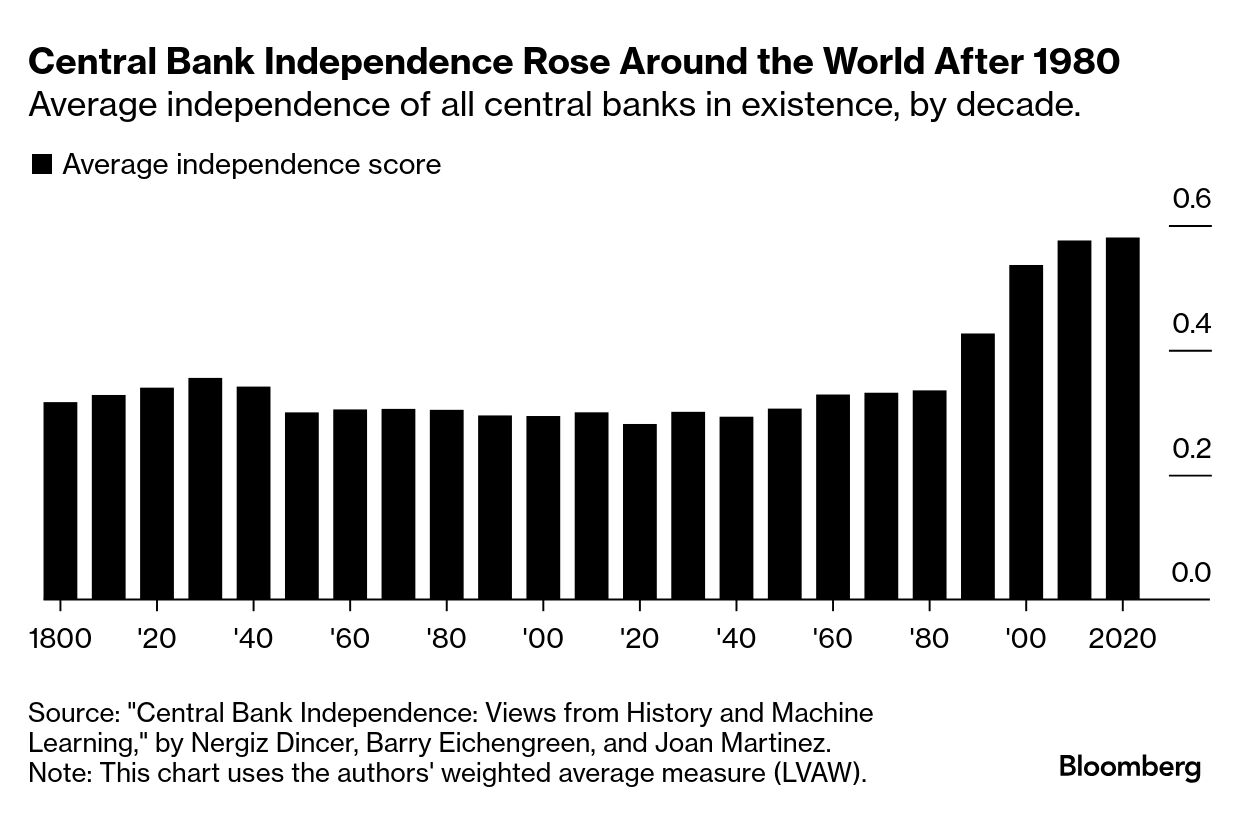

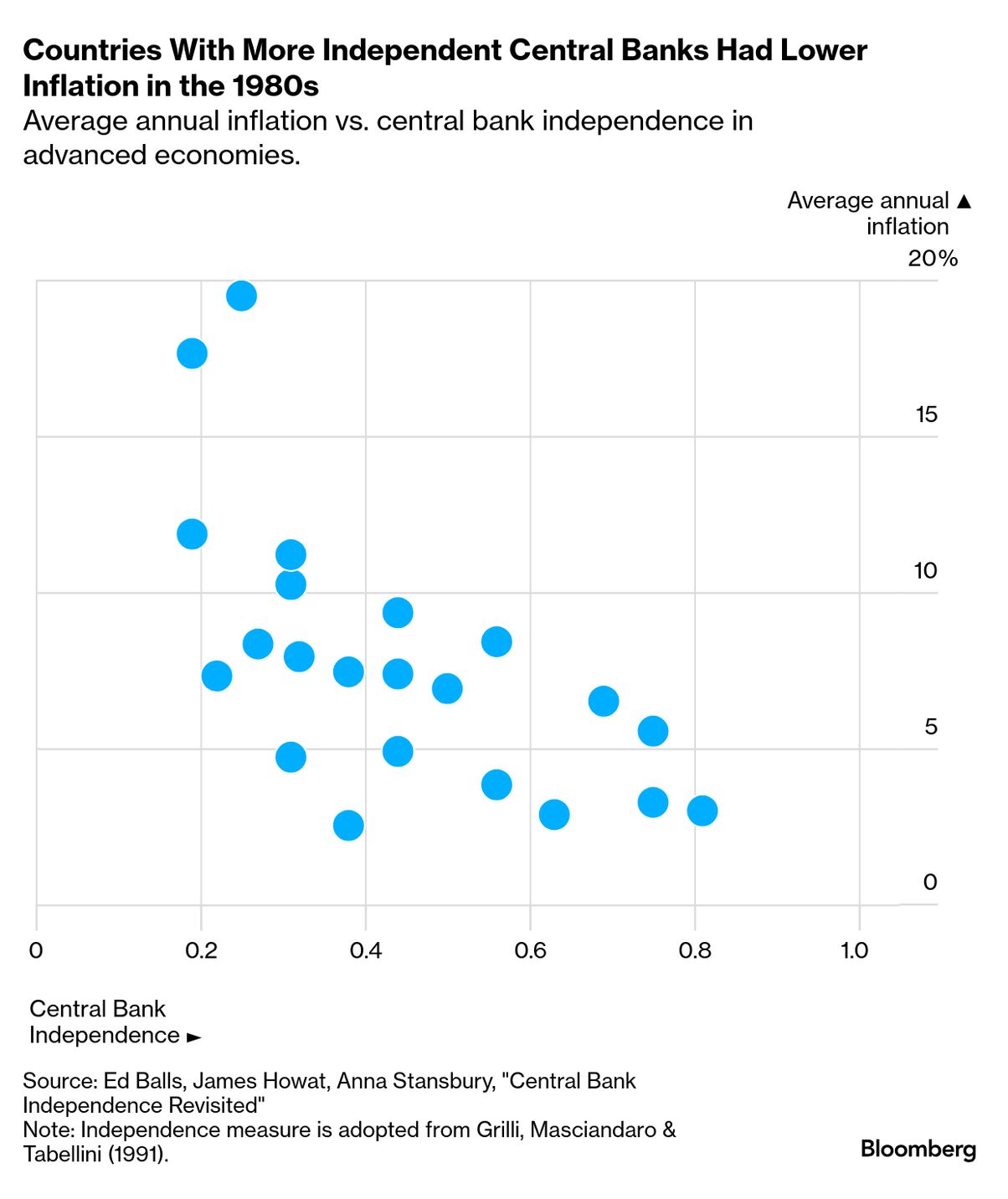

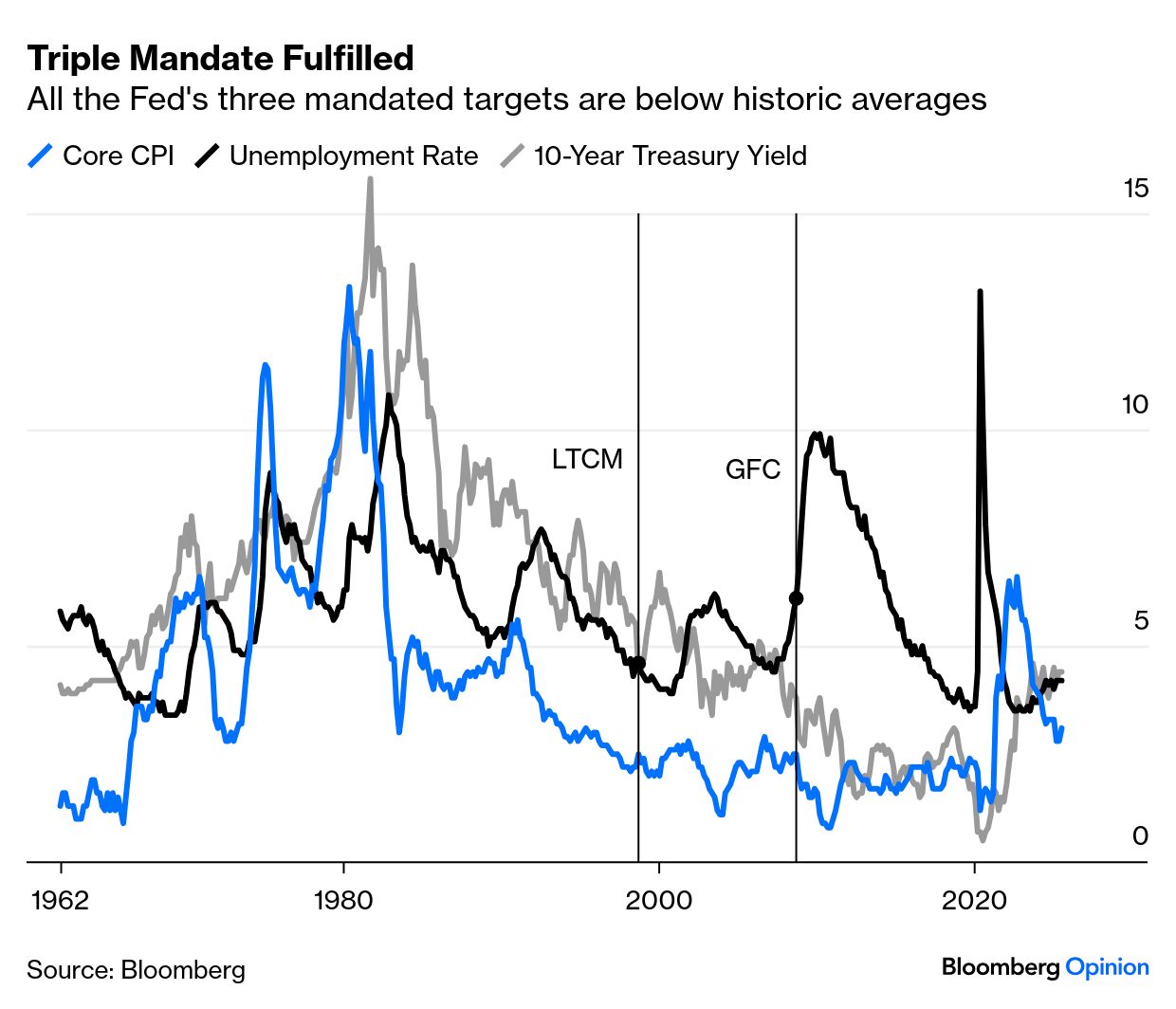

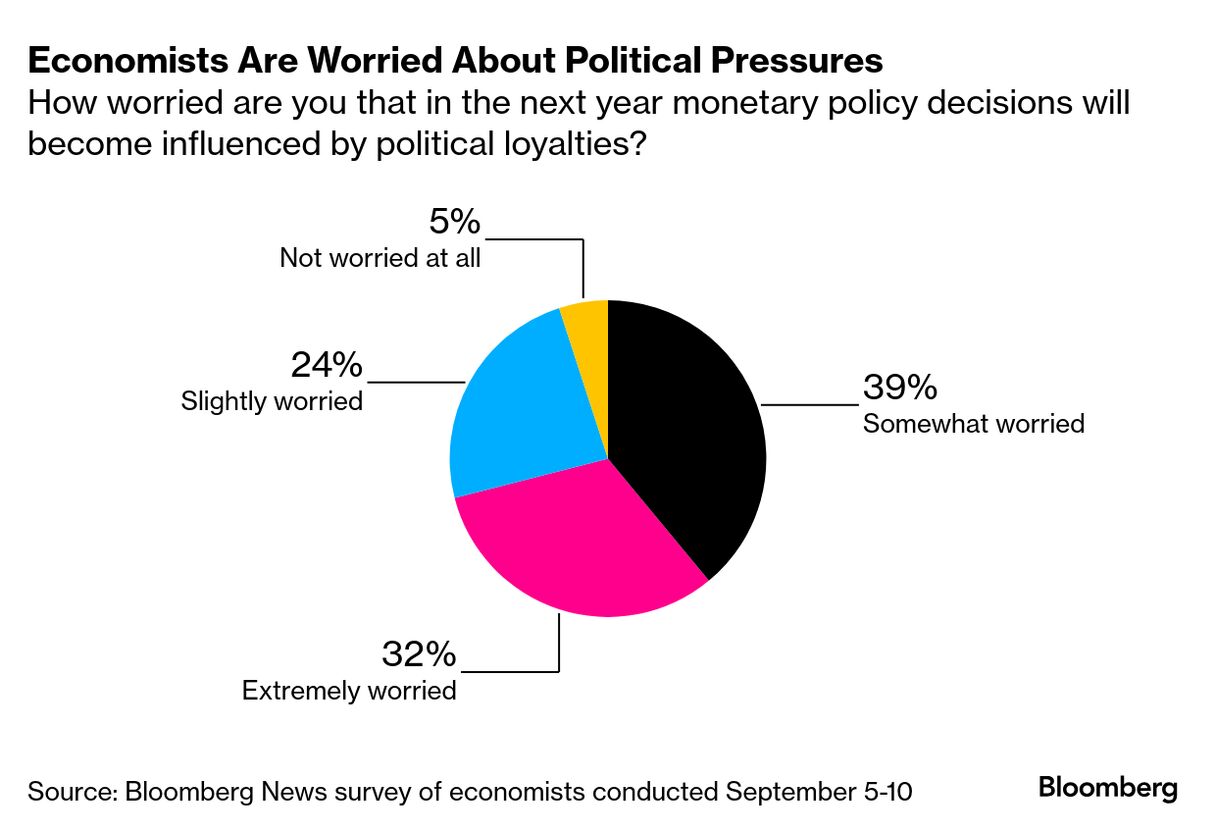

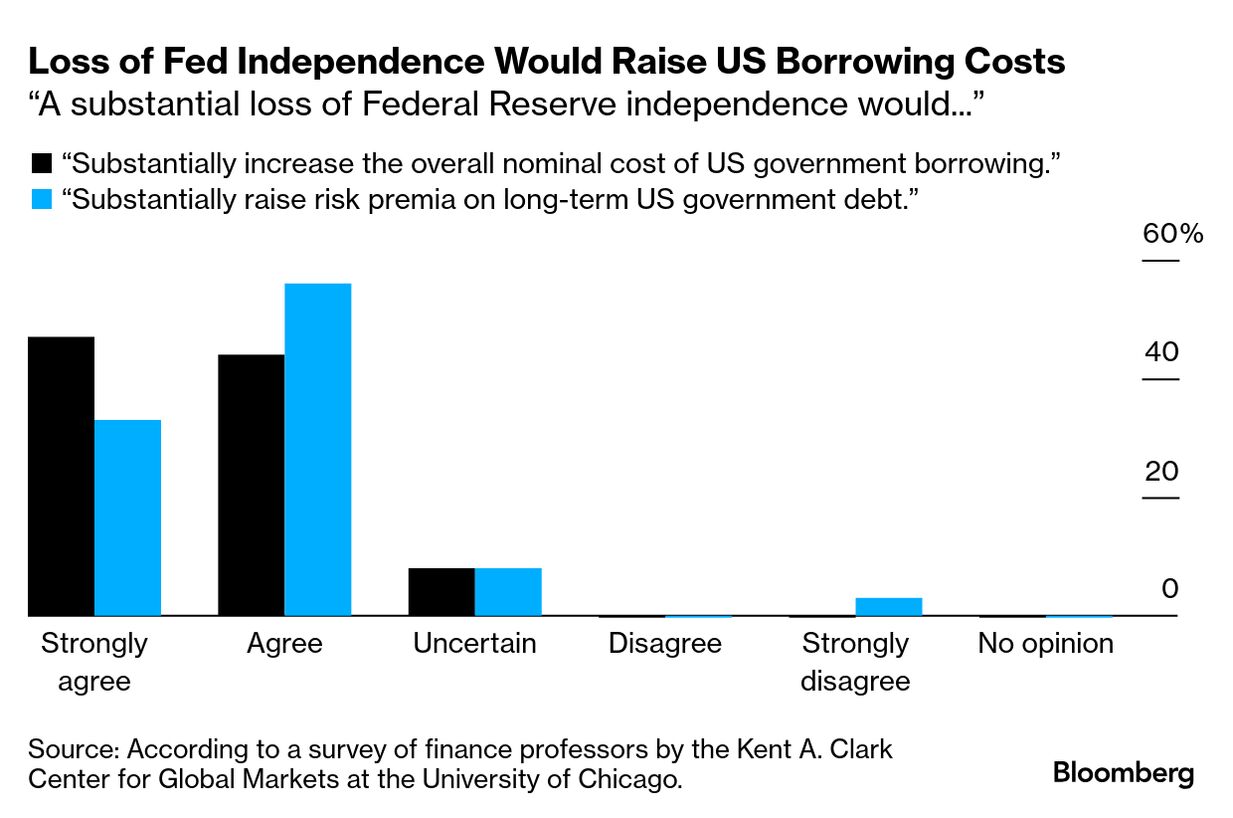

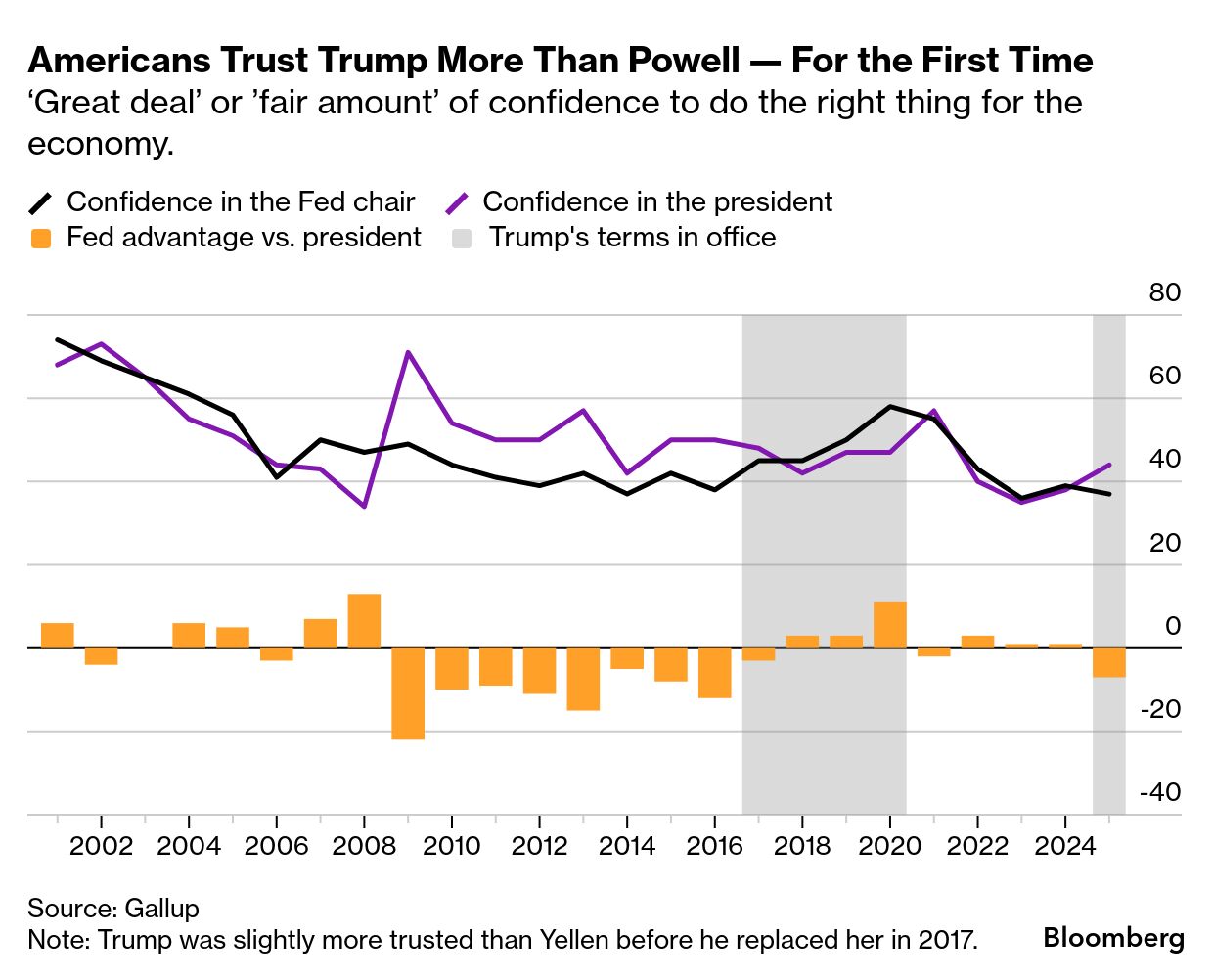

| This will be a big week for the Federal Reserve. Investors expect it to cut interest rates, with at least one more cut coming later this year. But attention will also be on the institution itself and its independence from the White House, which we covered in both an essay and a column this weekend. Today, though, let’s explore it in charts. Fed independence was kicked off by Congress in 1935, cemented in the Treasury-Fed Accord of 1951, and arguably demonstrated most forcibly by Paul Volcker in the early 1980s. But it’s worth noting that, globally, the modern era of central bank independence didn’t arrive until after 1980. The Fed’s arrangement, which many take for granted, was not particularly common until a few decades ago. Sticking with the global view, it’s fair to say central bank independence has mostly worked. Various studies have slightly different glosses and offer different caveats, but by and large independence has been associated with lower inflation. What about the Fed specifically? As my colleague Saleha Mohsin explains, Trump officials including Treasury Secretary Scott Bessent see the Fed’s recent record as “patchy at best.” In particular, Bessent has argued that the bank expanded beyond its original mission with an unconventional response to the 2008 financial crisis — and blurred the lines between fiscal and monetary policy. But in his Weekend column, John Authers takes a different view. The Fed’s congressional mandate, he says, comes in three parts, not two: maximum employment, stable prices and moderate long-term interest rates. Smash all three together and you can create what he calls a “triple mandate index” — unemployment, core inflation and 10-year bond rates. And by that measure the Fed is doing quite well: Whatever one makes of the Fed’s recent record, economists overwhelmingly support its prerogative to set interest rates — and a majority say they’re “somewhat” or “extremely” worried that the Fed’s decisions will become influenced by political loyalties, according to a September survey by Bloomberg News. If that happens, it would mean higher borrowing rates for the US government, according to a separate survey of academic economists by the University of Chicago. The experts also agreed almost unanimously that it would raise risk premia on US government debt. So why are we here? Mohsin ends her essay noting the elephant in the room: The president himself wants lower rates. Authers argues that the best critiques of the Fed require politicians to confront hard decisions, like how to balance inequality and growth. But don’t forget the backdrop: The Fed is an expert institution in an anti-expert and anti-institutional age. In 2001, 74% of Americans had confidence Alan Greenspan would do the right thing, according to Gallup. In 2025, 37% have confidence that Powell will. Trust in the president and in Congress has fallen over that period, too. But in 2025, for the first time in their tenure together, more Americans have confidence in Trump to do the right thing for the economy than they do in Fed chair Jerome Powell. That does not bode well for Fed independence. — Walter Frick, Bloomberg Weekend |