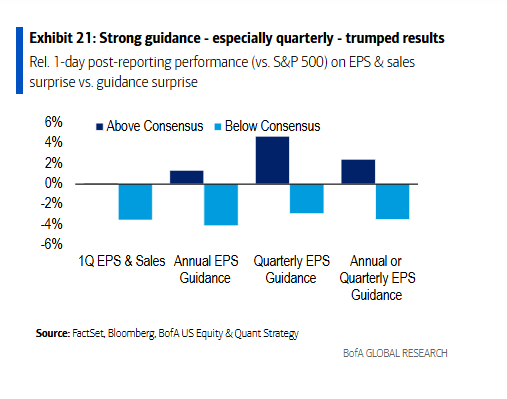

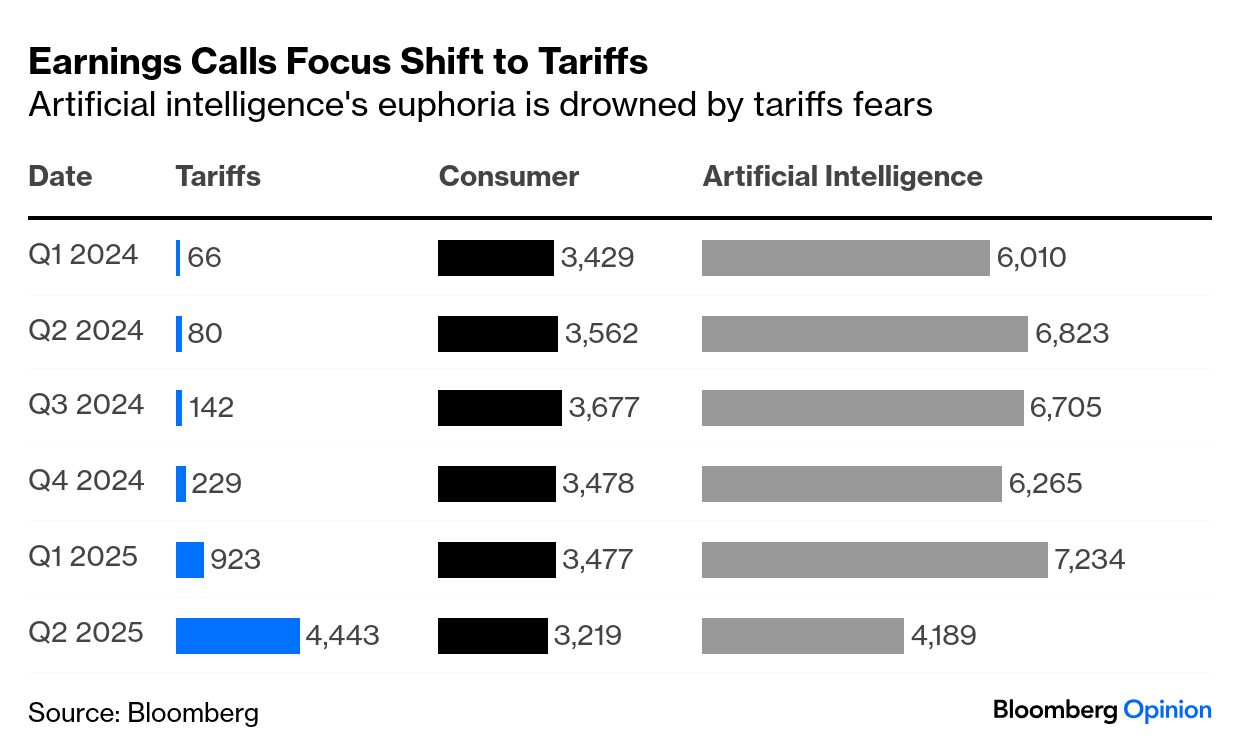

| Global trade tensions made for a very high-stakes first-quarter earnings season for executives. Wall Street analysts’ ears perked up not just for misses but for the more subtle cracks that could widen in an economic downturn. As generally happens, most companies beat the expectations bar they’d set for themselves. Out of the over 90% of the companies in the S&P 500 that have reported earnings, 78% beat their estimates for earnings per share — above the average for the last 10 years, according to FactSet. But that didn’t really matter, particularly as questions remain over the extent to which a pull forward in demand to beat tariffs bolstered the numbers. Bank of America’s Savita Subramanian adds that companies, too, are worried about their inability to tell recovery trends apart from stockpiling. In an uncertain environment, reactions to both beats and misses tend to be more exaggerated. FactSet’s John Butters notes that companies that have reported positive earnings surprises saw an average price increase of 1.9% two days before and two days after the release. This is more than the five-year average price increase of 1%. But strong forward-looking guidance, especially quarterly, was a bigger positive for the share price. This chart is from Subramanian: Tariffs A Bloomberg analysis of earnings call transcripts shows an astronomical surge in tariff mentions. Goldman Sachs’ David Kostin estimates that 89% of S&P 500 companies cited tariffs — even more than those who cited AI, which had dominated calls since the start of last year. The consumer was also important: Empower’s Marta Norton finds it reassuring that the uncertain economic outlook didn’t weigh on earnings performance, which was good enough to keep the market rallying. But she adds that “with all the economic data, you just can't project it forward because it's not representative of the environment we're heading into.” Margin exposure will be critical: I don’t think there’s a 100% ability to pass those costs along, which is why there could be some earnings deterioration in the near term. I just don’t know how significant it will be. But we do know the sectors where there’s exposure. Industrials, materials, consumer discretionary, staples, and technology — these are all the areas where there should be some cost pressure from these tariffs.

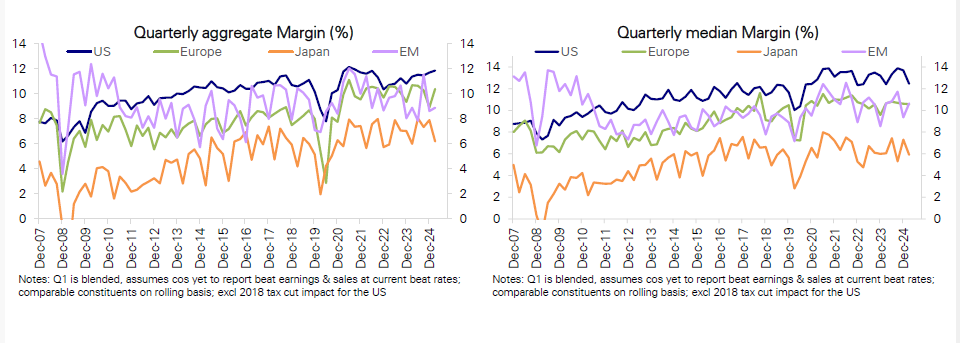

This chart, produced by Deutsche Bank’s Binky Chadha, highlights margin performance in the US compared to elsewhere — superior profitability has been crucial to American exceptionalism over the last decade. So far, the US has held steady, but future performance depends on how companies handle tariffs: Artificial Intelligence Even before the tariff scare, extreme large-cap valuations were expected to drive investors to diversify away from the US. That accelerated with January’s emergence of the Chinese large language model start-up DeepSeek, which proved that AI models did not have to be capital-intensive. But companies aren’t cutting back on their AI capex. Subramanian adds that the degree to which companies can monetize AI over the long term remains in question, while firms historically underperform in reinvestment cycles: In our view, AI capex is a bigger tailwind for the market than idiosyncratic AI monetization. Semiconductors are the most obvious beneficiaries, but increased power usage from AI and the physical build-out of data centers should also lead to more demand for electrification, construction, utilities, commodities, etc., ultimately creating more jobs.

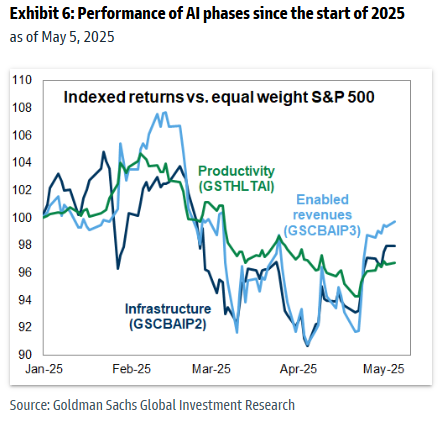

Meanwhile, Kostin shows that AI isn’t (yet) a game changer. So far this year, none of the groups of companies that should benefit most from AI have matched the average stock. Goldman’s basket of stocks with AI-enabled revenues has traded flat versus the equal-weight S&P 500, compared with two percentage points of underperformance for a basket of Phase 2 AI infrastructure stocks. Stocks expected to gain long-term productivity from AI lag by three percentage points: Time for Small Caps? Westwood Group’s Adrian Helfert sees small caps benefiting from technology adoption and innovation to maintain their margins. Small-cap companies haven’t done all that poorly in terms of fundamental performance; it’s just that mega caps have done so well that they mask everything else, according to Research Affiliates’ Que Nguyen. The US retreat from globalization changes the environment for global platform companies, creating space for small caps to shine. Our view is not necessarily that small-cap companies will somehow dominate these mega-cap companies. That’ll be too radical a shift. Our view is that the economic world order is changing, in a way that will make things a little harder for global platform companies.

Meanwhile, small caps are cheap. With corporate margins under pressure from tariffs, proposed tax cuts could provide temporary breathing room. However, Nguyen remains cautious. With US debt-to-GDP at historic highs, she argues that a traditional stimulus may deliver diminishing returns. And the Moody’s downgrade won’t help with that. —Richard Abbey |