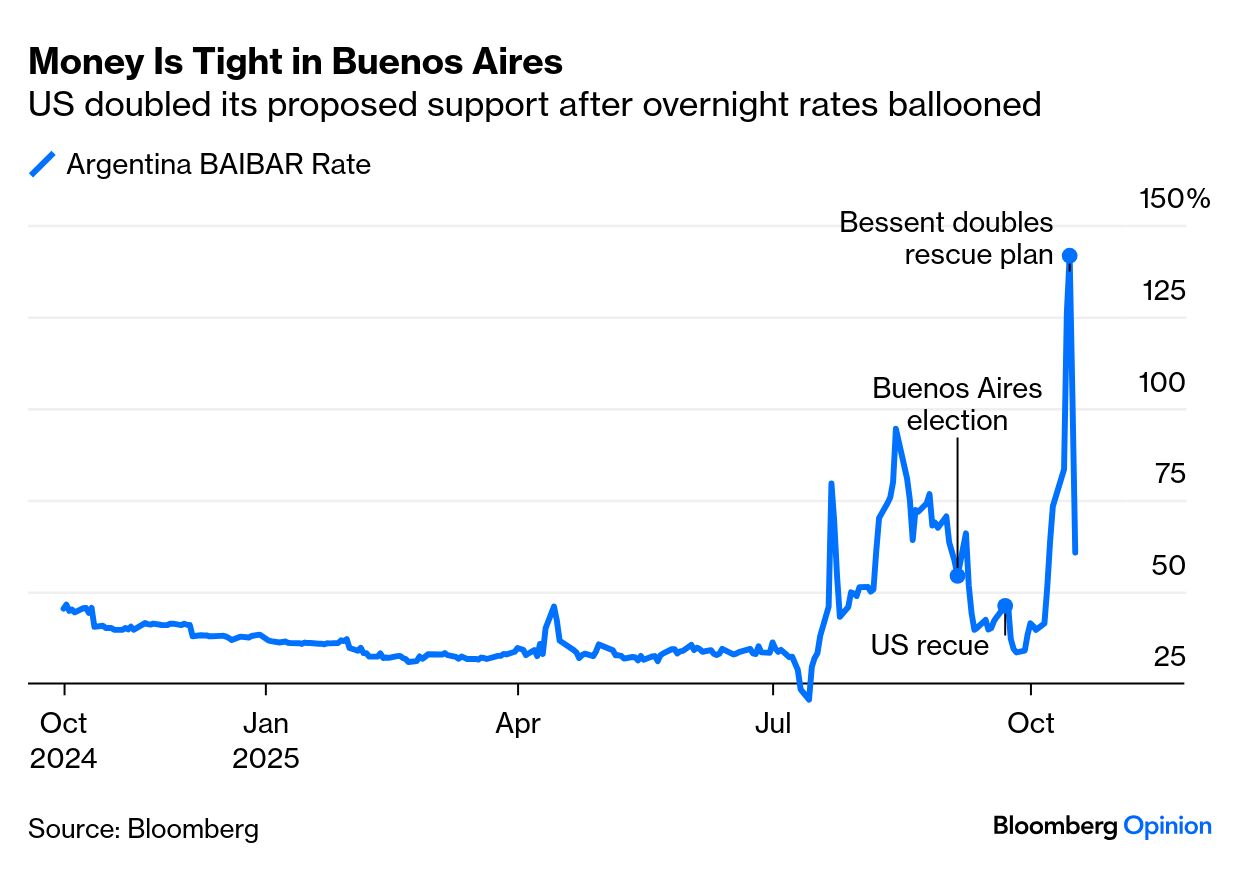

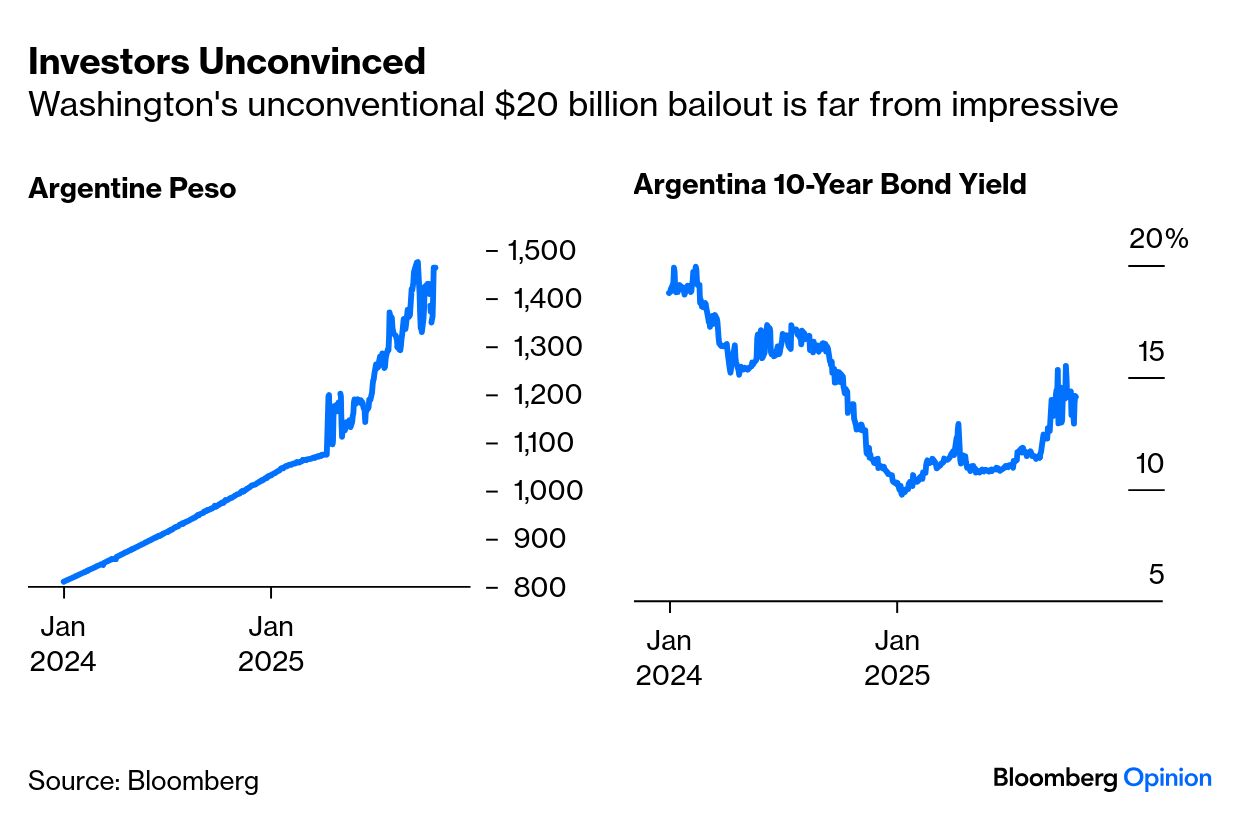

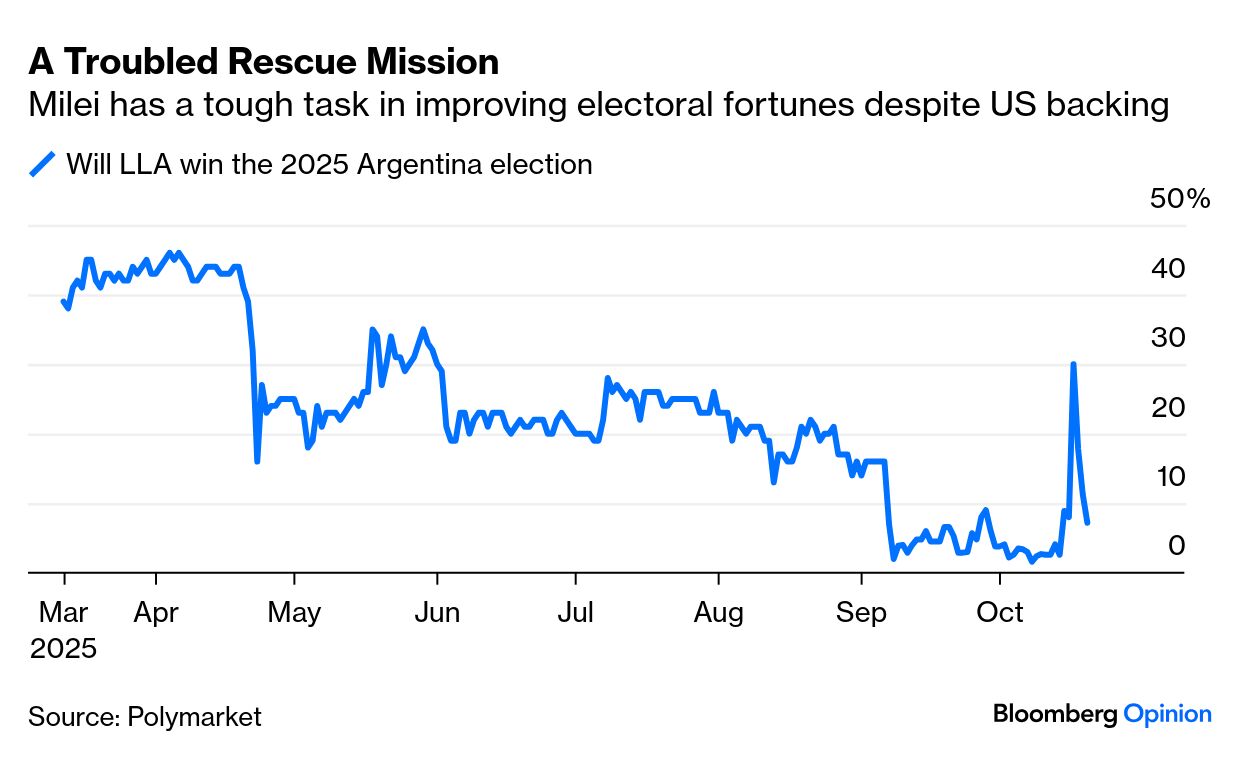

| Ordinarily, a US Treasury backstop in times of crisis is as good as money in the bank — or so Argentina’s President Javier Milei thought. The reality is proving far more complicated. Treasury Secretary Scott Bessent, who was already backing Buenos Aires with a $20 billion rescue package, is now wagering another $20 billion to buy pesos that he, surprisingly, considers undervalued. But so far, not even Monday's signing of the promised lifeline has calmed investors, with the peso heading into a five-day losing streak despite Uncle Sam buying it. As things stand, this unconventional bailout, which is similar to the US rescue of Mexico in 1985, hasn’t fixed the damage. It has calmed but not eliminated extreme pressure in money markets. Argentina’s overnight BAIBAR rate for banks briefly spiked to 140%, but remains at 60%: Ahead of crucial midterm elections on Sunday, the lifeline has calmed a developing market rout in the perennially fragile economy. But the peso, like Argentina’s bonds, quickly retreated after the initial positive reaction: Bonds are exceptionally volatile, and responded dramatically to an announcement late in the day that the government planned to buy back 10-year bonds: This might not rescue Milei at the polls. The peso’s continuing torment, even after Mario Draghi-esque whatever-it-takes rhetoric, is a bad sign. The critical question is whether Milei’s party, reeling from its bruising defeat in the Buenos Aires provincial election last month, can piece together a congressional coalition strong enough to insulate him from any attempt at impeachment. His La Libertad Avanza party holds only a sliver of congress — roughly 15% of seats in the lower house and about 10% in the Senate. A strong showing would strengthen his attempt to push reforms through a hostile legislature. But the US support comes with strings attached, as Trump has made clear. If Milei flops at the polls, the US backstop will no longer be there. The more investors sense the race slipping away from him, the faster economic confidence could erode. Polymarket’s odds on Milei’s chances of building the largest congressional delegation have receded all year, and dwindled again after the Washington rescue: Bloomberg Opinion colleague Juan Pablo Spinetto points out that traditionally, Argentines are quite “anti-American and the idea of having Trump so involved may be very dangerous for the ruling coalition.” The question is whether Argentines will reject Trump’s backing even if doing so risks an economic relapse. I see more Argentines willing to vote against Milei's coalition because of the Trump association than Argentines saying, '”Oh I am now voting for Milei because Trump is standing up to him.” But in the end, folks will vote on local issues — basically how much the economy is hurting them and how much they are willing to give Milei another chance. This isn't an election about Trump.

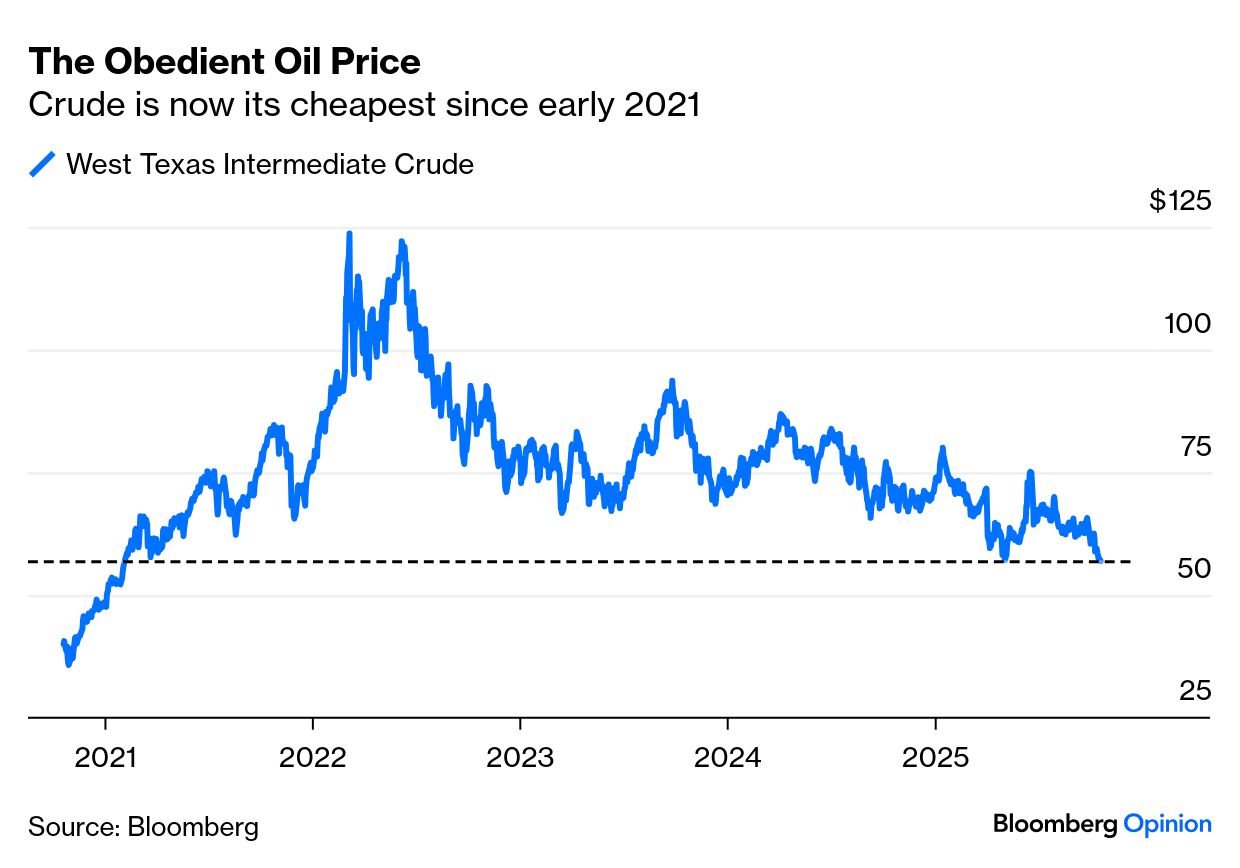

Investors are now gaming out possible post-election scenarios, and how each might reshape Argentina’s fragile recovery. Citi Research’s Johanna Chua expects greater forex volatility if the electorate rebuffs the current economic policies, and sees some parallels with the loss of momentum for the reformist president Mauricio Macri towards the end of his term in 2019. Whatever Sunday’s outcome, a stable recovery will be hard without a weaker currency that narrows the current account deficit and allows Argentina to rebuild foreign reserves, Chua argues. As the chart from Capital Economics’ Kimberley Sperrfechter shows, the peso’s overvaluation has already fed into a widening current account deficit, preventing any meaningful accumulation of FX reserves. Once elections are over, policymakers will try to balance reducing inflation and external competitiveness — which probably means a step devaluation and a new trading band. The peso is currently overvalued somewhere between 25% to 35%. Thus, there’s a long way to go once the political dust settles — and the US Treasury is unlikely to make a good profit on its money. Even so, as Sperrfechter notes, while this policy mix would be the right move, itmight not fully restore external competitiveness. Should Milei’s party fare poorly, there is a real risk of a sharp and disorderly peso correction that would undermine Bessent’s assertion that the currency is undervalued. As Robin Brooks of the Brookings Institution notes, the Treasury secretary is hardly oblivious to the risk of the odds turning against him. That justifies making Washington’s support conditional. The election is merely the beginning. —Richard Abbey |