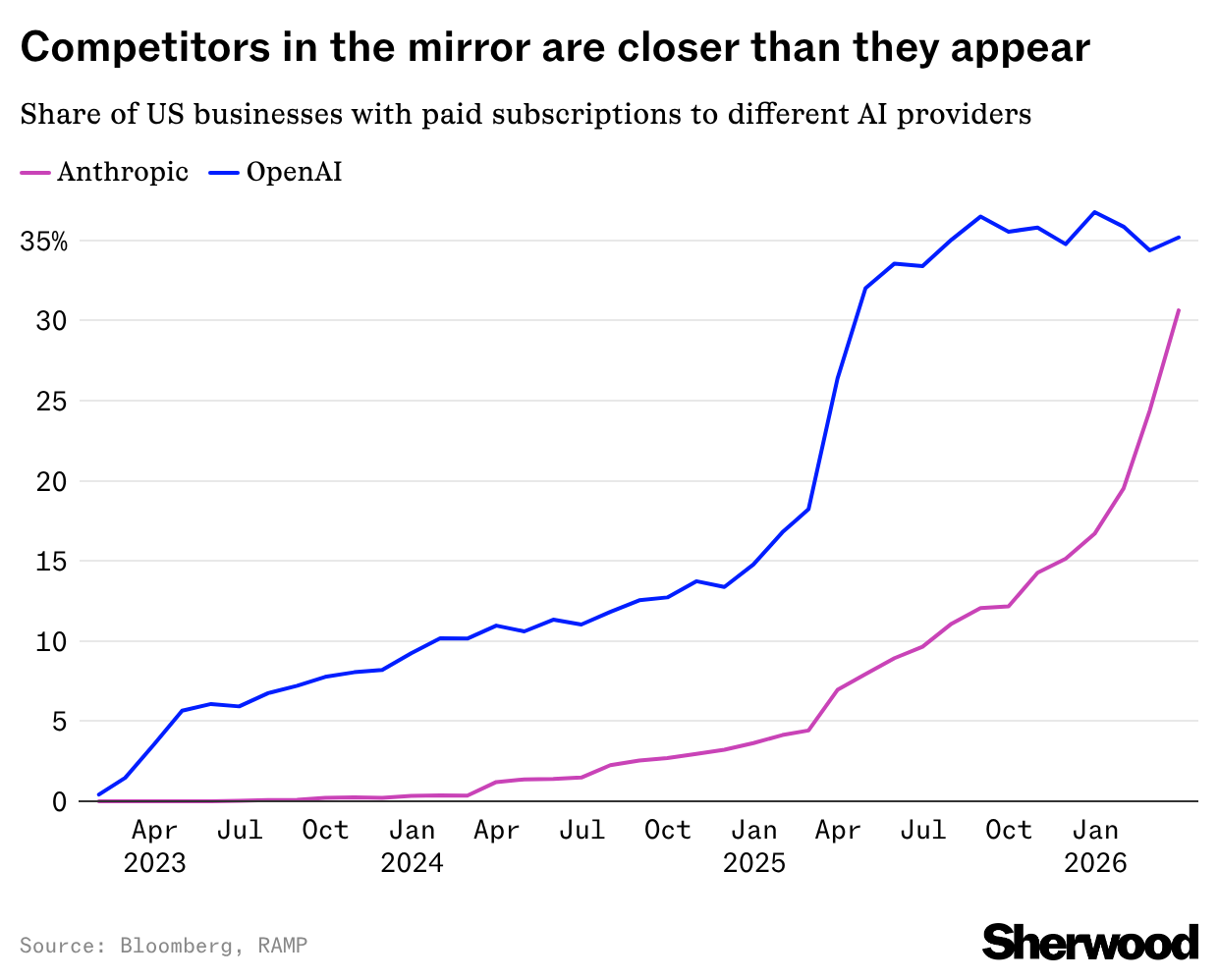

“Did 2025 end badly for OpenAI?” is the wrong question. Here are the 2 questions that do matter. |

OpenAI once again weighed on a raft of its suppliers and partners after The Wall Street Journal reported that the company has missed a number of internal revenue and user targets, as its competition with Anthropic and others heats up.

The goals missed reportedly include a target to hit 1 billion weekly active users by the end of 2025, its annual revenue target for ChatGPT last year, and multiple monthly revenue targets this year, as Anthropic has surged ahead in the enterprise markets. So, where to from here?

|

-

We spent the final two months of 2025 punishing stocks for being close to OpenAI, and until April, those names remained in the penalty box, lagging the Nasdaq 100 and significantly trailing Google-linked stocks.

- What really matters? Does OpenAI understand why it lost market share among enterprises, and can OpenAI compete on quality? Solve those two questions, and this is just a rough patch. Fail to, and no amount of compute can solve its issues.

-

Most of OpenAI’s internal and external communiques in 2026 have taken care to spotlight the growth of Codex (its AI coding tool) and how enterprise revenues are gaining ground on consumer sales within the firm. This appears to be a company that’s better balancing the need for enterprise depth to go along with its consumer breadth.

|

One thing OpenAI does have going for it is that the best ability is availability. OpenAI has sought to make this a key differentiating and selling point relative to Anthropic. The Claude developer has been bedeviled by complaints about use limits and is in the midst of a mad scramble for compute that’s seen it strike or expand deals with CoreWeave, Amazon, Google, and Broadcom over the past month.

|

|

|

|

Commoditization might sound like a bit of a dirty word, or like it’s devaluing the impact of a potentially revolutionary technology. But at its essence, all we’re describing here is the ability of AI tools to produce a (roughly) standardized and reliable output: you don’t think twice about whether the gas you’re putting in your car at Exxon Mobil will be any better or worse than Shell’s. Both get you where you want to be.

To tie these two points together: if Exxon Mobil is closed and Shell is open, well, then there’s really no choice for whose fuel you’ll be using. |

|

|

|

A New Entrant To The Royalties Race? |

For decades, three names have owned the gold royalty sector. There has never been a credible fourth — but Versamet is positioning to take the spot. Led by a team that has already built and sold a gold royalties company from the ground up, Versamet (Nasdaq: VMET) is a rapidly growing precious metals powerhouse.

Here’s the math: Versamet acquires royalties and streams on world-class mining projects, which return revenue as attributable Gold Equivalent Ounces (GEOs). More GEOs mean more cash flow to fund new deals, creating a compounding growth effect. After nearly doubling 2024 GEOs to ~9,815 in 2025,1 Versamet projects a jump to 20,000–23,000 GEOs by the end of 2026,2 representing 4x growth in just three years. As gold continues to gain structural strength, the company could be entering a major inflection point in its growth curve. And with an average mine life of 15 years across the portfolio, Versamet (Nasdaq: VMET) has a long-term cash flow duration that can provide a stable foundation of underlying value.

Get diversified gold exposure with Versamet. |

|

|

|

The 6 biggest US airlines spent $1.2 billion more on fuel in Q1, and things are about to get worse

|

Collectively, the country’s six biggest carriers spent about $1.2 billion more on fuel in the quarter that ended in March than in Q1 of 2025. Given this year’s first quarter included only one month of the war in Iran, things are likely going to get worse. |

- Carriers expect to pay about $4.26 per gallon for jet fuel in Q2, up from $2.80 in Q1.

-

Looking ahead, carriers expect the seat belt sign to stay on. Delta Air Lines forecast a $2 billion hike to its Q2 fuel bill, and Alaska Air guided for an increase of “$600 million or more.”

- As recent flyers will know, airlines have been making attempts to “recapture” fuel costs through higher fares, fewer flights, and the hiking of bag fees in recent weeks. Still, those efforts are slow-going and need to be carefully done to have the lowest impact on demand.

-

“To state the obvious, the best type of fuel recapture is not to purchase the fuel in the first place,” Delta CEO Ed Bastian said on the company’s earnings call earlier this month. The company said it expects to recover up to half of its higher fuel costs in the quarter.

|

| |

|

Per United CEO Scott Kirby, to recover the full amount of higher fuel costs, the carrier would need to earn between 15% and 20% more per passenger.

“As yields increase, there will be an elasticity effect on demand, [which] we’re estimating will lead to less overall demand,” said Kirby. “While we haven’t actually seen that decline yet, Econ 101 makes us believe it’s coming.” |

|

|

|

Meta could be getting ready to post its highest revenue growth since 2021 |

When Meta reports first-quarter earnings today after the bell, analysts and Meta itself expect that its revenue could rise more than 30% compared to the same period last year — the company’s biggest year-over-year jump since 2021. Meta is even expected to surpass Google in one key revenue stream.

|

|

|

|

|