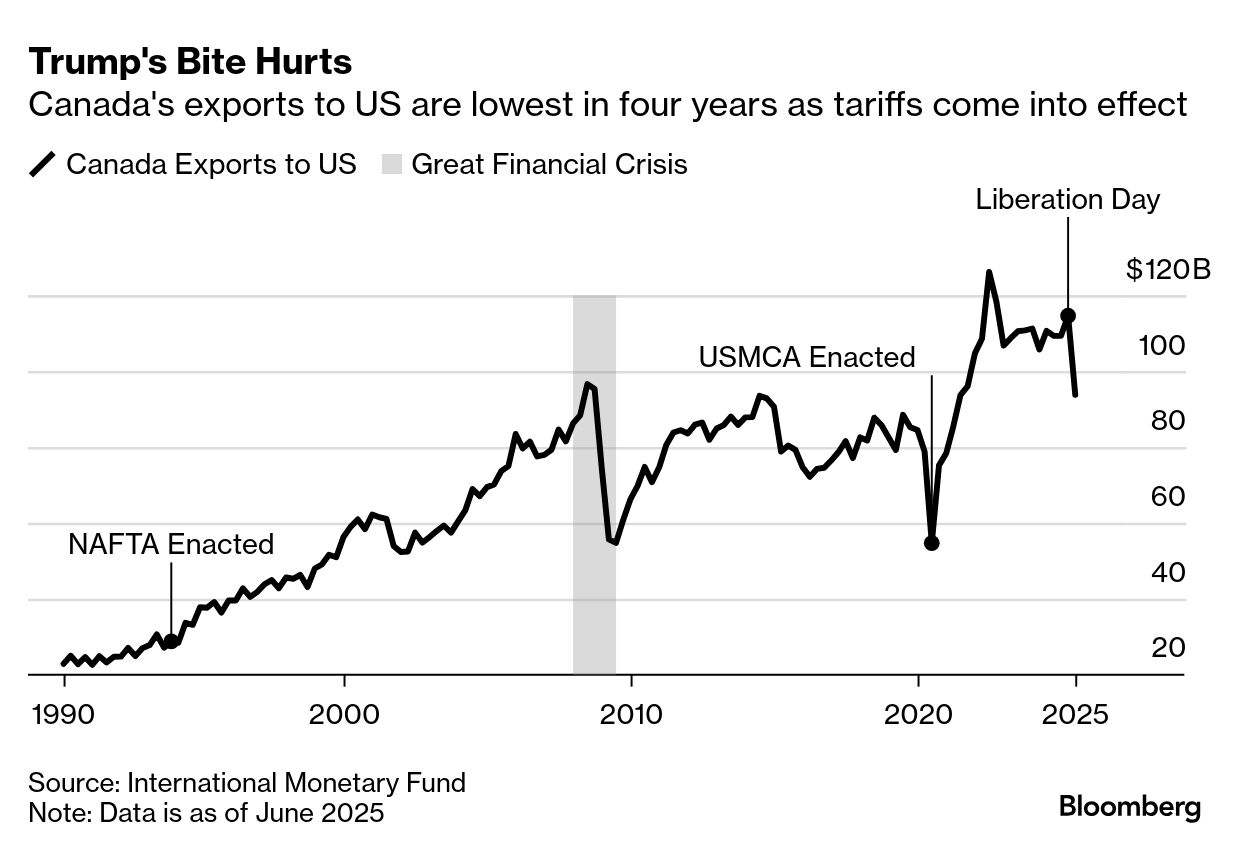

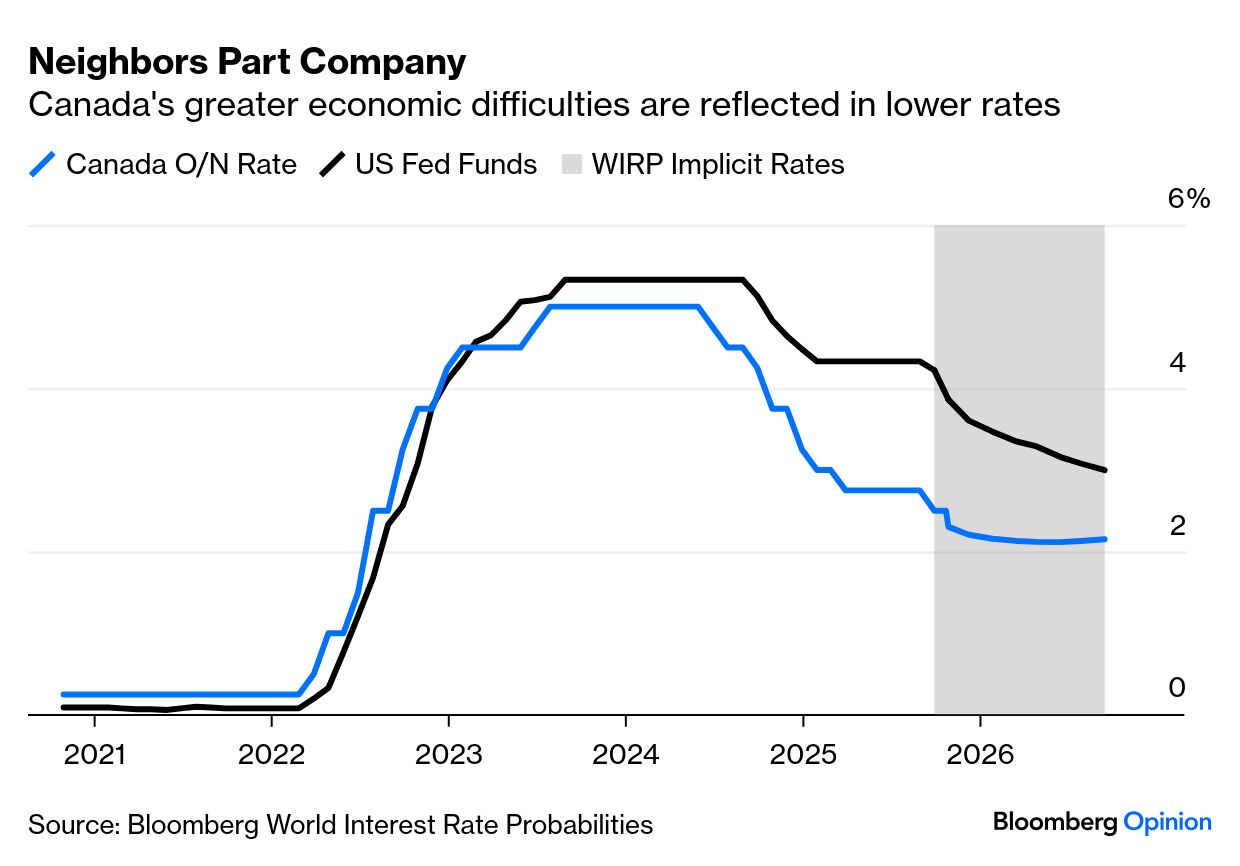

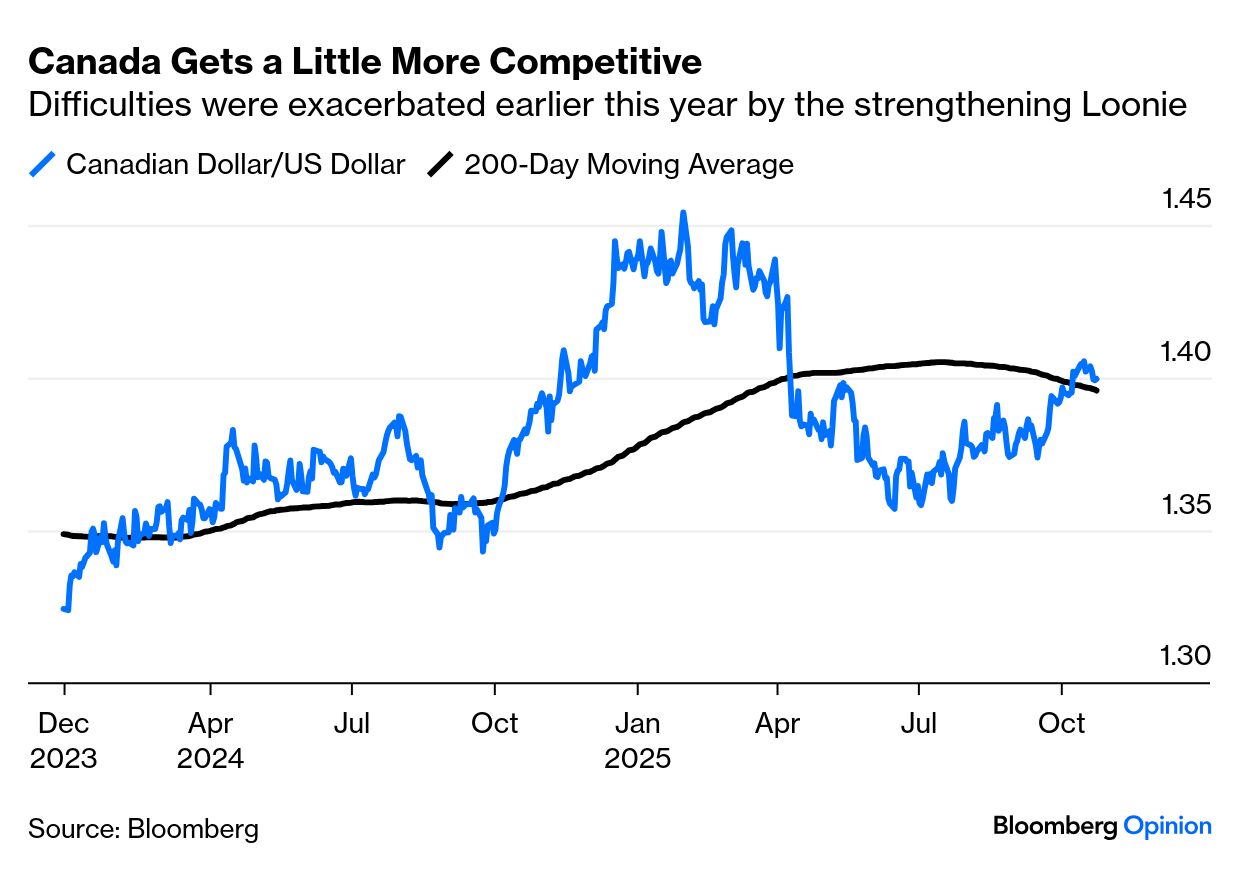

| President Donald Trump’s decision to halt trade talks with Canada and impose an additional 10% tariff over an Ontario-backed TV anti-tariff ad featuring Ronald Reagan is only his latest move to upend the traditional rules of trade diplomacy. Trump’s fury shouldn’t surprise anyone who recalls his proposal for Canada to be the 51st state. While the scope of the additional levy is unclear, it builds on the existing 35% base tariff for noncompliant goods under the US-Mexico-Canada Agreement (USMCA). The setback underscores the difficulties lying in wait for the USMCA’s scheduled review next July. This year’s sharp decline in Canada’s exports to the US has added to the urgency as Ontario resorted to an unconventional approach while Prime Minister Mark Carney engaged Washington — and tried to talk down the provinces. Quarter-on-quarter exports suffered their biggest fall since the pandemic: The pain for Canada also shows up in central bank policy. Previously intertwined with the US, the Bank of Canada has had to cut much more aggressively than the Fed over the last year, and the gap is only projected to narrow a little next year: Earlier this year, that didn’t even help by weakening the currency, but the recent revival of the US dollar might begin to help Canadian exporters. A more dovish Fed could mess that up: It’s possible that trade diplomacy, similar to the latest attempt at an agreement between the US and Beijing, may lead to the reversal of the additional 10% tariff. The bigger question is whether Washington will soften its hardline stance in the USMCA review. George Pollack of Signum Global argues that, unlike the first quarter of this year, the demands the US will likely be making of its neighbors, starting with auto rules of origin revisions, will be too complex for either party to swallow without putting up a fight: In response, we expect President Trump to turn to tools with real bite, such as, for example: Tariffs on USMCA-compliant goods; Triggering the deal’s 6-month termination clause. And while these threats and measures will be tempting for markets to dismiss as mere negotiating bluster, they may prove too serious to ignore.

Still, the 2,000-page-plus agreement — which succeeded the North American Free Trade Agreement in Trump’s first term — won’t be easy to shutter without devastating consequences. It took nearly two years to put the current agreement together, reflecting the intricate supply chain connections between the three countries. Dismantling it in its current form would be painful for all three countries. Michael McAdoo of Boston Consulting Group sees a range of possible outcomes: You can imagine a shorter process where they keep that large agreement intact, but do some smaller side agreements or complementary agreements that would cover a sector that concerns the US or the other countries, or a topic like rules of origin for automotive and how to get more North American content in there. That's another scenario that we're looking at.

With Canada barely escaping a technical recession this year, the reality that it’s tied too tightly to the US is beginning to draw a reconsideration. More than 75% of Canada’s exports go to the US. China has done a great job of finding alternative customers, and Carney is already looking to the East for new trade partners, specifically China and India. The aim is to double non-US exports over the next decade. That target looks ambitious, as exports to both countries have been roughly stable for the last decade. Canada can’t increase its trade as easily as China has: Interdependence cuts both ways. About 60% of America’s crude imports and 85% of its electricity imports come from Canada. Ottawa is aware of its economic importance, even as it recognizes the strain that any pivot away from the US would impose. The same logic extends to Mexico. As Bloomberg Opinion’s Juan Pablo Spinetto notes, geography remains its most significant advantage. Mexico now accounts for nearly 16% of US imports, up from less than 13% when Trump first took office in 2017, and it has surpassed China as America’s top trading partner. Whatever the new terms, Spinetto argues, Mexico will remain more attractive than many other US suppliers. And if Trump’s White House is serious about reviving American industry, it cannot do so without Mexico, whose younger workforce, lower costs and cultural proximity remain essential to that goal. In that sense, Trump’s America First agenda depends on its neighbors succeeding. Which is a point Ronald Reagan might have made. — Richard Abbey |