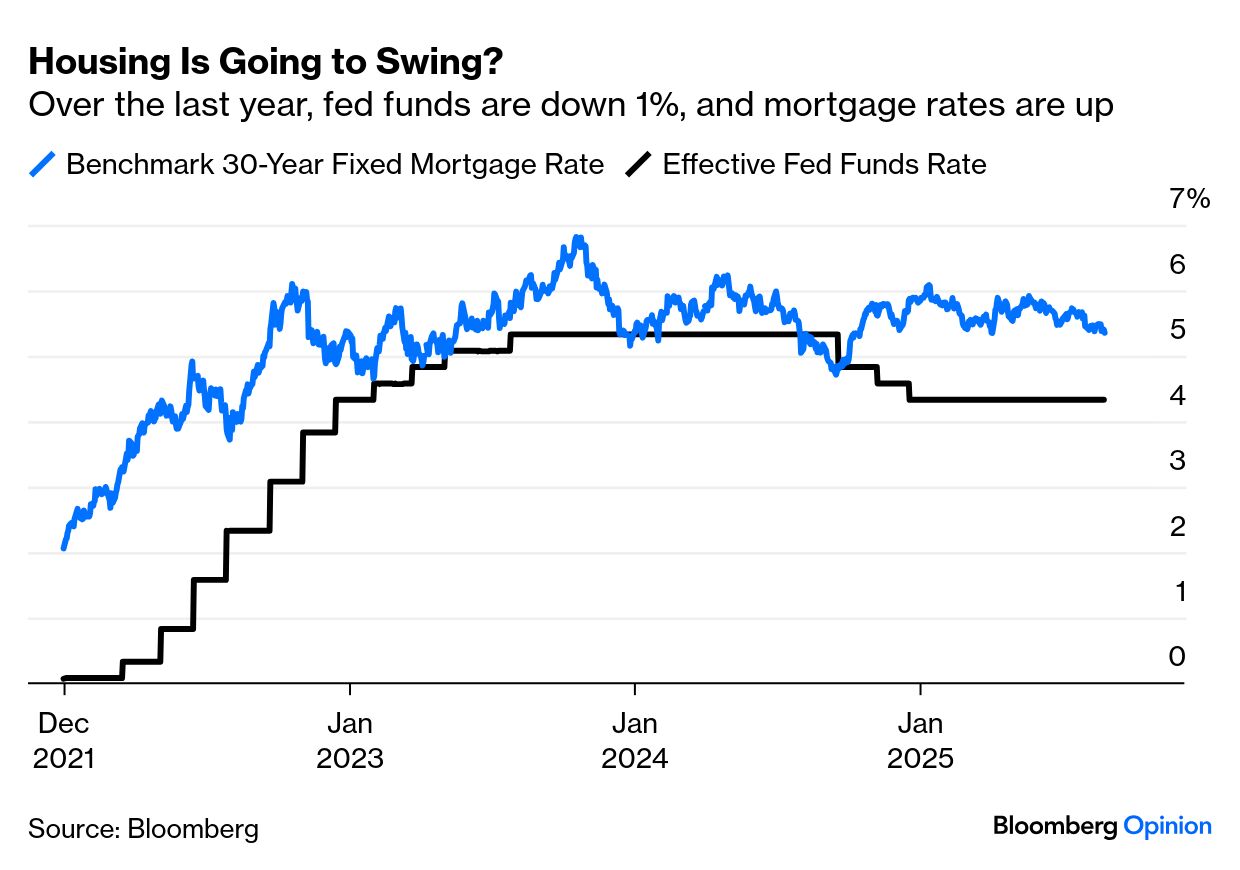

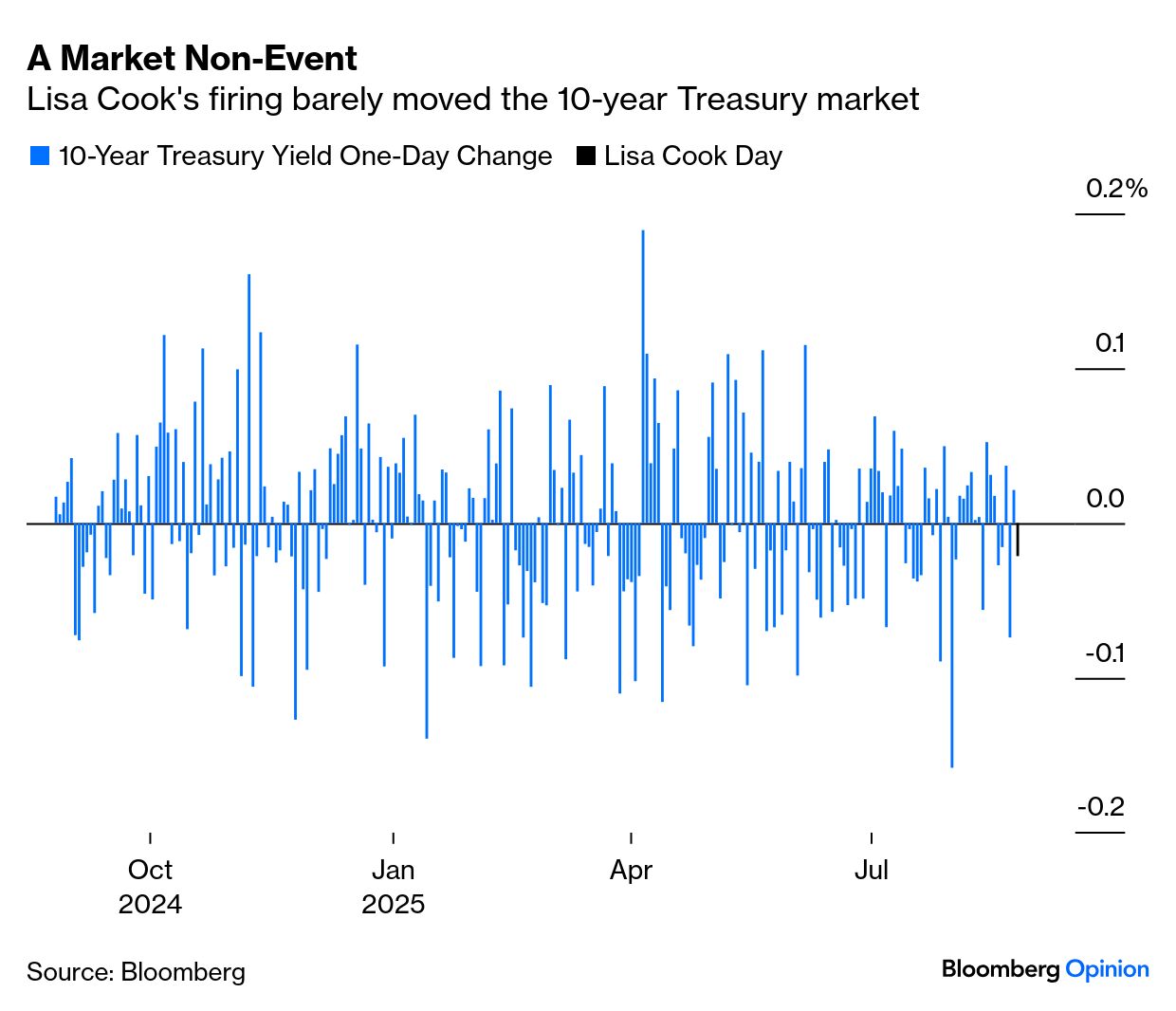

| If the end of central banking independence is terrifying financial markets, they’re not showing it. The US stock market gained slightly for a day that had been dominated from the opening by the Cook news. The two-year Treasury yield, sensitive to rate forecasts and volatile of late, barely moved: Gold rose, but remains below its high. The bottom line is that this has had minimal market impact. Mike Howell of CrossBorder Capital suggests that the calmness is down to a great job by the Treasury under Scott Bessent: US bonds are being well-controlled by policymakers. They matter hugely in a collateral-based credit system. We have argued that Fed and Treasury have been carefully managing liquidity and probably also targeting the MOVE index. Inflation seems to be cyclically dipping near-term and economy softening. With scarcity of coupons, long-term funds have no reason to sell. With low volatility, hedge funds have no reason to end basis trade.

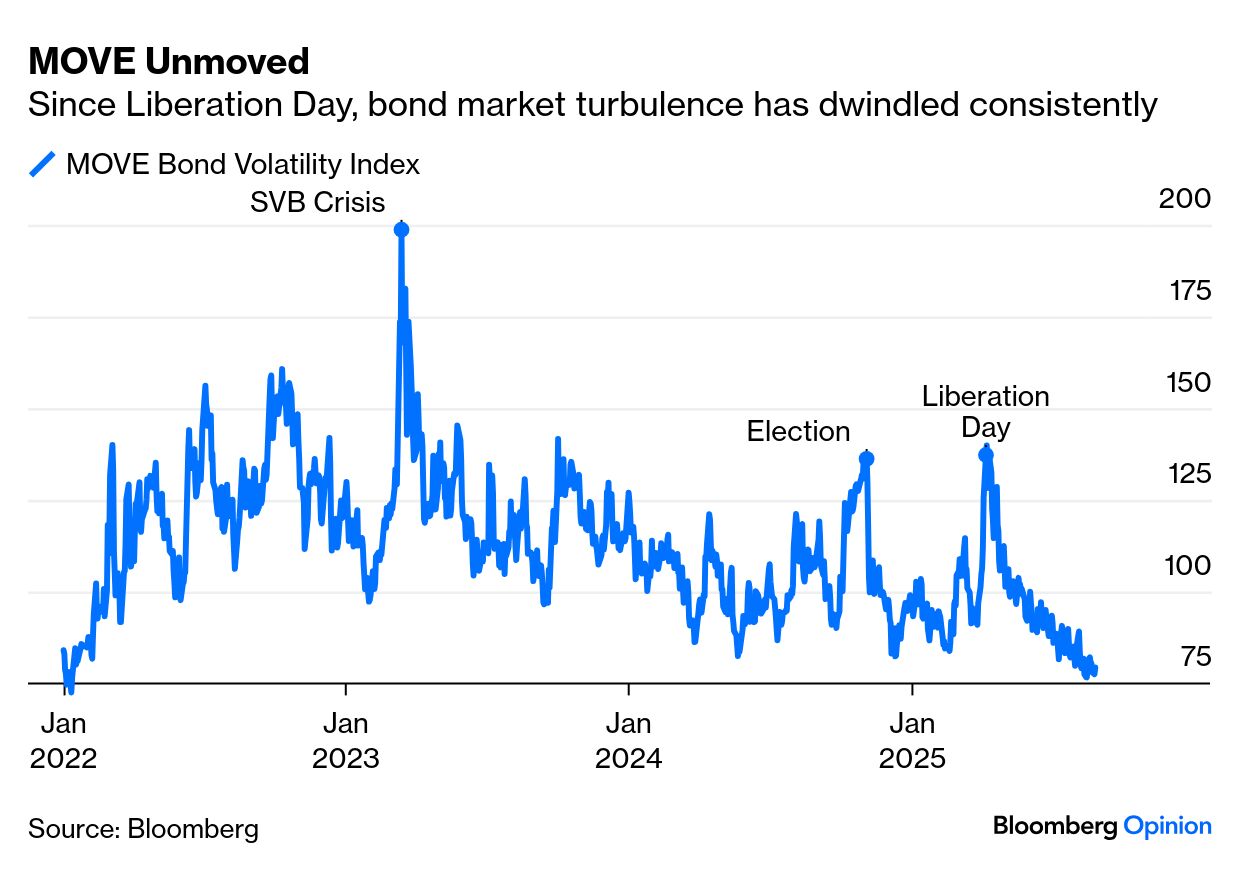

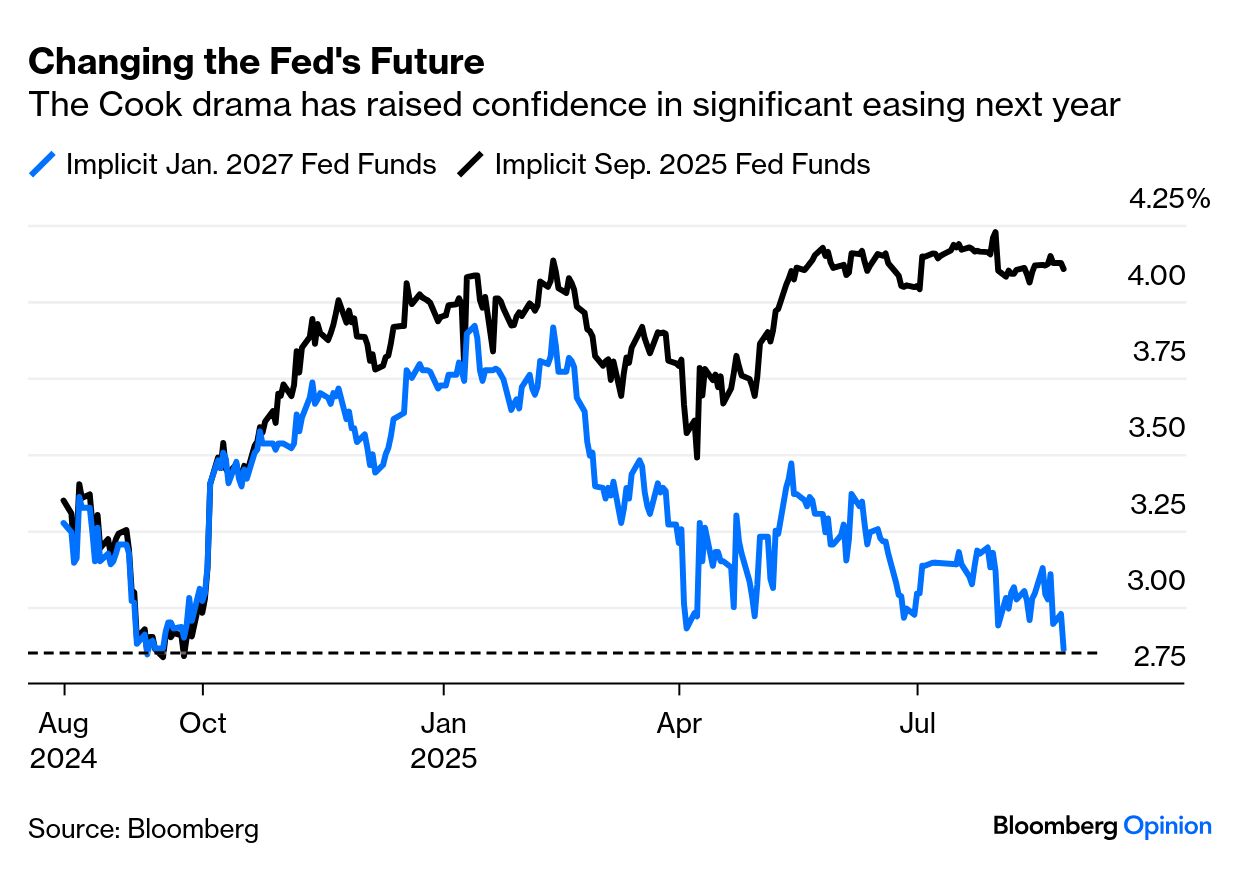

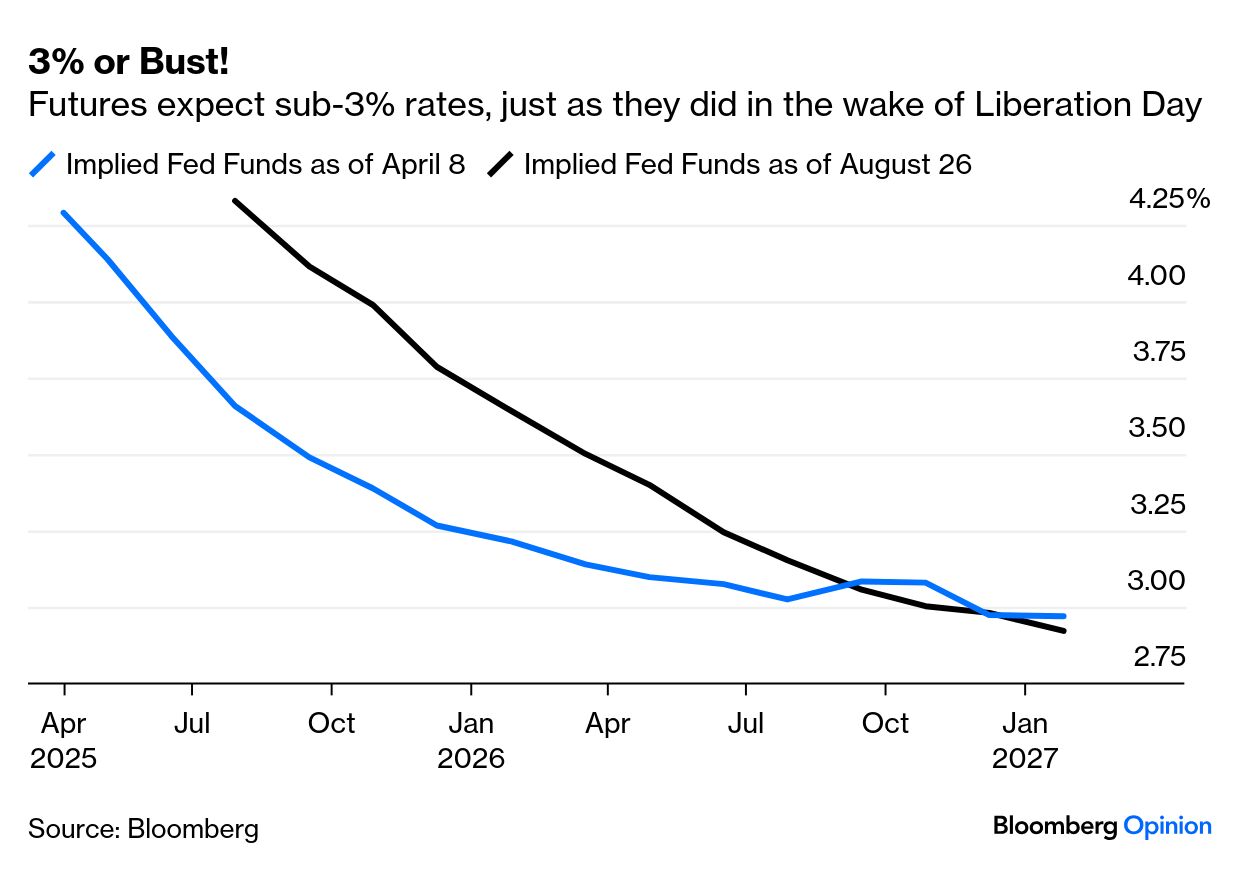

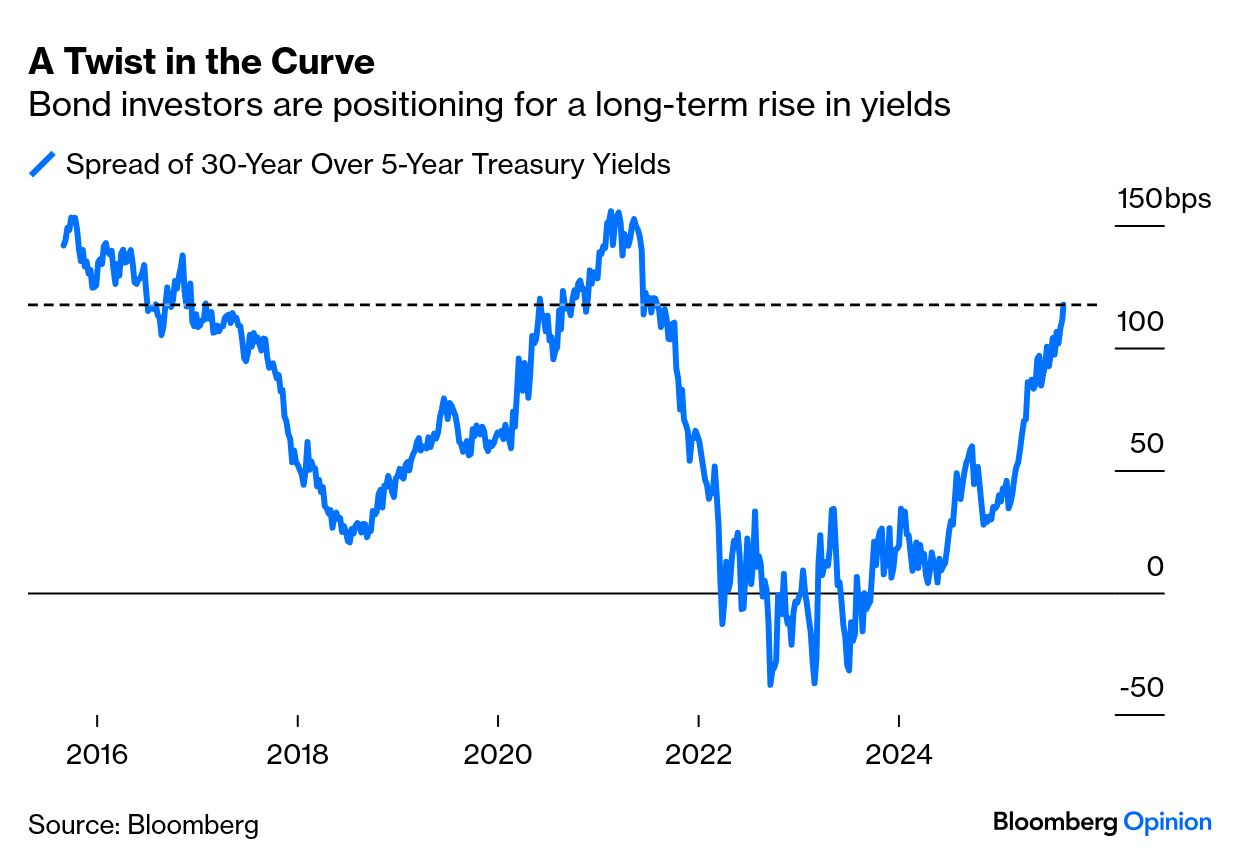

Since Liberation Day in April, the MOVE index, a gauge of bond market volatility, has indeed been remarkably steady. The last four months have seen threats to sack Powell, a downgrade to the US sovereign rating by Moody’s, the imposition of tariffs far higher than expected at the start of the year, a shocking revision to unemployment data, the firing of the head of the Bureau of Labor Statistics, and now the Cook drama. The MOVE has fallen steadily throughout: The imbroglio had its greatest effect on expectations for the medium term. Nobody foresees more than a 25-basis-points cut next month. The odds have barely shifted. The implicit fed funds rate expected for January 2027, however, is back to its low since the contract initiated a year ago, and dropped sharply on the Cook news. The odds of a post-Powell FOMC easing a lot next year are rising: The two previous times that January 2027 expectations were at about this level, last September when a recession scare prompted a jumbo cut and after Liberation Day, there was widespread alarm about an imminent economic downturn. There’s no such fear now. Investors’ confidence in a concerted easing next year is more or less entirely attributable to political pressure. After four months with the Fed in suspended animation, its projected flight path is back to where it was after the tariff shock in April: The move to fire Cook had its clearest impact on very long bonds. The five-year/30-year Treasury yield curve is now its steepest in four years: That suggests that the economy will expand, and push rates up in the long term. The administration will get fed funds to 3% or thereabouts by the end of 2026. But it may well not get its desired dirt-cheap mortgage rates. The market doesn’t expect fed funds to drop to Trump’s desired 1%, as anyone the administration could conceivably place on the Fed would balk at doing such a thing. The economy is in decent shape, and cuts next year will juice it further. The yield curve suggests a new equilibrium where the Fed tolerates higher inflation, and rates at the top end of the cycle will be higher than we’re accustomed to. Trump may therefore need to do more than interfere with the Fed to get what he wants. David Roberts of Nedbank warns that this risk is not yet adequately reflected in markets. The president, he points out, has already claimed emergencies to send troops to the peaceful streets of Los Angeles and Washington. He’s unlikely to balk at emergency intervention in the bond market, along the lines of desperation measures during the Global Financial Crisis. He can tinker with fed funds as much as he likes. Plan B comes when fed funds fall and he doesn’t get what he wants. Then they can look at QE from 2009, when they bought a lot of mortgage assets.

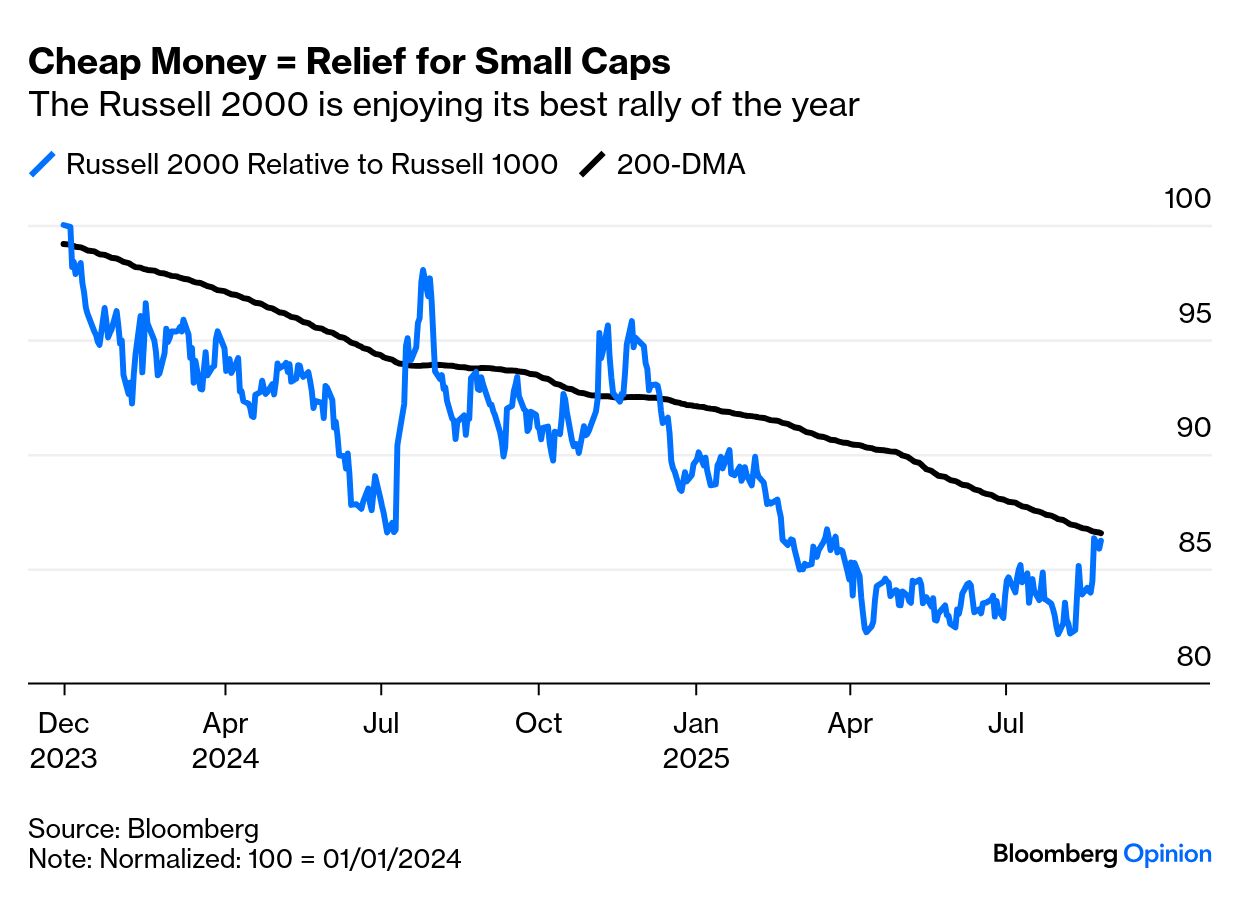

If the White House and Treasury resort to financial repression like this, there could be pain in future for those shorting long bonds. Just ask Japanese bond investors. For now, imminent rate cuts are great news for the usual suspects. Small-cap US stocks were also clear beneficiaries, as they are more leveraged than large caps. Alexander Altmann of Barclays Equities Tactical Strategies pointed out that approximately half of the Russell 2000’s debt burden is variable rate (i.e. tied to SOFR), and that its weighted average maturity was about half that of large caps: “It is movement in the front end of the Treasury curve that matters more” for the index. Surging 30-year yields were “of course bad for risk in general,” but they remained contained so there was little immediate reason for concern. That logic seems to have been applied across the market. |