| | Oil prices fell to their lowest point since the first day of the Iran war.͏ ͏ ͏ ͏ ͏ ͏ |

| |  | Energy |  |

| |

|

- Slow return of flow

- Oil battle not over yet

- Mining shift

- Another offshore wind buyout

- Green industrial strategy

The green economy hits a record $10 trillion market value. |

|

The deal signed yesterday between Washington and Tehran to reopen the Strait of Hormuz proved Iran’s energy weapon was powerful enough to take on the world’s mightiest military and come out ahead. Earlier in the conflict, US President Donald Trump repeatedly stressed that the war could only end with Tehran’s “unconditional surrender.” Yet the agreement includes numerous conditions, perhaps most importantly that Iranian oil is back on the menu. This is a huge prize for Tehran, which prior to February had been forced to sell most of its oil to China at steep discounts because of US sanctions. Iran could stand to gain $60 billion a year by regaining access to the regular market. And when Trump announced the terms of the deal, he was clear about the driving force behind it: “We run out of [oil] reserves in about four weeks. We would really run out. You want to see bedlam?” One fascinating thing about the past few months has been that bedlam took longer to arrive than many people thought it would, given the world suffered the biggest volumetric disruption to oil and gas supply in history. There was pain at the pump, especially in Asia. European airlines hit some turbulence. And I won’t forget getting hassled by energy curfew-enforcing cops in Cairo. But crude oil prices in Europe and the US didn’t top their post-Ukraine peaks. And now, the International Energy Agency warned yesterday, we’re likely facing a glut. Yet, as the world’s tanks drained out, Trump was clearly able to see a scary-looking cliff approaching fast, and blinked. It’s too early to say this is all over; one drone could bring the whole thing down. But so far, there are a few key lessons from the crisis. - Contrary to the central promise of “energy dominance” — that high oil and gas production gives the US an indomitable geostrategic advantage — in this case US drilling was only able to delay the inevitable extreme price spike, to buy time for a deal that mainly achieves a return to the status quo. The US is still, ultimately, at the mercy of the global market. And for now, Iran retains enough control over that market that the US was willing to pay Tehran to reopen it (and possibly to keep it open, if Tehran manages to institute passage “fees”).

- But, the weaponization of oil flows is a “wasting asset,” as one former security official put it to me this week. One big reason this crisis was less painful was because millions of consumers, executives, and political leaders worldwide have already realized the security benefits of reducing their exposure to fossil fuels. Like any other military asset, every time the energy weapon is used, someone on the other side improves their defenses. In the years ahead, the leverage Iran can gain from its control over the Strait of Hormuz will diminish (to “zero,” if the UAE has its way), as will the US ability to use drilling as a shield or cudgel — this week, even an exec from American LNG exporter Cheniere admitted as much.

- Patience is a virtue for producers. The crisis was certainly good for oil companies, but the really booming corner of the business was trading, not drilling; European majors outshone their US competitors in first-quarter earnings because of their robust trading desks. And while some US producers were cautiously beginning to follow Trump’s call for more oil, most remained loath to do so, having foreseen a return to less dazzling prices. That seems like a smart move.

- The political cost of all of this to Trump remains unclear. Given the amount of time needed to fully reopen the strait (the return of pre-war daily oil flows could take until January in an optimistic case, according to Rystad Energy) and the competition that refineries will face for crude with hungry storage tanks, US gasoline prices could fall slowly — although they already dipped below $4 per gallon on Thursday. Analysts think Trump is likely to reauthorize a waiver of the Jones Act, which facilitates oil shipping, but apart from that there is precious little he can do to further drive down prices. By the time the midterm elections roll around, voters will want to know what those costs have bought them, in the form of a strong nuclear deal. Now that race is on.

|

|

Majid Asgaripour/WANA via Reuters Majid Asgaripour/WANA via ReutersOil prices fell to their lowest point since the first day of the Iran war, after Trump and Iranian President Masoud Pezeshkian signed a deal to reopen the Strait of Hormuz. The deal lifts the US blockade and sanctions on Iranian oil exports, and commits Tehran to ensure that shipping traffic returns to its pre-war level within 30 days. That’s an ambitious goal: Although many tankers are making a dash to the Persian Gulf, there’s likely to be a traffic jam, plus the challenge of restarting thousands of shuttered wells. And as the threat of re-escalation remains tangible, ships may simply not be called on: Goldman Sachs forecasts that oil volumes through the strait will likely return to only 70% of prewar levels as Gulf producers build out alternative routes. In the meantime, as more Iranian barrels return to market, more Russian ones may be coming off: At the G7 meeting in France on Wednesday, Trump said the US was looking to reinstate harsher sanctions on Russian oil and gas. |

|

| |  | Clay Chandler |

| |

Nobuo Tanaka. Michael Buholzer/Reuters Nobuo Tanaka. Michael Buholzer/ReutersThe former head of the International Energy Agency thinks it’s too early to celebrate the end of the biggest energy disruption in history. “This is the third oil shock,” Nobuo Tanaka, who led the IEA from 2007 to 2011, told Semafor this week. “Just as the first and second oil shocks made a huge impact on the global economy, the third shock is a transformational moment.” Tanaka speaks with authority, having ridden out every major oil crisis since the 1970s. He’s cautious in assessing the timeline for a return to “normal.” Even with the deal signed Wednesday, he says, full supply recovery could be two years away. But what really troubles him is something larger: The crisis, in his view, has cracked open a fault line that was already forming in the global energy order between “petrostates,” led by the US, and “electrostates,” led by China. He warns that the consequences for every major economy, and every major company, will be profound. The immediate pain of an oil shock is not the point, he said. The main thing is the responses it triggers, from governments, industries, and companies — how it reshapes the global economic order in the aftermath of the crisis. And history, he argues, is unambiguous on this: Countries that read that signal fastest and bet on the right technology don’t just survive shocks, they profit from them. “CEOs should watch the long-term geopolitics of energy,” he says. “The petrostates versus electrostates battle will impact every business, every supply chain. The companies that understand this transformation now are the ones that will be competitive later.” |

|

Steve Marcus/Reuters Steve Marcus/ReutersA major US-Saudi mining investment program is shifting its focus to Iran’s reconstruction. During Trump’s visit to Riyadh last year, the US investment firm Burkhan World signed a $9 billion MOU with the Saudi mining firm Grand Mines, aimed at strengthening Saudi access to critical mineral supply chains. Originally, the intent was to acquire mines in sub-Saharan Africa and send the minerals to new refineries in Saudi Arabia for processing. Now, the fund has turned its gaze to Central Asia — specifically to mineral supplies from Kazakhstan and Pakistan that could be useful for the postwar reconstruction of Iran, Burkhan CEO Shahal Khan told Semafor. The deal “completely changed into something much larger because of the war,” he said, adding the Saudi government “wants to give Iran the ability to fully function outside of sanctions and be able to rebuild its economy.” Bandar Alkhorayef, the Saudi mining minister, touted the prospects for joint ventures with Kazakhstan during a visit there this week. Khan’s pivot is well-timed, coming at the same moment the US-Iran deal introduces a $300 billion fund to support Iran’s reconstruction. “The Saudi deal we have is now geopolitically even more important,” Khan said. “[It] allowed us to negotiate with other parties for minerals that we didn’t plan for originally.” |

|

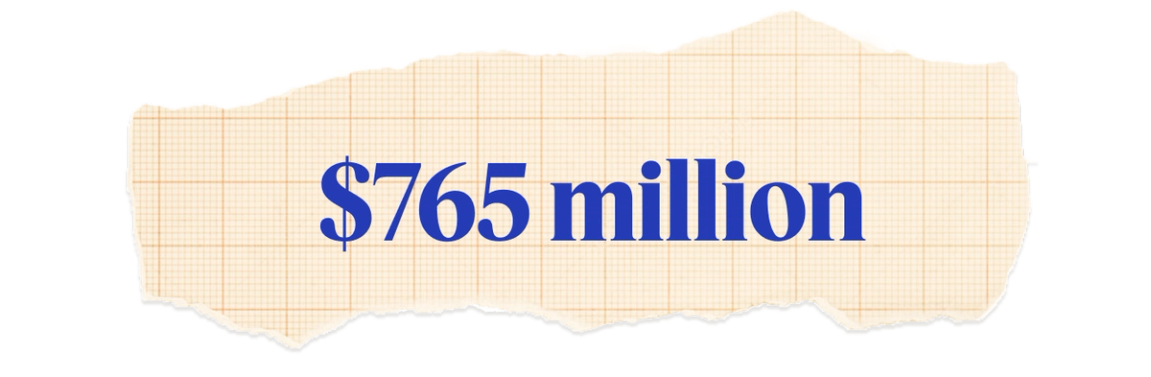

Another offshore wind buyout |

The Trump administration sealed its fourth deal with an energy company to pull the plug on a new offshore wind farm. Invenergy, the developer, will be returned $765 million that it paid for leases under the Biden administration, which it will reinvest in new gas-fired power plants. The deal brings the total amount the Trump administration has committed to cancelling offshore wind projects to more than $2 billion. An earlier deal offered in March to TotalEnergies is already embroiled in a lawsuit, and these payouts are likely to become a focal point for Congressional investigators if Democrats succeed in winning control of the House of Representatives in November. In an interview at Semafor’s World Economy summit in April, Invenergy CEO Michael Polsky said the company’s policy toward different energy technologies is “to encourage everything and let the market decide what they’re willing to buy.” In this case, the market wasn’t the only vote on the matter. |

|

Green industrial strategy |

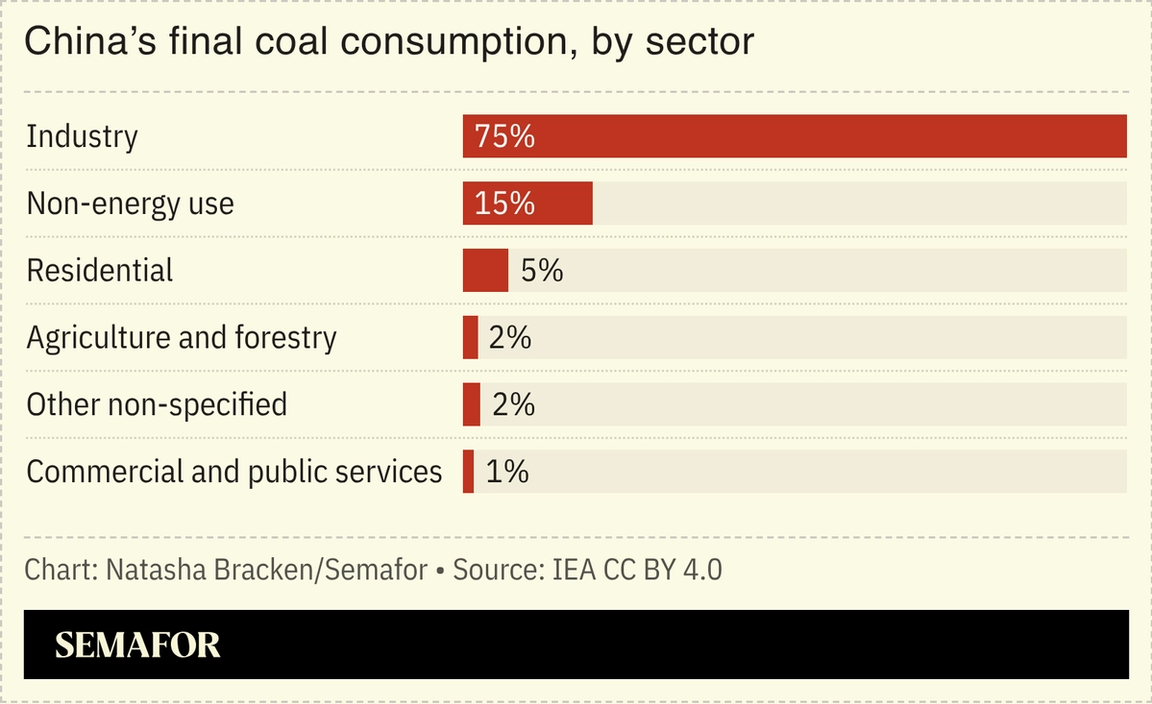

China unveiled a three-year plan to curb energy consumption and carbon emissions across nine of its most energy-intensive sectors. Starting in 2026, producers in industries including steel, aluminum, cement, and coal power that fail to meet energy-efficiency benchmarks could face higher electricity costs. By the end of 2028, any capacity that fails to meet efficiency standards will be phased out entirely —- a move Beijing estimates could save roughly 100 million tons of standard coal and reduce carbon emissions by 200 million tons. The new plan demonstrates China’s willingness to curb coal consumption, a fuel it turned to last month when fossil-fuel generation rose 2.1% to offset low wind speeds. Despite its continued dependence on fossil fuels at home, abroad the country is still very much a leader in the global clean economy: China accounts for roughly 25% of the global clean-industry pipeline and has secured 13 of the 19 new investment decisions announced since November, according to Mission Possible. |

|

New Energy- Fixing the US electric grid’s reliability issues could give the executives in charge a huge payout, as the value of a publicly traded utility is directly tied to its capital spending.

- Renewable energy projects across Africa have stalled because they cannot secure funding due to a rule that ties the creditworthiness of projects to the sovereign rating of the country where they operate.

- The White House dropped legal efforts to reimpose a freeze on wind farm projects nationwide, with US renewables development surging despite Trump’s opposition.

Fossil FuelsFinance- The green economy hit a record high market value of $10 trillion. The S&P Global Clean Energy Transition Index has surged more than 80% since the end of 2024, more than double the return of the S&P 500.

|

|

|