| It is helpful, in investing, to be able to amortize a certain amount of work over a lot of capital. If someone offers you an opportunity to invest in a company with an expected return of 30% annualized, that is pretty good, and you might be willing to take the meeting and do some due diligence and sign the contracts and wire the money and do all the intellectual and administrative work to get that return. But if the company is a lemonade stand and your investment is capped at $20, that 30% return will not be very exciting. What you want is an asset with a high expected return and a lot of capacity, one where you can invest millions of dollars, earn 30% of millions of dollars, and get a nice reward for all the work you put into understanding and making the investment. In the stock market, this works out nicely. The biggest companies are the ones where you can most easily put capital to work; you can buy a billion dollars of Nvidia stock without too much trouble. And the biggest companies are also in some intuitive sense the most valuable ones, the companies that the market has decided are the best companies, the ones with the highest future earnings and growth potential, the good safe stocks, though of course the market can be wrong. In credit markets, though, it is a little counterintuitive. The more debt a company has, the easier it is to buy that company’s debt. The debt will be more liquid and more likely to appear in indexes. If you put the work into understanding the company, and you decide you like it, you can buy a lot of the debt and get a lot of bang for your buck. Particularly in private debt markets, where you buy the debt not by clicking a button on a screen but by negotiating complicated bespoke agreements directly with the company, it is a lot of work to invest in any one company, and it’s nice to be able to reuse that work. If the company borrows a lot of money every three months, and they call you every time, that’s easier than having to find new companies to lend to — and do new due diligence and negotiate new agreements — every three months. Big borrowers are convenient. But the more money a company borrows, ceteris paribus, the riskier its debt is. [1] People sometimes complain about this in the context of bond index funds: Market-cap-weighted bond indexes funnel money to the borrowers who have the most debt, which are not necessarily the safest bond investments. I have to say that, relative to trading stocks and bonds, trade finance seems pretty inconvenient. You have a bunch of, like, auto parts suppliers selling windshield wipers to a bunch of auto parts stores, and they sell the windshield wipers on credit and the stores owe them money, and they have an invoice for like $1,000 of windshield wipers that is due in 90 days, and they come to you and say “we’ll sell you this invoice for $975 and you’ll get $1,000 in three months and that’s more than 10% annualized,” and you’re like “yeah that’s pretty good here’s your check,” and then some other supplier comes to you with another $2,000 invoice, and you’re doing this all day for lots of little invoices. I mean, not literally; probably you set up a program with each supplier to discount lots of their invoices, so you don’t have to negotiate new agreements for every $1,000 invoice. But still, lots of suppliers, lots of customers, lots of moving parts. If some company comes to you and says “I have rolled up a bunch of auto parts suppliers and here’s a billion dollars of invoices to discount,” you might be like “man, that is so convenient, here’s $975 million.” If you run a billion-dollar trade finance fund, having one counterparty sell you $1 billion of invoices is less work than having a million counterparties sell you $1,000 of invoices each. You can do your due diligence once, you can sign one agreement, you can put a lot of money to work. But obviously it is riskier: - Now you have very concentrated exposure to the one counterparty, and if things go wrong at the one counterparty your whole fund is in trouble.

- If your one counterparty is borrowing a billion dollars then it is, uh, heavily indebted? Needs a lot of money? Could run into trouble paying all of it back? Maybe a worse credit risk than someone only borrowing $1,000 at a time?

- You have to think about the incentives that the counterparty faces. It comes to you and is like “here’s $1 billion of invoices, are you in,” and you are like “ugh thank you I am sick of all these small invoices, please, yes, bring me as much as you can, I would love to put a lot of money to work and just can’t get enough invoices,” and your counterparty gets to thinking “hmm, people really want my invoices, how can I manufacture more,” and that way madness lies.

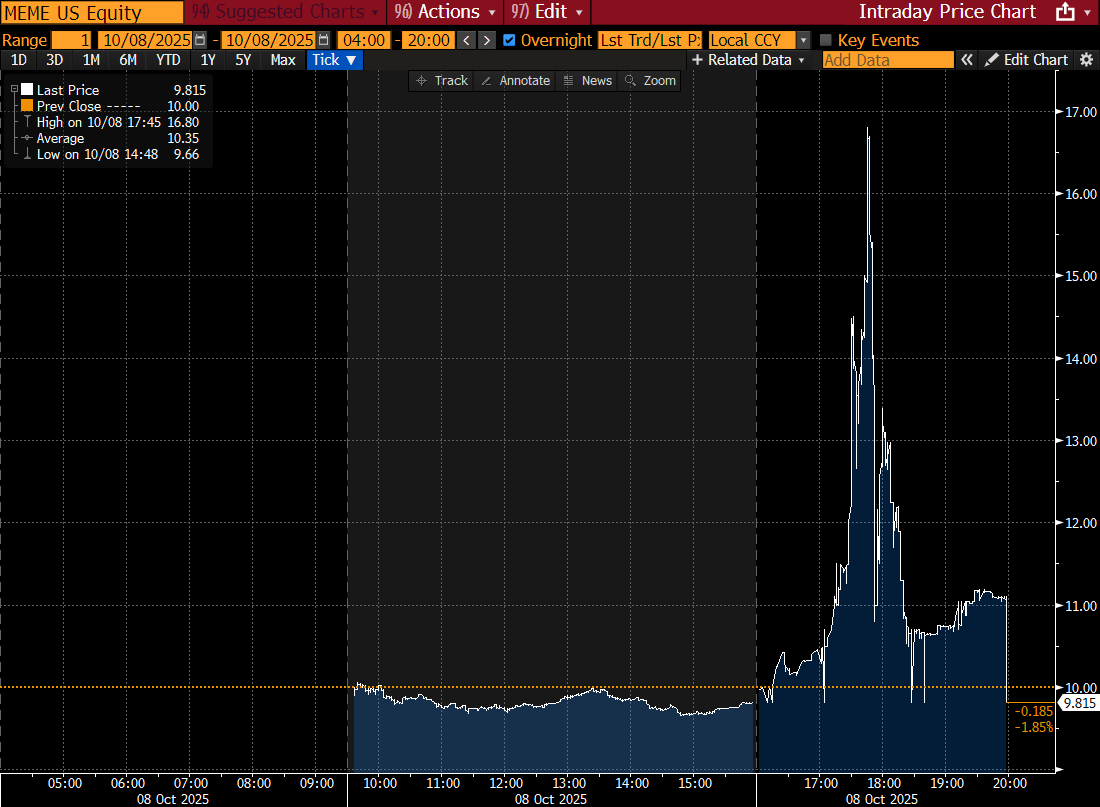

One way to tell the story of Greensill Capital, the supply-chain-finance firm that blew up in 2021, is that it was in the business of financing invoices for various companies, and that was a good business and it was able to raise lots of money and earn high returns relatively safely, but it was too easy to raise money and too hard to deploy it: Lots of investors wanted to finance invoices, and there were only so many invoices to finance. So Greensill would go to its borrowers and say “hey we could just give you large long-term unsecured loans and kind of pretend that there are invoices somewhere.” “Prospective receivables,” Greensill actually called them: It would make long-term loans secured by the borrowers’ plans to one day find customers and sell them products and get invoices for payment. This was a terrible idea and Greensill blew up, but it was also sort of understandable. It wanted to finance more invoices than it could get, so it started financing some imaginary invoices. Is that part of the First Brands story? First Brands Group Inc. did go out and acquire a bunch of smaller auto parts suppliers, rolled them up into one big company, and got billions of dollars of trade financing against their sales. Now it is in bankruptcy, and there are allegations that it might have used the same collateral to take out multiple loans and that “as much as $2.3 billion has ‘simply vanished.’” The latter allegation came in a demand for an investigation from Raistone, a trade finance platform: The request for appointment of an independent examiner follows an Oct. 2 email exchange in which a bankruptcy lawyer for First Brands told Raistone that advisers don’t know if the auto parts supplier has received an estimated $1.9 billion. … “First, do we know whether FBG actually received $1.9 billion (no matter what happened to it)?,” Raistone lawyer Emanuel Grillo said in an Oct. 2 email, which was filed in bankruptcy court in support of its request for an examiner. “Second, would you tell us how much is in the segregated accounts in respect of the factored receivables as of today?” “#1 —We don’t know,” First Brands restructuring lawyer Sunny Singh said in response to the questions. “#2 - $0.” Not the answer they wanted! It is definitely not fun, as a bankruptcy lawyer representing a creditor, to receive an email like that. (It is probably not fun, as a lawyer representing the debtor, to send an email like that, but … maybe a little fun? Like that is an objectively funny email, if it’s not your money that vanished.) But also: Raistone, the company that called for the investigation, and that had facilitated First Brands’ short-term borrowing, derived 80% of its revenue from First Brands and has already cut roughly half of its employees. The O’Connor hedge fund unit owned by UBS is facing such significant losses that Cantor Fitzgerald is now trying to renegotiate the terms of its acquisition of the business. Jefferies is facing redemption requests from investors who had money in a hedge fund arm of the bank, Point Bonita Capital, which had a quarter of one of its portfolios — some $715 million — tied to First Brands. Raistone, “whose founder had been one of Greensill’s first employees,” got 80% of its trade-finance revenue from First Brands. That Jefferies fund had a quarter of its portfolio in First Brands debt. There was a lot of demand for receivables, and First Brands was apparently in the business of meeting that demand. In part by doing debt-financed acquisitions: First Brands’ aggressive maneuvers allowed [owner and chief executive officer Patrick] James to build a company that had 26,000 employees on six continents and revenues of around $5 billion in 2024, according to a presentation to investors. But the underlying business, selling replacement auto parts to the likes of AutoZone and Walmart, did not offer up tremendous growth potential once the acquisitions stopped. Between 2023 and 2024, while its revenue only rose 1.3%, the cost of servicing its debt went up 38%, the investor presentation showed. … “First Brands is a clear case of a company with a very aggressive founder and very bad financial disclosures that don’t give you enough information as an investor,” said Michael Gatto, a partner at Silver Point, a credit-focused investment firm that looked into First Brands loans but is not invested. “They were constantly making acquisitions, and that way they could mask problems because it gives the idea that the business was constantly growing.” Did it also meet the demand in part by double-pledging collateral, selling more receivables than it had? Nobody seems to know yet. But you can see why people are worried. Hey the meme-stock exchange-traded fund is back: Roundhill Investments … revives a pandemic-era trope — the MEME ETF. The original fund was shuttered in 2023 when it looked as if the craze it was born in had blown over. It hadn’t. Now the New York-based firm is resurrecting the Meme Stock ETF on Wednesday. ... “In some ways, ‘meme’ is still perceived as a dirty word. Many still scoff at what the retail community does on various forums. But that’s an entirely antiquated view,” said Dave Mazza, Roundhill’s chief executive officer. “What didn’t fade is the influence of retail in today’s equity market.” The original version passively tracked a meme-stock index, but the new one is actively managed and zeros in on a tighter basket of roughly two dozen stocks that exhibit what Roundhill views as meme-like characteristics, such as extreme price volatility. Its top holdings from the get-go include Opendoor Technologies Inc., Plug Power Inc. and Applied Digital Corp. Cool cool cool. “The Roundhill Meme Stock ETF (‘MEME’) is the only ETF in the world to offer targeted exposure to meme stocks,” its website says, though I suspect several leveraged Strategy ETFs would disagree. Intuitively, you might expect a meme-stock exchange-traded fund to trade above its net asset value. You know: It’s a meme thing. The point of a meme stock is that it trades above its fundamental value because of retail enthusiasm. If you plop 21 meme stocks together in a fund with the ticker MEME, surely that should spark some retail enthusiasm. “No,” you object, “the retail enthusiasm might push the 21 underlying meme stocks up above their fundamental values, but the ETF, which is just a transparent collection of those stocks, will not attract any additional retail enthusiasm and so will trade in line with the prices of the underlying stocks,” but, why? The whole hypothesis here is that retail traders like memes and don’t care about fundamental value. If they see a meme-stock ETF called MEME they might get excited to buy it, without worrying too much about what’s in it or whether it is trading at a premium. But that’s not how ETFs work. The reason that ETFs normally trade in line with their net asset values is not “people won’t buy them for more than NAV”; people will do all sorts of things. The reason that ETFs normally trade in line with their NAV is arbitrage. If the net asset value of an ETF is $10, that means that an arbitrageur can deliver $10 worth of underlying stocks to the ETF issuer and get back one share of the ETF. [2] If the ETF is trading at $12, arbitrageurs will buy the underlying assets for $10, deliver them to the ETF, get back shares, sell them for $12, and make $2 per share. They will do this as long as anybody wants to buy the ETF for $12, or $11, or $10.10, pushing down the price of the ETF (and pushing up the prices of the underlying stocks [3] ) until the ETF trades at close to net asset value. And so if you go to your brokerage account and send in an order to buy 100 shares of MEME at the market price, you are going to get those shares of MEME at something very close to their net asset value. The person selling you those shares will be an electronic market maker, and the market maker can effectively source those shares from either (1) the market for MEME shares or (2) the market for the underlying assets. If the underlying assets are cheaper than the MEME shares, the market maker will buy them and turn them into MEME shares for you, so you should never have to pay much more than NAV to buy the MEME shares. Even if you want to! Even if you are like “I would buy shares of this meme-stock ETF at whatever price you want to charge me, I love meme stocks so much, just give me the shares,” the market maker still isn’t going to charge you much more than net asset value. Irrational retail demand is a nice little source of profits for the market maker, but market making is a competitive business and no one’s going to get away with charging you $11 per share. Here’s a chart of MEME’s first day of trading yesterday: Just by eyeballing it you get the basic idea. From 9:30 a.m. to 4 p.m., MEME traded at kind of normal prices, in line with its net asset value. It closed at $9.82 per share, a premium of 0.2% to its NAV of $9.80 per share. After 4 p.m. it went nuts. It hit a high of $16.80 per share at 5:41 p.m. It also traded quite rich before the open this morning, trading as high as $13.30 per share at 8 a.m. And then, at 9:30 a.m. today, regular trading began and MEME went back to normal. It opened the regular trading session at $9.92 per share and traded in a range between $9.72 and $9.97 for the rest of the morning. What happened? Intuitively it seems like the explanation has the form “retail investors got excited to buy the MEME ETF, so they did. During regular market hours, they bought the MEME ETF from market makers, and arbitrage relationships kept its price in line with its net asset value. At 4 o’clock, the market makers went home and the price of the MEME ETF went crazy: Lots of retail investors wanted to buy it, they didn’t care about the price, and nobody was bothering to arbitrage it to keep the price in line with net asset value. So it traded at a huge premium to NAV overnight. And then at 9:30 this morning, the market makers came back to the office and started trading the MEME ETF at NAV again, so everything went back to normal.” That is not quite a correct explanation: Big electronic market makers are aware that the stock market continues trading (in extended sessions) after the 4 p.m. close, and starts trading again in the morning before the 9:30 a.m. open. They keep their computers on, they buy and sell stocks, they arbitrage ETFs. Not every stock goes crazy after 4 p.m. Yesterday was MEME’s first day back on the market, and it’s still extremely small; its website says it only has about $250,000 of assets so far. It might just be too small and new for professionals to bother trading after 4 p.m., but if it gets traction and assets then its after-hours trading will settle down. Still the general story does seem to be that, between 9:30 a.m. and 4 p.m., US stock markets are relatively normal and there are powerful arbitrage forces making prices — at least ETF prices — reflect economic reality. After 4 p.m. the grownups go home and retail trading can get weird. Elsewhere in memes, here is the story of Bed Bath & Beyond Inc. [4] : - Early in 2023, Bed Bath was essentially bankrupt — it had a ton of debt and no real hope of repaying it — but it had not yet filed for bankruptcy.

- But it “checked the two boxes needed to become a meme-stock: (i) a troubled financial situation and (ii) nostalgia value,” as its bankruptcy lawyers later put it, so it could sell some stock.

- Did it ever. It started January 2023 with about 117 million shares outstanding; by the time it filed for bankruptcy in April, it had 739 million. So about 85% of the shares outstanding at the end were issued in 2023, as Bed Bath was sliding into bankruptcy.

- These stock sales transferred several hundred million dollars pretty directly from the retail shareholders who bought the stock to the creditors who got what was left of Bed Bath in bankruptcy. (Ultimately the brand was sold in bankruptcy to Overstock.com, which changed its name to Beyond Inc. and now uses the Bed Bath name.)

- This always struck me as wild: Almost all of Bed Bath’s shares were sold in its death throes, to retail investors, with no real hope of making money. As I once put it: “Bed Bath was kind of like ‘hey everyone, we went bust, sorry, but our lenders are such nice people and they could really use a break, we’re gonna pass the hat and it would be great if you could throw in a few hundred million dollars to make them feel better.’ And the retail shareholders did!”

- Roughly half of those stock sales were in at-the-market offerings directly to retail shareholders.

- The other half, though, were done in a strange structured transaction with Hudson Bay Capital Management. Loosely speaking, Hudson Bay paid Bed Bath $360 million, in several installments, for a total of 311 million shares of Bed Bath stock. But Hudson Bay did not hold that stock: The point of the trade was that Hudson Bay would (1) get a slug of stock at a discount to market prices, (2) sell it to retail investors at a profit and (3) go back for another slug of stock. Bed Bath’s stock was sliding dramatically during the course of this trade — the stock fell from $5.86 per share the day the trade was announced to $0.59 the day it wrapped up — in part because Bed Bath was heading to bankruptcy but in larger part because Hudson Bay was selling hundreds of millions of shares as fast as it could, pushing the price down. Hudson Bay was not going to take stock price risk on this deal; it wasn’t buying a big block of stock at a fixed price hoping to resell it. It was buying tiny blocks of stock at a discount to market prices, selling them quick, and then coming back for more at ever-lower prices.

- Technically the way this worked was that Hudson Bay bought convertible preferred stock with a floating conversion price: Hudson Bay could convert every $1,000 slug of preferred stock into (more than) $1,000 worth of common stock at market prices, so it could constantly turn each $1,000 of its investment into stock it could sell for more than $1,000. (It also got warrants to buy more convertible preferred stock, because it didn’t put in all the money up front.)

- This was very lucrative: I once estimated that Hudson Bay made about $84 million on its $360 million commitment, and the Bed Bath bankruptcy estate later estimated that the number might be $310 million. In any case, Hudson Bay did well, while the retail shareholders lost 100% of the money they put in.

There is an oddity in that quick summary. If you take it literally, you might think something like the following. “Hudson Bay got 311 million new shares at a time when Bed Bath only had 117 million shares outstanding. So Hudson Bay was by far Bed Bath’s majority shareholder in early 2023, with 311 million out of 428 million shares, or about 73%. US securities laws have rules about ‘short-swing profits,’ designed to prevent insider trading by affiliates. In particular, Section 16 of the Securities Exchange Act says that a 10% shareholder who buys stock and then sells it within six months has to ‘disgorge’ any profits from the trade to the corporation. Here, Hudson Bay was a 73% shareholder and spent months buying stock from the company and immediately turning around and selling it at a profit. The total profit was tens or hundreds of millions of dollars. Shouldn’t it have to disgorge those profits to the company?” Bed Bath’s bankruptcy estate — the creditors who took it over in bankruptcy and got back less than they were owed — had that thought, and sued, claiming that Hudson Bay had made $310 million and should have to hand the money over to the creditors. We talked about the lawsuit last year. I was skeptical, but I wrote that “the main point here is that if you are a bankrupt company and you’ve got a shot at clawing back $300 million to hand over to your creditors, you have to give it a try.” Bed Bath gave it a try. Last week it lost: On Tuesday, a federal judge dismissed the complaint against Hudson Bay. Here is the opinion. The basic idea is that, while Hudson Bay’s deal with Bed Bath did in some sense entitle it to 311 million out of 428 million shares — it owned convertible preferred stock convertible into a majority of Bed Bath’s common shares — it was not entitled to all of those shares at the same time. The deal included a “Section 16 blocker” saying that Hudson Bay was not allowed to own more than 9.99% of Bed Bath’s common stock, keeping it under the Section 16 threshold: If it was at the 9.99% cap, it couldn’t convert any more preferred stock into common. Of course, this was not a practical problem, because Hudson Bay never wanted to own the common stock for more than an instant: It would convert some preferred into common, sell it immediately, get down to 0% ownership, and then convert some more. It would never actually own anything close to 10% of Bed Bath’s stock. Bed Bath’s creditors took the view that this doesn’t matter: Hudson Bay owned convertible preferred that could eventually be converted into 73% of the common stock, so it was a “beneficial owner” of 73% of the common stock, so it was a Section 16 insider and should have to give up its profits. Hudson Bay took the view that, no, the preferred never could be converted into 73% of the common stock, so it wasn’t an insider. As a former corporate equity derivatives structurer myself, I was sympathetic to Hudson Bay’s view, not so much because it’s right but because it is market standard. A lot of deals include Section 16 blockers so that intermediaries can deal in a company’s stock without becoming insiders restricted from trading, and if those blockers didn’t work then a lot of financings would get harder. But they work: In sum, BBBY’s allegations do not amount to a plausible claim for relief on the theory that the blocker provisions were illusory or a sham. Thus, Plaintiff does not plausibly allege that Defendants beneficially owned the common stock underlying the Derivative Securities they held such that Defendants were over 10% beneficial owners of outstanding BBBY common stock while executing conversions and sales of the stock within a six-month period.

Hudson Bay gets to keep its money. I wrote yesterday about one model for public-company mergers and acquisitions, in which the target company is sold by its shareholders and bought by a buyer, with the company’s management acting as a broker for the deal. In this model, the managers are incentivized to get the deal done — if they get the deal done, they get big change-of-control payments — and they have reasons to inflate the company’s value to the buyer, and deflate its value to the shareholders, to make sure a deal happens and they get paid. In a footnote, I added: This is not the only model — often the managers want to keep doing their day jobs, don’t want to be acquired, and have to be paid to even consider a deal — but it is sometimes a useful one.

Probably that’s the more standard model of public-company M&A: Not “managers are constantly going around trying to sell their companies to get paid, even if that means selling shareholders out cheap,” but rather “managers really want to keep their jobs and try to avoid being acquired, even if an acquisition would be good for shareholders.” On that more standard model, the change-of-control and severance payments and accelerated stock vesting that managers get when a deal closes are necessary protections for shareholders: If the managers didn’t get a big payout for getting a deal done, they’d never get deals done. I once wrote that “few CEOs have ever deserved their severance package more than Parag Agrawal,” who was the chief executive officer of Twitter Inc. when Elon Musk bought it (and then immediately fired him). Agrawal had a more-or-less pleasant job running Twitter, for which he was paid well. Musk came along with a hostile bid to buy Twitter, making clear that (1) he would make drastic changes to the product that Agrawal probably wouldn’t like, (2) he would make working at Twitter considerably more unpleasant and (3) he’d fire Agrawal and his executive team. It seemed to me at the time, and now, that this was all basically rotten for Agrawal personally, and that he wished Musk would go away. But Musk’s offer was $54.20 per share in cash, which was considerably more than Twitter was realistically worth on its own. The deal was bad for Twitter’s managers, but good for shareholders. In general, the CEO of a public company can’t just say no to a viable, fully financed cash takeover offer at a big premium to the company’s market price: Shareholders will get annoyed, and the buyer can (and Musk threatened to) go hostile and take the offer directly to the shareholders. So even if Agrawal didn’t like Musk’s offer personally, he had no real choice but to engage with it. He did, and Twitter quickly agreed to Musk’s terms, and shareholders got a good deal. And then Musk tried to get out of it! Which was great for Agrawal! He could have gone back to running his pleasant little social media company without interference from Musk other than some mean tweets. But that would have been bad for shareholders — Twitter definitely wasn’t worth $54.20 on its own after the Musk escapades — so instead the management team hired lawyers, sued Musk, and forced him to close the deal. The managers salvaged many billions of dollars of value for Twitter’s shareholders, at the expense of (1) their jobs and (2) quite a lot of personal unpleasantness from dealing with Musk. Why did they do that? I have not asked them, but the two standard answers are: - They were public-company executives, they had fiduciary duties to shareholders, and they took those duties seriously as a matter of professional pride and honor. [5] They did what was right for shareholders because that was what they were supposed to do.

- Their employment contracts included big severance payments, so if they got Musk to close the deal and fire them, they’d get tens of millions of dollars as a consolation prize.

Probably both things were true, but the second thing does matter. For all of their professional pride and honor, if the upshot of forcing Musk to close the deal was that they would be fired with no pay and insulted on their way out the door, they might not have worked quite so hard to get him to close. But then Musk did fire them with no pay, daring them to sue to enforce their severance arrangements. And they did. Yesterday Bloomberg’s Jef Feeley reported that they have settled: Elon Musk and the company formerly known as Twitter have agreed to resolve a $128 million lawsuit filed last year by former Chief Executive Officer Parag Agrawal and three other top officials who said they were denied severance payments. Terms of the settlement weren’t disclosed in a Sept. 30 federal court filing, which pushed back deadlines in the case and the date of a scheduled hearing in San Francisco. “The parties have reached a settlement and the settlement requires certain conditions to be met in the near term,” a lawyer for the executives said in the filing. Presum |