| Welcome to Next Africa, a twice-weekly newsletter on where the continent stands now — and where it’s headed. Sign up here to have it delivered to your email. Nigeria’s fortunes appear to be looking up after nearly two years of painful economic reforms that triggered a cost-of-living crisis. Improved security in its main oil-producing region has boosted earnings from crude, which generates about 80% of foreign-exchange inflows. Daily output averaged 1.54 million barrels in January, a four-year high and exceeding the West African nation’s OPEC+ quota.  Nigerian President Bola Tinubu. Photographer: Hollie Adams/Bloomberg The pickup in revenue has helped stabilize the naira that plunged about 70% against the dollar since June 2023, when the central bank started allowing it to trade more freely. Investors have taken note. The extra yield they demand to hold the country’s dollar debt has fallen to a five-year low. And the main stock index is up 11% since the beginning of December, triple the gain posted by the MSCI developing-world equities index. Nigeria, meanwhile, looks set to regain the mantle of Africa’s biggest economy (it currently ranks fourth) when the national statistics agency releases rebased figures next month. Gross domestic product is expected to be revised upward to almost $500 billion. The release of overhauled inflation data on Tuesday was another boon. The measure fell to 24.5% from almost 35% a month before. That could offer the central bank scope to trim its key interest rate when it meets on Thursday, giving consumer spending and the economy another lift.

The good news hasn’t come a moment too soon for President Bola Tinubu, whose attempts to steady the government’s finances have sent food and fuel prices soaring, and exacerbated hardship in a country where more than half the population lives below the poverty line. Challenges remain to keep up the momentum, but the long-flailing economy does have a far better look. — Anthony Osae-Brown Key stories and opinion:

Investors Bullish on Nigerian Assets as Reforms Boost Confidence

Nigeria Central Bank Chief Says Naira Reforms Enticing Investors

Can Nigerians Bear Pain of Economic Shock Therapy?: QuickTake

Nigeria’s Oil Comeback to Test Its Commitment to OPEC+ Cuts

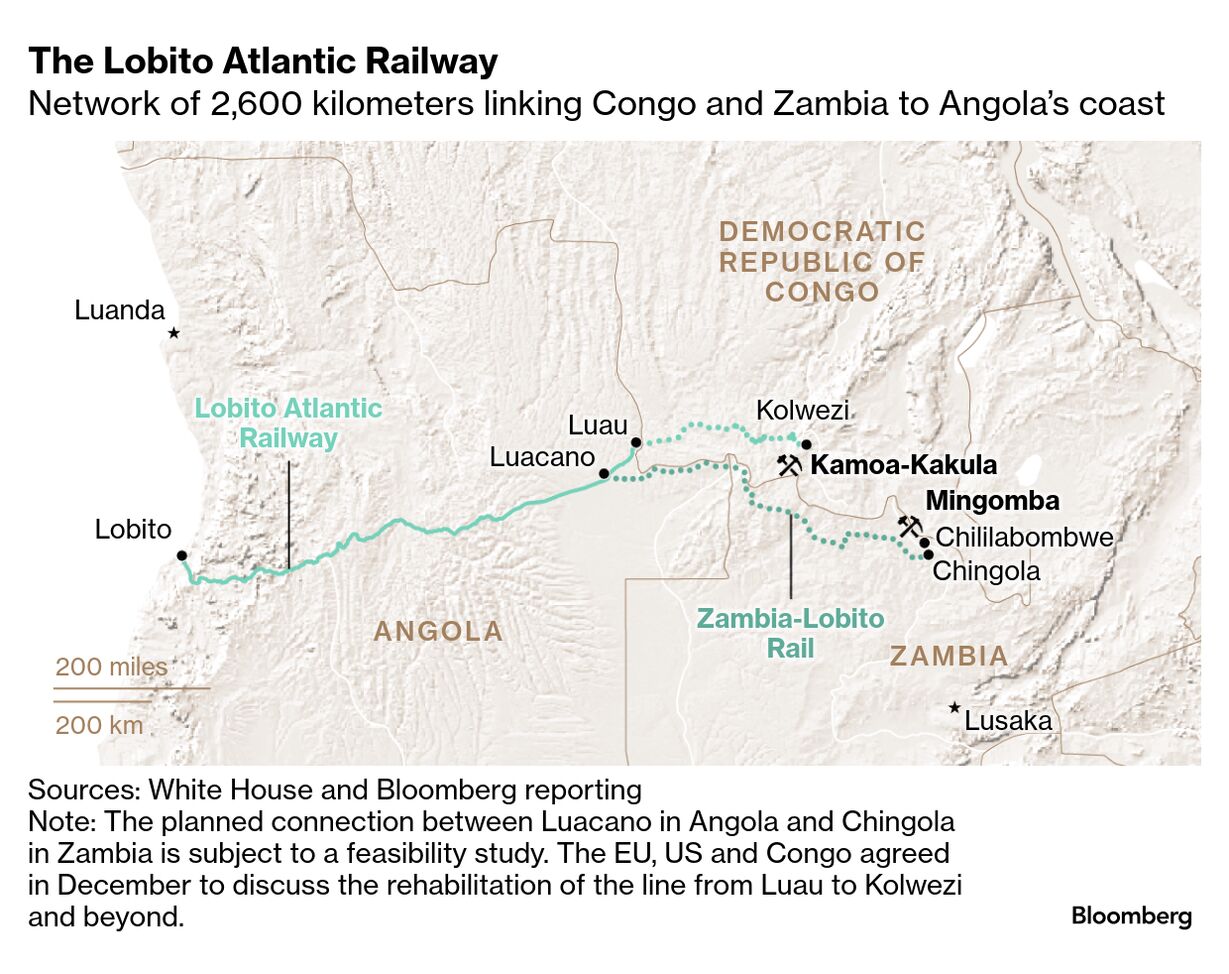

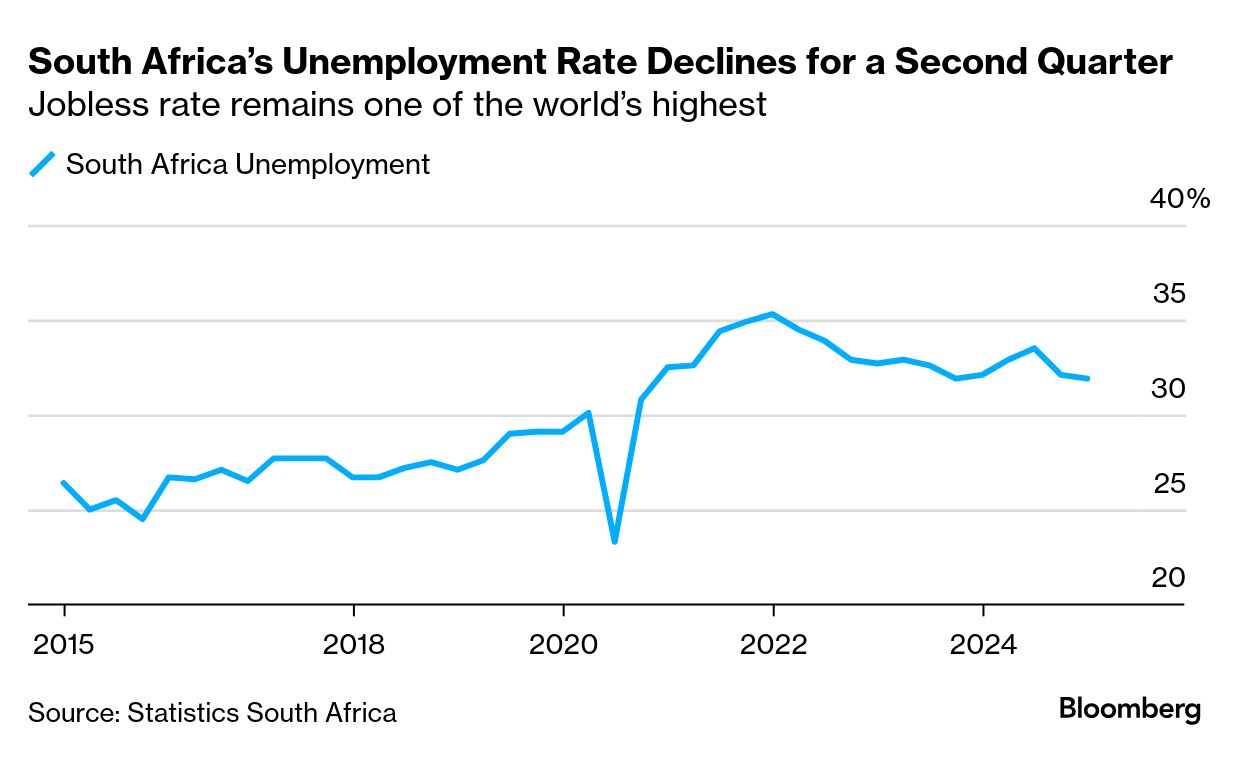

Nigeria Joins BRICS Group as Partner State to Boost Investment Rwanda-backed militants seized Bukavu in eastern Democratic Republic of Congo, tightening control of the mineral-rich region. Videos of M23 troops entering the city center were posted on social media, hours after Congolese President Felix Tshisekedi claimed the army was in control. The fall of the hub means M23 controls all of eastern Congo’s border with Rwanda along Lake Kivu. The government says Rwanda and the rebels plan to maintain their occupation, heightening concerns of a regional war.  Congolese soldiers drive through the streets of Bukavu on Feb. 14. Photographer: Amani Alimasi /AFP/Getty Images US forces carried out an airstrike against Islamic State insurgents in northeastern Somalia on Sunday, the second such attack this month. Two militants were killed in the raid, which was carried out in coordination with Somalia’s government, according to the US Africa Command. It said that at least 14 IS operatives died in a Feb. 1 attack, including Ahmed Maeleninine, a key financier of the group. A billion-dollar expansion of the biggest US strategic critical-minerals project in Africa faces delays because of the Trump administration’s sweeping aid freeze, providing a potential opening for rivals like China. The Lobito corridor railway project is meant to ferry minerals from the Central African copperbelt to the Angolan coast for export to the West. It’s among mining and energy developments across the continent that have been pledged funding from USAID. Officials and developers now fear disruptions. Pravind Jugnauth, the former prime minister of Mauritius, was briefly detained in connection with a money-laundering investigation. The ex-premier, who denies wrongdoing, is the second high-profile member of the previous administration to be taken into custody since it lost November elections. Harvesh Seegolam, a former central bank governor, was held last month before being granted bail. He was provisionally charged with conspiracy to defraud. Warring factions in Sudan’s two-year civil war are forming parallel governments, a move that may lead to a Libya-style split of the devastated North African nation. A coalition of Sudanese political entities is establishing a new “peace and unity government” allied with the Rapid Support Forces paramilitary group, according to Ezzadean al-Safi, a political adviser to RSF leader Mohamed Hamdan Dagalo. The announcement comes after army chief Abdel Fattah al-Burhan said he’s preparing to unveil a new “democratic political bloc” to govern the country.  Members of the Beja pro-army militia in Port Sudan in October 2024. Photographer: Eduardo Soteras/Bloomberg Zimbabwean President Emmerson Mnangagwa said he will retire when his current term ends in 2028, rebuffing a ruling party proposal to extend his tenure until 2030. The 82-year-old has led the southeast African country since long-time ruler Robert Mugabe was toppled in a military coup in 2017. Some officials in the Zimbabwe African National Union-Patriotic Front have been lobbying for the constitution to be amended to enable Mnangagwa to extend his stay in office. Thank you for your responses to our weekly Next Africa Quiz and congratulations to Evans M. Munyoki who correctly identified Malawi as the African country that temporarily banned mineral exports. South Africa’s unemployment rate edged down in the fourth quarter as the finance and manufacturing industries added jobs. The second consecutive decline in joblessness bodes well for the nation’s coalition government that was formed after the African National Congress lost its parliamentary majority in May elections. The so-called government of national unity has made lifting economic growth and reducing unemployment its top priorities. Thanks for reading. We’ll be back in your inbox with the next edition on Friday. Send any feedback to mcohen21@bloomberg.net |