In March, we argued that the recent rise in Chinese RMB payments internationally, and the movement in such payments from the Western SWIFT system to China’s Cross-Border Interbank Payment System (CIPS), was being driven by efforts to avoid the reach of U.S. financial sanctions. Were we right?

In this post, we provide some evidence from ongoing world events.

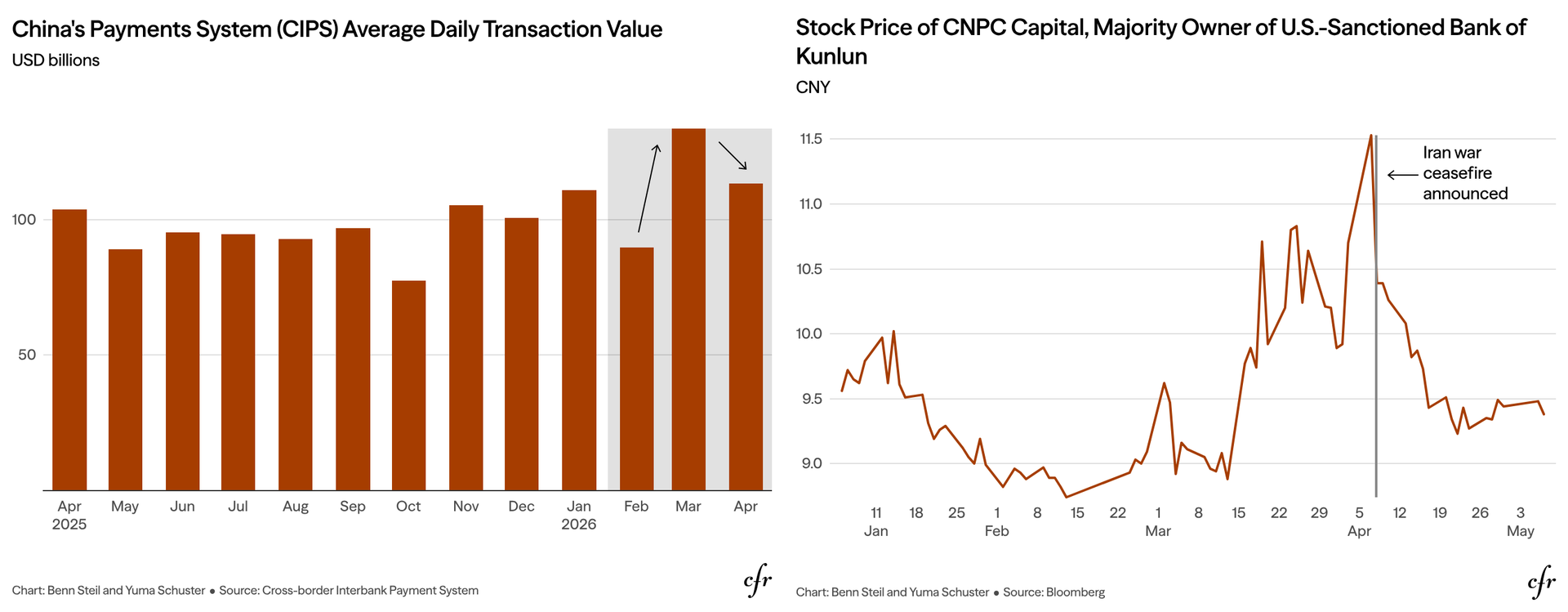

As shown in the left-hand graphic above, CIPS volumes spiked in March, just after the U.S. attacks on Iran. And as the right-hand graphic shows, there was a simultaneous spike in the stock price of CNPC Capital—the majority owner of the U.S.-sanctioned Bank of Kunlun. Both phenomena appear consistent with reports of Iran demanding large RMB toll payments in the Strait of Hormuz together with renewed U.S. threats to sanction countries aiding or trading with Iran. Payments that would normally have been routed in dollars through SWIFT now took place in RMB through CIPS. And traders marked up the value of Chinese financial institutions, such as CNPC Capital, able to operate outside the dollar system.

What happened after the U.S. ceasefire announcement on April 7 was equally revealing. The graphics show that CIPS volumes fell in tandem with a sharp drop in CNPC Capital’s share price. Both were signs of the market returning to the dollar-based status quo ante.

The message for the Trump administration is both comforting and worrying—comforting in that the market still prefers doing business in dollars, worrying in the sense that China’s alternative is increasingly seen as cost-effective and reliable.

Geopolitically, dollar sanctions function like powerful antibiotics—highly effective when used selectively, but less so when repeated use encourages development of resistant alternatives.

Ironically, the RMB’s appeal in sanctions-sensitive trade may derive less from its independence from the dollar than from its linkage to it. China’s managed currency, much like a dollar stablecoin, can offer much of the dollar system’s benefits with reduced exposure to U.S. sanctions.