The Week in Breakingviews |

|

| |

|

The Week in Breakingviews |

|

| |

| Insights from Reuters global financial commentary team |

|

|

|

By Peter Thal Larsen, Global Editor

|

|

|

|

Welcome back! Donald Trump and Xi Jinping both concluded that the U.S. president’s trip to Beijing was a success, but it’s far from clear what else, if anything, they agreed on. What is certain is that the Strait of Hormuz is still mostly closed, and American equity investors don’t seem to care. Let me know what you think. If this newsletter was forwarded to you, sign up here to get it in your inbox every weekend.

Note: Links in this newsletter require a Breakingviews subscription. To sign up for a free trial, click here. |

|

|

“No people whose word for ‘yesterday’ is the same as their word for ‘tomorrow’ can be said to have a firm grip on the time, Salman Rushdie once wrote in a friendly dig at Indians in reference to the Hindi language.” Read more: India’s forex-saving push is late, and pre-emptive. |

|

|

|

Five things I learned from Breakingviews this week |

|

|

|

A U.S flag is seen at the New York Stock Exchange in New York City, U.S., November 6, 2020. REUTERS/Carlo Allegri |

An ever-present pitfall for those who write about finance is the premature obituary for a market trend. It can be tempting to confuse a turning point with a wobble which registers as a barely noticeable blip in an upward line. No investment craze received more untimely epitaphs last year than American exceptionalism: the tenacious tendency for the U.S. stock market to outperform its rivals around the world. Indeed, the first edition of this newsletter in September questioned how long this trajectory could last in the face of Donald Trump’s attacks on global trade, weaponisation of the judicial system, and meddling with private companies. (See Exceptional no more.)

As it happens, American exceptionalism is not only alive but kicking. Despite the continuing blockade of the Strait of Hormuz, U.S. stocks are on a tear. The S&P 500 Index is up more than 16% in the seven weeks since March 27, easily beating all major benchmarks apart from chip-mad South Korea. Asked to predict which asset class will produce the best performance this year, investors now invariably choose U.S. equities. Overseas fund managers who spent 2025 diversifying their exposure to the world’s largest economy are piling back in.

The reversal has some logical foundations. Companies reported robust growth in the first quarter, and it was not all due to artificial intelligence. As Sebastian Pellejero points out, even after excluding the “Magnificent Seven” tech giants, earnings for the remaining members of the S&P 500 are growing at their fastest rate in more than four years. Corporate profit margins continue to defy gravity.

|

|

|

|

Rising prices, the elevated cost of oil, and higher-for-longer interest rates may end the party. For now, though, public market investors are showing few signs of restraint, especially for anything AI-related. Shares in Cerebras Systems almost doubled on their first day of trading on Thursday, valuing the maker of chips for chatbots at more than $100 billion. The company was even able to brush away a takeover approach from SoftBank’s Masayoshi Son, that serial chaser of tech fashions. And this is just a warm-up for the much larger initial public offering of Elon Musk’s SpaceX. (See The summer of SpaceX.)

Investors who lived through the dotcom bubble are having flashbacks to 1999. But even if the analogy holds, timing matters. The defining IPO of that era was Netscape, the web browser company whose shares doubled on their first day of trading in 1995. The S&P 500 Index went on to record double-digit gains in each of the next four years. Just because a trend is unsustainable does not mean it’s time to dust off the obituary. |

|

|

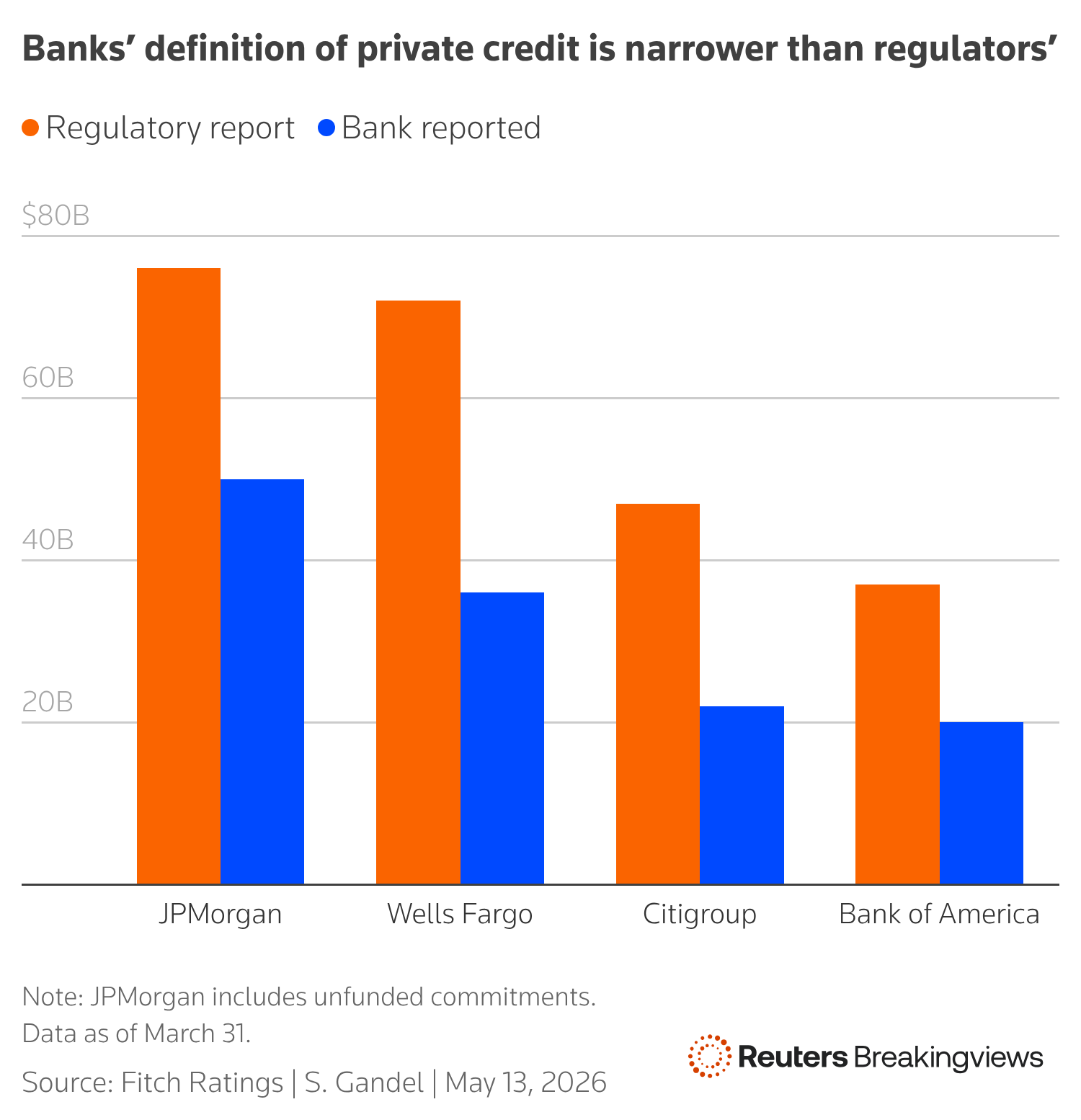

Financial regulators worry about banks’ exposure to private lenders. Bank executives say it’s not a big issue. Refereeing this debate would be easier if the two sides agreed on the numbers. That’s not the case. Filings with the Federal Deposit Insurance Corporation suggest much more active lending than the banks’ own disclosures. The discrepancy itself is a cause for concern, Stephen Gandel writes.

|

|

|

|

For an early read on what artificial intelligence is doing to white-collar service jobs, the best place to look is India, where many large companies have back-office centres. Shritama Bose joined Aimee Donnellan and Una Galani in the Viewsroom to talk about why the country is vulnerable to “AI deflation”, and how this trend may play out elsewhere.

Over on The Big View, I took a break from knotty financial and economic issues to consider a more existential question: people in developed countries are materially better off than ever, so why are they so dissatisfied? I talked this over with Ryan Avent, the author of “In Good Faith: How the Nature of Belief Shapes the Fate of Societies”. |

|

|

|

|