|

MAIN FEATURE

THE BANKS HAVE COMPLETELY TWISTED OUR PERCEPTION OF SAFE VS. DANGEROUS

"Isn't this dangerous?!"

I was talking to someone recently about building their wealth operating system and this was their response when we started talking about debt and leverage.

In fact I get this same response at least once a week.

So I asked him a few questions.

Did he have a mortgage? Yes.

Car payment? Yes.

A HELOC with a balance on it? Actually, yes.

And none of it had a stress test behind it. No liquidity plan. No risk mitigation. No exit strategy. He just signed and moved on like everyone else does.

But he wasn't worried at all about any of those decisions.

The reason why is because the financial institutions selling you these products have some of the biggest marketing budgets in the world. Not only TV and social media, think about how many offers you get in the mail.

They've made debt feel like a normal responsible adult decision. Everyone takes on consumer debt without thinking twice, yet when it comes to good debt to create financial freedom for themselves, suddenly it becomes a terrifying idea.

So when someone looks at what we do and says this feels risky, what they are really saying is this feels unfamiliar.

Here is the part that nobody talks about. We actually put more guardrails in place than most people have on the leverage they are already carrying. It all comes down to these 4 steps...

1. Know your levers

Before anything else, you need an honest inventory of what you actually have.

What assets do you own, what can they support, and how hard do you want to pull based on where you are right now and where you want to go?

And where do you want to go. Most people assume their financial goal is to just make more money. More money automatically means more freedom, right?

But it's like a GPS. You have to punch in where you want to go. If you don't have the coordinates, how could you ever hope to plot the right course?

This is not a generic answer. It is specific to your situation, your goals, and your timeline. Most people have never done this exercise and therefore have no idea what they are actually working with.

2. Risk mitigation first, not after

Most people find out their risk tolerance when something goes wrong. That is the worst possible time to figure it out.

The move is to identify in advance the conditions under which a position becomes uncomfortable and decide what the response is before that moment arrives.

When you have that in place, nothing that happens in the market catches you off guard.

You've heard me say it before- the most important goal of our wealth operating system is to never be a forced seller. Never be put in a position where you have to make a decision you don't want to.

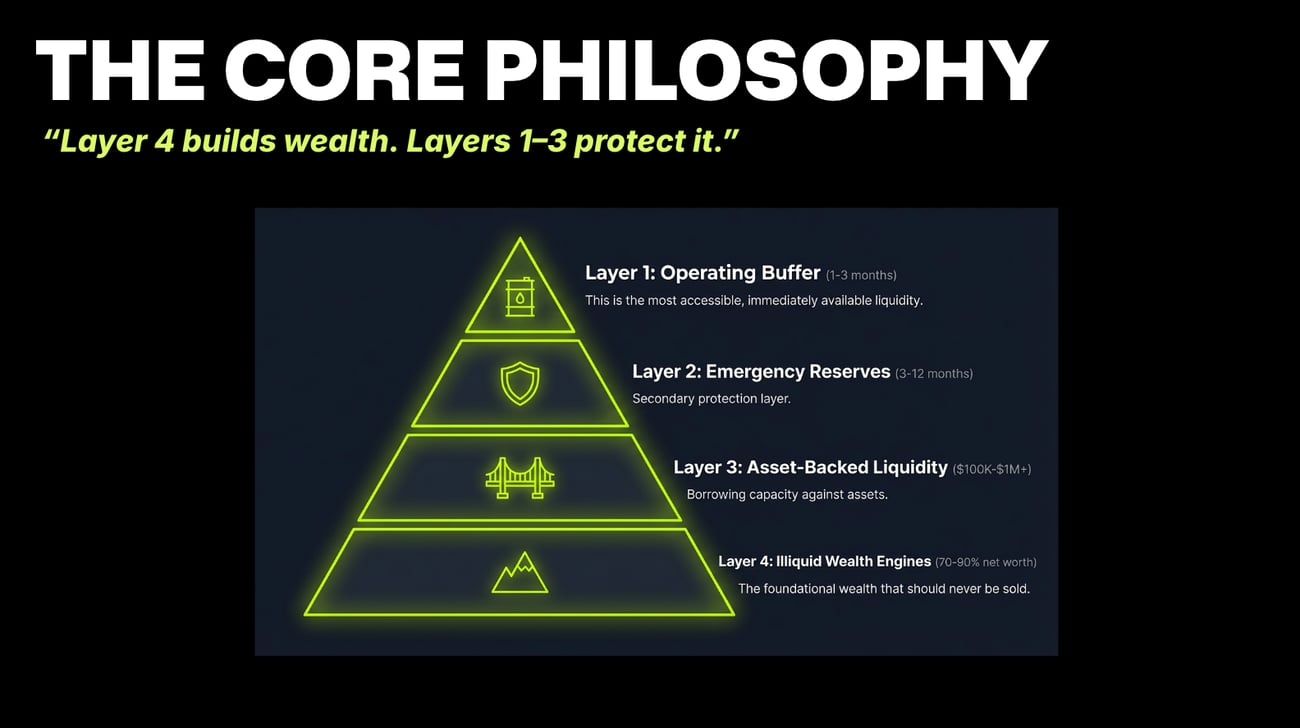

3. Know your liquidity layers

This one changes everything for most people.

Access to capital does not mean making more money or selling an asset. There are multiple layers of liquidity available to most people that they have never mapped out.

There are 4 layers everyone should have, and when you have all 4 in place you always have a move. You never get backed into a corner.

4. Stress test before you commit

Model the downside before you do anything. What does this look like if the asset drops significantly? What does it look like if income slows for six months?

Run the scenarios while you are calm, not while you are reacting. This is the single thing that keeps you from becoming a forced seller at the worst possible moment.

The part that always gets me...

Most people signed up for that debt without a single one of those things in place. No stress test. No liquidity map. No plan for when things get uncomfortable. Just a signature and a monthly payment.

And yet somehow the strategies that actually have all of this built in are the ones that feel scary.

Think about that for a second. The unexamined version is normal. The thoughtful version is dangerous. That is completely backwards.

Here's the real question. Are you using leverage to pay for things you can't afford, or are you using it to build wealth and accelerate the velocity of every dollar you have?

Because both are leverage. But only one of them is working for you.

You're already using it. You have been for years. The only question is whether you are using it like someone who has actually thought it through?

|