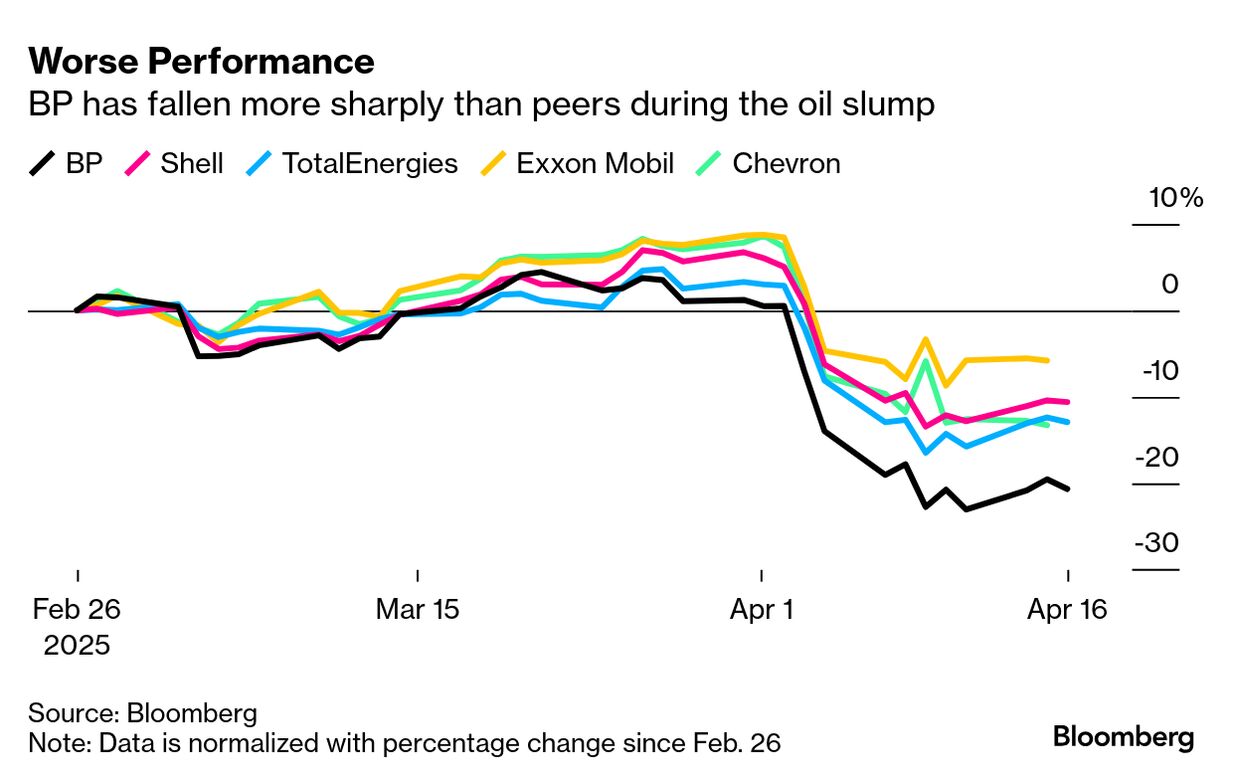

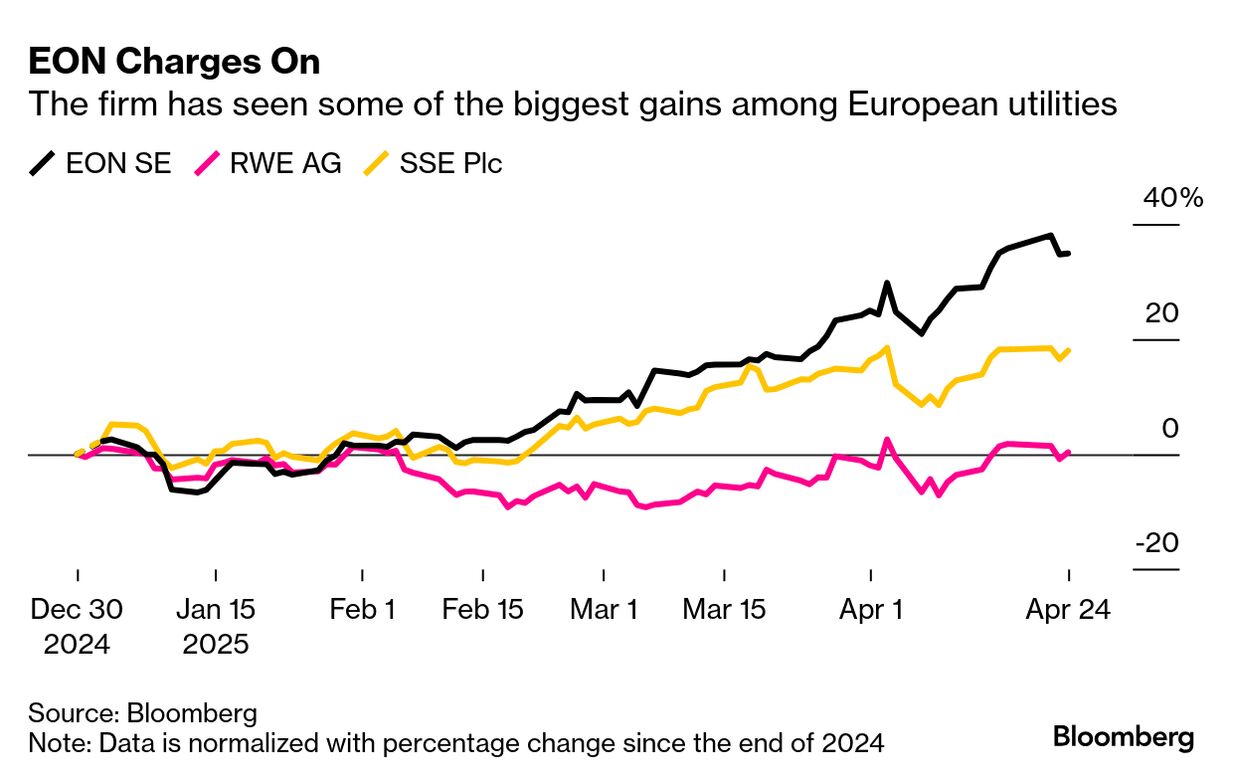

| By Natasha White As Elliott Investment Management pressures BP Plc to abandon its renewable-energy ambitions, ESG fund managers can’t agree on how to treat the UK oil giant. BP’s pledge to beef up investments in oil and gas — and slash its commitments to renewable energy — has coincided with ESG fund inflows into the company of $200 million since late February. ESG fund outflows from BP, meanwhile, were $315 million, resulting in net withdrawals of $115 million, according to data compiled by Bloomberg. Read More: BP’s Crisis Marks the Tombstone for Big Oil’s Green Pivot Money managers who say BP still belongs in an ESG portfolio include Legal & General Investment Management, which added BP to its Climate Action Global Equity fund in September and has held on to the stake despite the company’s pivot away from its climate commitments. “We’ve seen some backpedalling,” said Nick Stansbury, manager of the fund and head of climate solutions at Legal & General. “But that is in the context of an awful lot of backpedalling everywhere else.” Stansbury said that “what matters isn’t only the absolute sustainability performance of a company, but its performance relative to other companies.” Elliott has now built up a stake in BP to just over 5%, making it one of the oil major’s biggest investors along with BlackRock Inc. and Vanguard Group Inc. Elliott has made clear it wants BP to return to its core oil and gas business as part of a strategy to generate $20 billion of annual free cash flow by 2027. Against that backdrop, BP has embarked on a major pivot within its energy strategy. The company said on Feb. 26 it was abandoning earlier transition plans, and will instead seek to increase investment in oil and gas to about $10 billion a year. It also plans to reduce annual investment in low-carbon energy to $1.5 billion to $2 billion, which is roughly $5 billion less than BP’s previous guidance. “Companies that pursue fossil-fuel expansion projects in the midst of a climate crisis are jeopardizing our future,” said Julia Dubslaff, finance researcher at Urgewald. “Their presence in ESG funds violates the very concept of sustainability.” Yet since BP’s announcement, more than 60 funds that commit to a sustainability objective in their prospectus have added to their existing stakes in the company, according to data compiled by Bloomberg. A further six such environmental, social and governance funds invested in BP’s stock for the first time. The ESG fund industry has long struggled to reach a consensus on how to handle fossil-fuel companies. Many fund managers tout years-long engagement strategies they say will ultimately drive oil and gas producers to decarbonize. But the retreat from climate goals by BP and other oil majors indicates those efforts are having little impact. Natalie Stafford, head of ESG and sustainability at S-RM, a consulting firm, said BP’s climate pullback “represents a period of proper reflection,” which isn’t “necessarily a bad thing.” The company’s earlier climate pledges smacked of “green grandstanding,” she said. The oil and gas industry “hasn’t done a great job of investing in pure-play renewables,” Stansbury said. “But there’s lots and lots of other places in a low carbon energy system for them to play in.” Which ESG fund made the biggest purchase of BP shares in the past few months? Read the full story on Bloomberg.com to find out. Hedging their clean energy bets | By Ishika Mookerjee and Sheryl Tian Tong Lee As President Donald Trump takes a hatchet to the clean-energy transition, a number of hedge funds are trying to figure out how to make money on low-carbon investments that appear resilient to White House attacks. Hedge fund managers interviewed said their strategy doesn’t entail shunning the US altogether, but most said they now see better opportunities in Europe and Asia, focusing on utilities and grid-equipment providers. Per Lekander, chief executive of $2.7 billion London-based hedge fund Clean Energy Transition LLP, said he’s long Germany’s EON SE and RWE AG, as well as UK-based SSE Plc, because “they’re entirely domestic and quite cheap.” EON, which is one of Europe’s biggest distribution grid operators and a key plank in the bloc’s efforts to electrify its power supply, is up about 35% this year. Similar gains are playing out across European utilities, with the Euro Stoxx Utilities Index up 16% this year, compared with a 3% decline of the MSCI ACWI Index. Armina Rosenberg, co-founder of Sydney-based hedge fund Minotaur Capital, said she and her team have “started buying some ‘decarb’ stocks, taking advantage of the drawdown in the market.” Companies targeted include First Solar Inc. and NextEra Energy Inc., which have supply-chain setups that mean they’re protected from and “may even benefit from tariffs,” she said. Meanwhile, despite being a target of Trump’s tariffs, China is continuing to attract green investors keen to add exposure to companies such as battery maker Contemporary Amperex Technology Co. and electric car brand BYD Co. Rosenberg said Minotaur has invested in BYD, which has gained close to 50%, compared with the decline of more than 40% in Tesla Inc. This is based on an assessment that “Chinese EVs are taking share from Tesla,” she said. Much of China’s clean-tech industry targets its local market or developing regions such as Africa, according to the Centre for Research on Energy and Clean Air. The US accounts for only 4% of Chinese exports of electric vehicles as well as solar and wind equipment, but remains a dominant importer of batteries together with the European Union, the analysis found. For more on how hedge funds are navigating Trump’s anti-climate agenda, read the full story on Bloomberg.com. |