MAIN FEATURE

GIVE YOUR KIDS A HUGE INHERITANCE, BUT MAKE IT MORE THAN MONEY

Most people think leaving their kids money is enough. It's not.

I'm going to show you why, plus the five things your inheritance plan actually needs to include.

There's a famous book called The Millionaire Next Door. You've probably read it.

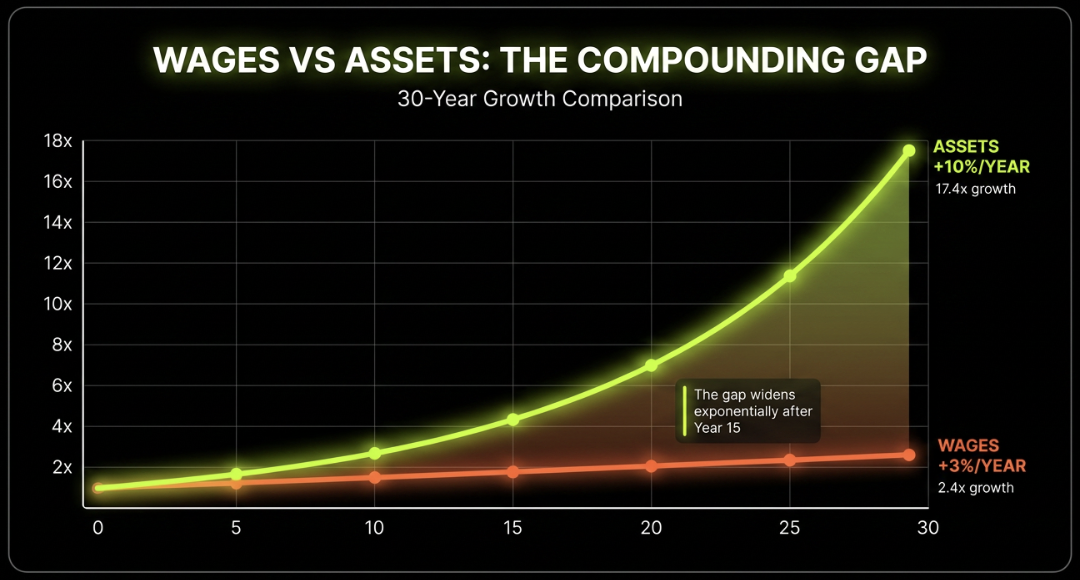

The idea is the average millionaire isn't driving a Ferrari or chartering jets. It's your unassuming neighbor who drives a beater truck and lives well below his means to invest as much as possible.

One of the most successful personal finance books of all time. But here's the sequel nobody wrote...

After that neighbor dies, the money is gone within sixteen months. Because his kids aren't going to deprive themselves the way he did. Nobody wants to live like that.

So when the money shows up, they have no framework for it, no values around it, no idea how it was built. And it disappears.

Most people make a will and think they're covered. I made a quiz that gives you an inheritance readiness score. It shows exactly how robust your plan is for preserving and passing down your Bitcoin. You can check it out here.

But legal structure is only half of it. The real question is what operating system you're passing down alongside the assets.

The most important document I've ever written is my family constitution. It started at 52 pages, I got it down to 38 because I wanted it to actually be read.

Here's what it needs to include:

1. Your legacy vision. What does your family stand for? Rockefeller wrote letters to his son. This is your version.

2. Core values, codified. Not "integrity" written on a wall. What would a future trustee need to see to confirm your heirs are living by these values?

3. A family mission statement. What do you stand for, stand against, build wealth for? Mine: give my family options and help more people in the world. Everything flows from that.

4. Rules for accessing the wealth. Not just age. What if there's an addiction? A divorce? Do they need to be working? These guardrails are what separate an inheritance from a curse.

5. Succession planning. Who governs it when you're gone? What happens when your kids raise your grandkids? Most people never answer this and the legacy dies with the first generation.

Money without the operating system disappears. Money with it compounds for generations.

That's the inheritance worth building.

|