Back in 2014, The Economist declared that “the globalisation of the [Chinese RMB] seems remorseless and unstoppable.” Notwithstanding hurdles in tracking remorse, we begged to differ—and were right.

A dozen years on, however, and RMB internationalization is showing renewed signs of life. The IMF’s recent annual staff report on China’s economy identified several metrics along which the RMB’s use in trade and finance has been rising modestly. These include the share of trade invoicing settled in RMB, offshore RMB lending, and issuance of “panda bonds”—RMB-denominated bonds issued in China by foreign entities.

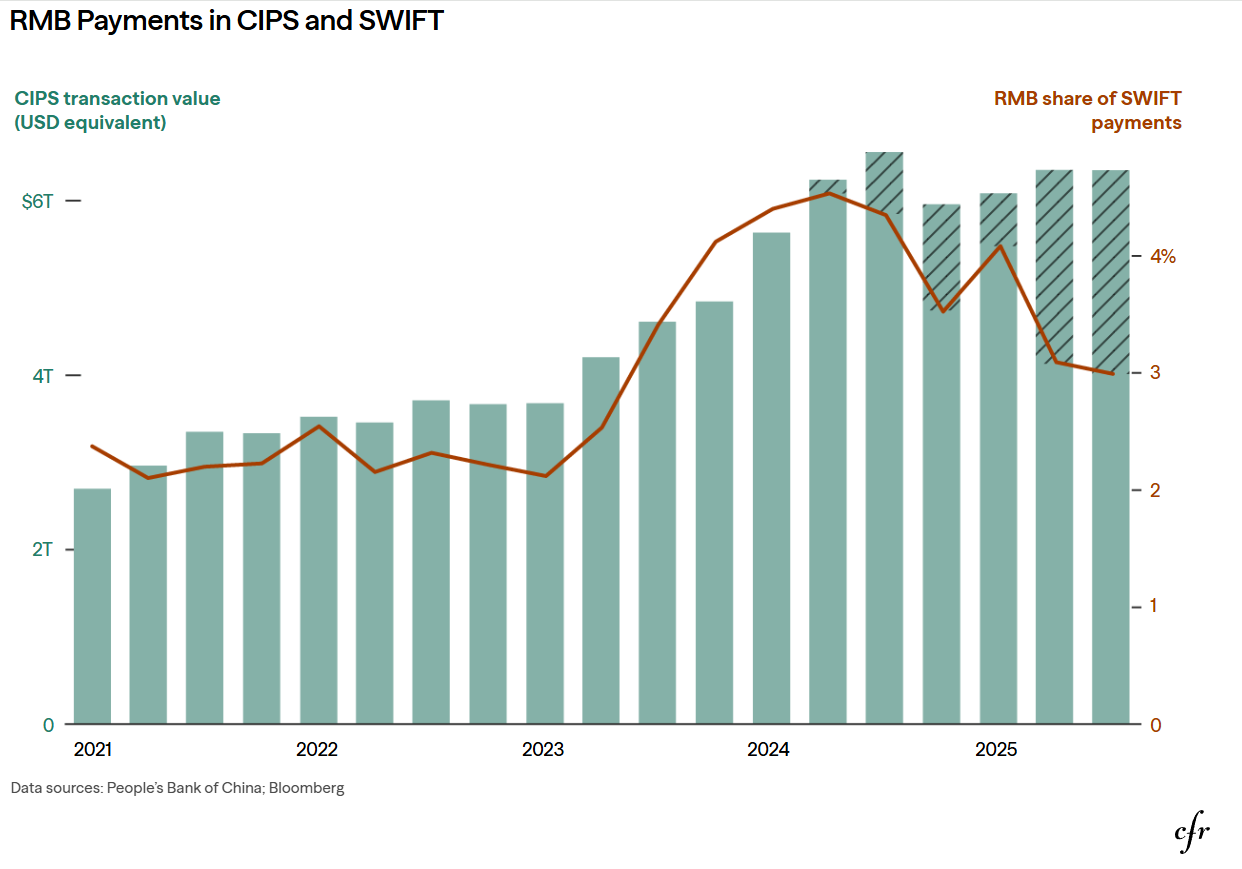

On one metric, however, the data, on the surface, seem anomalous. As shown by the red line in the graphic above, the RMB share of payments over SWIFT—the main messaging network for international financial transactions—has been in fairly steep decline since 2024, suggesting a lessening global role for the RMB.

This, however, is not the case. As we show in the accompanying vertical green bars, there has, since 2023, been an offsetting rise in RMB transactions over CIPS—China’s system for interbank RMB payments and messaging.

Historically, CIPS payments have been accompanied by necessary SWIFT messages containing payment instructions. As recently as 2022, an estimated 80 percent of CIPS payments were accompanied by SWIFT messages. Since 2024, however, direct participants in CIPS—the only participants able to make payments accompanied by CIPS messages—have grown by nearly 40 percent: from 139 banks to 193. Direct participation has grown not only in absolute terms but as a proportion of total CIPS membership. This means that large volumes of payments messages that would in the past have gone through SWIFT now go through CIPS. It follows, then, that the decline in the share of RMB payments on SWIFT is not an indicator of a lessening global role for the RMB, but rather of RMB payments becoming less dependent, and therefore less visible, on the SWIFT messaging network.

Why should we care? The U.S. has long relied on the threat of cutting off foreign banks from SWIFT in order to pursue foreign-policy objectives—such as pushing Russia to end its war against Ukraine. Although RMB transactions are still a tiny percentage of total international transactions, a continued shift to RMB—and the accompanying messaging from SWIFT to CIPS—will weaken the role of the dollar as a sanctions tool.