|

|

|

|

|

|

|

|

|

Kenneth Cheung/Getty Images

|

|

|

|

|

Oh, hi again. Before jumping into today’s newsletter, I have a request: I’m looking to chat with couples who invest together for a story I’m working on about the challenges that come with managing money with another person. Email me at mraman@globeandmail.com with your experience. |

|

|

|

|

Back to our regularly scheduled programming: Last week, in honour of RRSP season, I asked how you feel about registered retirement savings plans, and you didn’t hold back. Here’s what you told me. |

|

|

|

|

|

|

|

|

|

|

Based on the survey I put in last week’s edition, nearly 45 per cent of you said you regularly contribute to an RRSP. Another 17 per cent said you contribute occasionally. But a sizable 38 per cent said you’re not contributing at all right now. |

|

|

|

|

Many of you had perfectly reasonable explanations. Some have already converted their RRSPs into registered retirement income funds, while others have maxed out their contribution room. |

|

|

|

|

Still, a few clear themes emerged. One word came up again and again: TFSA. |

|

|

|

|

Since the tax-free savings account launched in 2009, and the first home savings account followed in 2023, many readers said RRSPs have slipped down their priority list. Unlike RRSPs, TFSA withdrawals aren’t taxed, which makes them feel more flexible for current life plans. |

|

|

|

|

A reader in in London, Ont., wrote that he and his wife recently bought a home and started a family. They used mostly their TFSAs for the down payment, and now any extra cash goes back into their TFSA. “That way, if there are any unexpected major expenses (car breaks down, loss of income, major home repairs, etc), the TFSA allows us to withdraw tax free.” Once they’ve saved up a year‘s worth of expenses there, they plan to return to RRSP contributions. |

|

|

|

|

Others lamented they didn’t have access to today’s options earlier in life. “I wish TFSAs had been available when I was younger,” said another reader in Corbeil, Ont. |

|

|

|

|

Some of you are saving for retirement, just not through RRSPs. A reader in Vancouver said his public-sector job comes with a defined-benefit pension, so for now he’s prioritizing an FHSA and TFSA. “Once the FHSA contribution limit is hit, then I’ll switch over to an RRSP,” he said. |

|

|

|

|

|

|

|

|

And for those with employer plans, convenience matters. A reader in Burlington, Ont., contributes through payroll deductions with an employer match. “I have about $700,000 saved right now,” they said, “but at 48, I still worry whether it’s enough.” |

|

|

|

|

Subscribe to the Retire Rich newsletter

Are you reading this newsletter on the web or did someone forward the e-mail version to you? If so, you can sign up for Retire Rich here. |

|

|

|

|

|

|

|

|

|

|

|

|

|

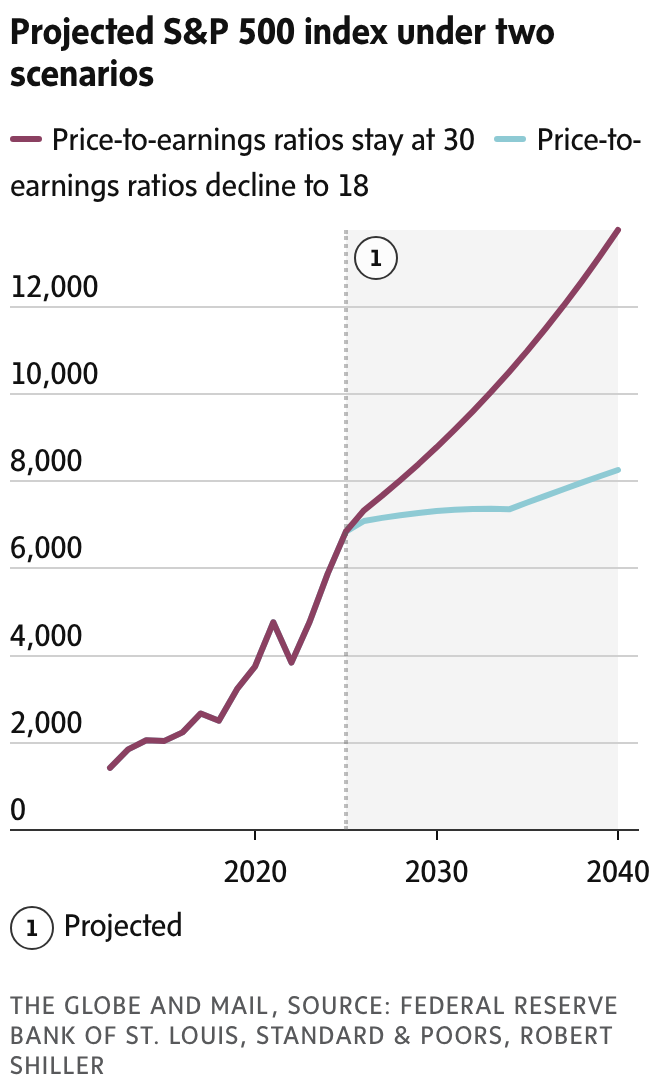

What’s happening: U.S. stock prices, especially the S&P 500, have surged far faster

than corporate earnings. Since 2012, the index has climbed more than 430 per cent, even as real earnings growth has been stuck around 2.4 per cent a year. Today’s valuations are being driven less by fundamentals and more by unusually high price-to-earnings ratios, which sit near 31, well above the long-term average of 18. |

|

|

|

|

What they’re saying: Stock returns are unlikely to keep up this pace, according to Frederick Vettese, former chief actuary at Morneau Shepell. He argues that elevated price-to-earnings ratios rarely last and that a reversion to historical norms would mean much slower growth going forward. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Blair Rogerson does paperwork in his Markham home on Jan. 31. Jennifer Roberts/The Globe and Mail

|

|

|

|

|

|

|

|

|

|

|

The situation: Blair Rogerson spent his entire career at one insurance firm in Markham, Ont. He had originally planned to retire at the end of 2020 after 40 years at the company, but ended up retiring earlier, in June of that year. |

|

|

|

|

How he prepared: He gave advance notice to his employer to help minimize surprises and help support his colleagues by passing on technical information that was required for his role. He also carefully planned his retirement financially well in advance, so he was prepared to step away. |

|

|

|

|

Yes, but: Announcing you’re leaving early (beyond the standard 30-to-90-day notice period) can pose some risks, such as muddying workplace dynamics, or shifting how projects are assigned. In more serious cases, giving notice during company downsizing could lead to subsequently missing out on severance or bonus packages tied to that period. |

|

|

|

|

|

|

|

|

|

|

|

|